Glossary entry

Power of Attorney for Elderly Parents: Types Defined and What Caregivers Need to Know

What Is a Power of Attorney? Key Terms Every Caregiver Should Know

A Power of Attorney (POA) is a legal document in which one person — the principal — voluntarily grants another person — the agent (also called an attorney-in-fact) — the legal authority to act on their behalf. Depending on how it is written, that authority can cover financial decisions, medical decisions, or both.

Four foundational terms define how every POA works in practice:

- Principal: The person who creates and signs the POA. In eldercare, this is your parent. The principal must be mentally competent at the time of signing — the document is only valid if they understand what they are authorizing.

- Agent: The person authorized to act on the principal's behalf. This is often an adult child or trusted family member, but it can be any competent adult the principal chooses.

- Fiduciary duty: The agent's legal obligation to act in the principal's best interests — not their own. Misuse of POA authority can result in civil liability and criminal charges. The Consumer Financial Protection Bureau recognizes the agent role as a distinct fiduciary responsibility with specific legal accountability.

- Legal capacity: The mental competency required to sign a valid POA. This is not a clinical diagnosis — it means the principal understands the document's implications at the time of signing. A medical diagnosis alone does not automatically eliminate capacity, but it creates urgency to act.

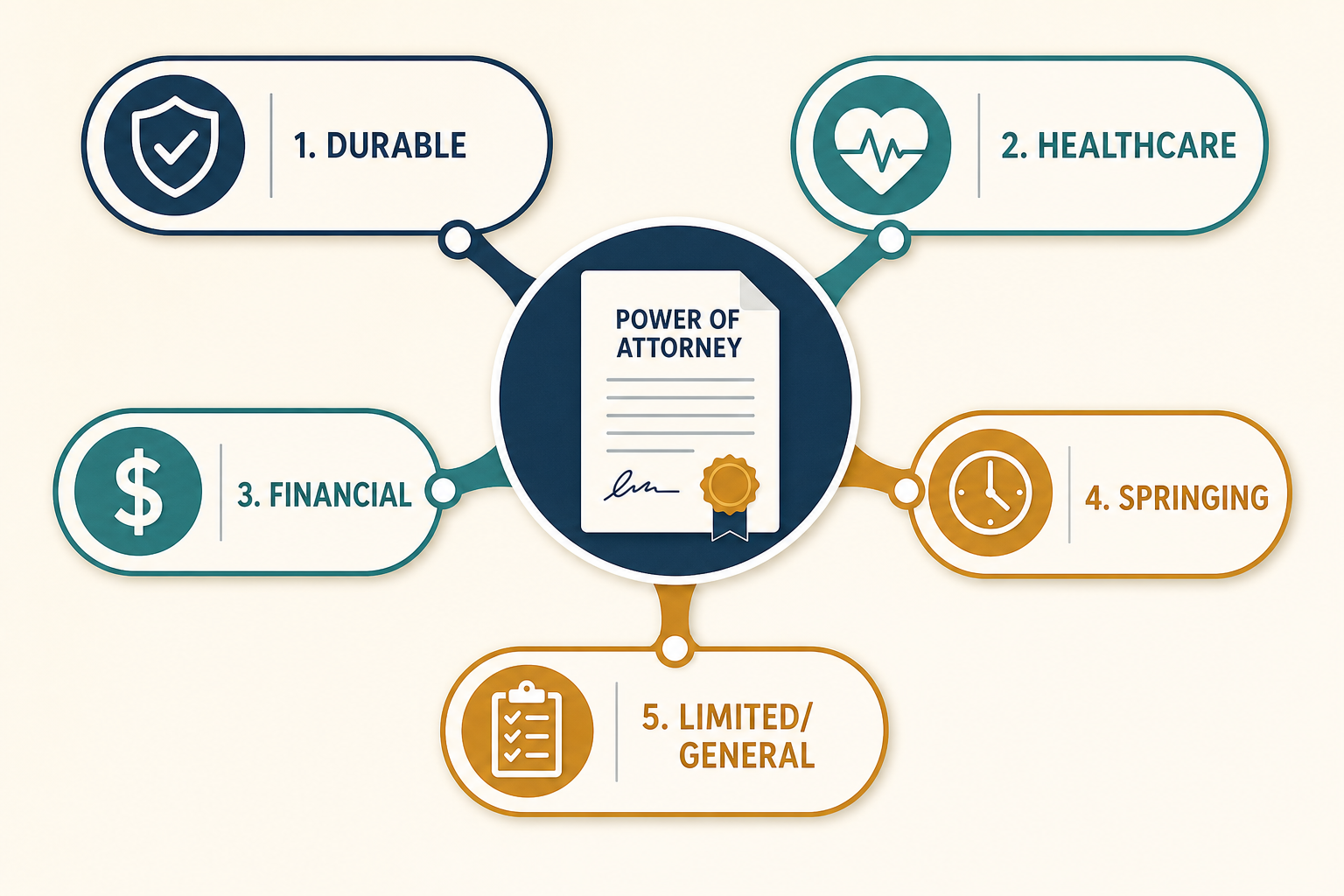

The Five Types of Power of Attorney: At a Glance

Five distinct POA types appear in eldercare planning. Each serves a different purpose and carries different implications for when and how an agent's authority activates. The table below gives an overview before each type is addressed in depth.

| POA Type | Core Function | Survives Incapacity? | Eldercare Relevance |

|---|---|---|---|

| Durable POA | Broad authority (financial and/or healthcare) that remains valid after the principal loses capacity | Yes — by design | Essential. The foundational eldercare document. Without the durable designation, authority ends precisely when it is most needed. |

| Healthcare POA | Authorizes agent to make medical decisions when the principal cannot communicate | Yes, when drafted as durable | Critical for any parent facing surgery, hospitalization, or cognitive decline. Must include HIPAA authorization language. |

| Financial POA | Authorizes agent to manage banking, investments, property, taxes, and bill-paying | Yes, when drafted as durable | Necessary to pay bills, manage assets, and handle financial institutions if a parent becomes incapacitated. |

| Springing POA | Authority activates only after a physician certifies incapacity in writing | Yes — but only after activation | Rarely recommended for eldercare. Documented delay risk during acute crises. Durable POA is the preferred alternative. |

| Limited / General POA | Restricts agent authority to specific tasks (limited) or grants broad authority that terminates at incapacity (general/non-durable) | No — terminates at incapacity unless drafted as durable | Useful for specific short-term tasks. A general (non-durable) POA is inadequate for eldercare planning because it lapses when most needed. |

Durable Power of Attorney: The Eldercare Cornerstone

A Durable Power of Attorney is a POA document that contains specific language stating the agent's authority remains in effect even if the principal later becomes incapacitated. That single word — durable — is what makes this document the foundation of eldercare legal planning.

A standard (non-durable) general POA terminates automatically the moment the principal loses capacity. This means the document becomes legally void at exactly the moment a caregiver needs it most — during a hospitalization, a dementia progression, or a stroke. The American Bar Association confirms that most states permit a durable POA that remains valid from signing until the principal dies or revokes it.

In practice, most eldercare attorneys draft financial and healthcare authority as two separate durable POA documents, each tailored to its domain. Some states permit a single combined document; others require or strongly recommend separate instruments. State law governs what language is required for the durable designation to be legally effective.

Healthcare Power of Attorney: Medical Decisions and the HIPAA Connection

A Healthcare Power of Attorney (also called a Medical POA or Healthcare Proxy) is a separate legal document from a financial POA. It authorizes the agent to make medical decisions on the principal's behalf when the principal is unable to communicate those decisions — during surgery, a medical emergency, or advanced cognitive decline.

The agent's authority under a healthcare POA can include decisions about treatment options, surgical procedures, care settings, and end-of-life interventions — but only to the extent the document grants that authority and only when the principal lacks the capacity to decide for themselves. The Alzheimer's Association is explicit that a POA does not give the agent authority to override the principal's decisions while the principal still has legal capacity.

The HIPAA dimension of healthcare POA is frequently underestimated by caregivers — and the consequences of overlooking it are immediate and serious.

What caregivers need to verify:

- The healthcare POA document contains explicit HIPAA authorization language — not just a general grant of medical decision-making authority.

- The HIPAA language is current. Older documents may use outdated authorization language that healthcare providers no longer accept.

- Copies have been provided to every healthcare provider, hospital system, and specialist involved in the parent's care — not just the primary care physician.

Healthcare POA is also distinct from a living will. A living will documents the principal's specific medical wishes but does not appoint a decision-maker. Healthcare POA appoints the decision-maker. Both documents serve different functions and both are typically needed — this distinction is addressed in detail in the advance directives section below.

Financial Power of Attorney: Scope, Limits, and Institutional Acceptance

A Financial Power of Attorney authorizes the agent to manage the principal's financial affairs. When drafted as durable, this authority continues after incapacity. The scope of authority can be broad or narrowly defined — the document itself determines what the agent can and cannot do.

Common financial authorities granted in eldercare POA documents include:

- Banking transactions: accessing accounts, writing checks, making deposits and withdrawals.

- Investment management: buying, selling, or managing securities and retirement accounts.

- Real property: selling, renting, or managing real estate.

- Tax filing: preparing and signing federal and state tax returns.

- Bill-paying and debt management: paying recurring expenses, managing loans.

- Government benefits: interacting with Social Security, Medicare, and Medicaid on the principal's behalf.

- Digital assets (as of 2026 in many states): managing online accounts, email, and digital financial accounts — discussed further in the 2026 updates section below.

A critical practical reality: having a valid financial POA document does not automatically mean every institution will honor it. Banks, brokerage firms, insurance companies, and government agencies each have their own acceptance procedures. Some require their own supplemental authorization forms in addition to the POA document. Some institutions will only accept POA documents executed within a recent time window, regardless of the document's stated terms.

- Notify every financial institution where the parent holds accounts and confirm their specific acceptance requirements before a crisis arises.

- Ask each institution whether they require a supplemental authorization form in addition to the POA.

- Keep certified copies of the POA document — some institutions require originals or certified copies, not photocopies.

- If the parent banks at multiple institutions, confirm acceptance at each one separately.

Springing POA and Limited/General POA: When Scope and Timing Matter

A Springing Power of Attorney does not take effect when signed. It "springs" into effect only after a triggering condition — typically a licensed physician's written certification that the principal has lost capacity. Until that certification is obtained and documented, the agent has no authority to act.

The appeal of a springing POA is intuitive: some principals prefer that an agent's authority not be active while they are still fully capable. The practical risk, however, is significant in eldercare contexts.

A Limited Power of Attorney restricts the agent's authority to specific tasks (for example, selling a particular piece of property, or managing finances during a specific period of time). It terminates when the specified task is completed or the time period expires. This type is occasionally useful for discrete transactions but is not designed for ongoing eldercare management.

A General Power of Attorney grants broad authority across financial and personal matters — but unless it is explicitly drafted as durable, it terminates automatically if the principal becomes incapacitated. This is the most important distinction for caregivers to understand: a general POA without durable language is legally void at the moment of incapacity, regardless of how broad its stated authority is.

The Capacity Window: Why Timing Is Everything

Every POA type shares one absolute requirement: the principal must have legal mental capacity at the time of signing. This is not a clinical threshold — it is a legal standard. The principal must be able to understand what the document says, what authority they are granting, and what the consequences of that grant are.

A dementia diagnosis does not automatically eliminate legal capacity. Cognitive impairment exists on a spectrum, and capacity can fluctuate — someone in early-stage Alzheimer's may retain the ability to understand and sign a POA on a given day, while someone with advanced dementia may not. The assessment is made at the moment of signing, not based on a prior or subsequent diagnosis.

The Alzheimer's Association is direct about the timing imperative: legal documents including POA should be put in place as soon as possible, while the person is still able to make decisions. Once capacity is lost, no POA can be created — the window closes permanently.

What this means in practice for caregivers:

- A new diagnosis — even an Alzheimer's diagnosis — is not a reason to wait. It is a reason to act immediately, while the window is still open.

- Capacity is not all-or-nothing. An elder law attorney can advise on whether a parent can currently sign a valid POA, and a physician may be asked to document capacity at the time of signing as a precaution against future challenges.

- The capacity window can close without warning. A stroke, a fall with head injury, or a rapid cognitive decline event can eliminate capacity overnight.

- Proactive planning — before any diagnosis or decline — is always preferable to planning under time pressure.

Without a POA: Guardianship and Conservatorship

When a parent loses capacity without a valid POA in place, adult children often discover — sometimes mid-crisis — that being someone's son or daughter does not give them legal authority to manage a parent's finances or make medical decisions on their behalf. Family relationship confers no automatic legal standing.

The only legal path forward is a court proceeding. A family member must petition a court to be appointed as the parent's guardian (for personal and medical decisions) or conservator (for financial decisions), or both. The court then supervises the arrangement on an ongoing basis.

What this process typically involves:

- Filing a petition with the probate or family court in the parent's jurisdiction.

- Medical evaluation to establish incapacity, typically requiring physician documentation.

- Court-appointed attorney for the parent (the "ward") in most states, adding to costs.

- A hearing at which the court evaluates the petition and appoints a guardian or conservator.

- Ongoing annual reporting to the court on the parent's condition, finances, and decisions made on their behalf.

The timeline under normal circumstances is typically three to six months. Emergency guardianship can move faster in acute situations, but it is not guaranteed and adds additional legal complexity.

Beyond cost and time, guardianship carries a dimension that many families do not anticipate: the parent loses the right to choose who advocates for them. The court appoints a guardian based on its own assessment — not the parent's preference. As the American Bar Association notes, without a POA, "you may not have the ability to choose the person who will act for you." A guardianship is also a matter of public court record, unlike a privately executed POA.

If other family members contest the guardianship petition — disagreeing about who should serve or whether it is necessary — the proceeding can become adversarial, depleting assets and straining relationships at an already difficult time.

How to Establish a Power of Attorney: Steps, State Requirements, and 2026 Updates

Establishing a POA is a legal process governed by state law. Requirements for execution — notarization, witnesses, specific language — vary by state and by POA type. The following steps reflect the general process in the United States, with consistent caveats about state variation.

- Choose an agent carefully. The agent should be someone the principal trusts completely, who is organized and capable of handling financial or medical matters, and who is willing to take on the responsibility. The agent's fiduciary duty is legally binding — choose someone who understands that obligation. Discuss the role with the person before naming them.

- Work with an elder law attorney to draft the documents. POA documents for eldercare purposes are not one-size-fits-all. An elder law attorney can ensure the durable designation is properly worded, that HIPAA language is current in the healthcare POA, that scope of authority matches the family's needs, and that the document meets current state execution requirements. Online form services are not a substitute for legal counsel in this context.

- Execute the document according to state law. Most states require notarization. Many also require one or two witnesses who are not the agent and are not named in the principal's will. Some states have specific additional requirements for healthcare POA documents. Failure to meet execution requirements can render the document invalid.

- Distribute certified copies to all relevant parties. Financial institutions, banks, investment accounts, the parent's primary care physician, any specialists, and hospital systems where the parent receives care should all receive copies. Confirm each institution's acceptance requirements.

- Store the original document securely and tell the agent where it is. The agent needs to be able to locate and present the document when needed — in an emergency, time matters.

- Review and update the document periodically. Laws change, circumstances change, and the chosen agent may no longer be available or appropriate. Elder law attorneys generally recommend reviewing POA documents every three to five years, or after major life events.

2026 Legal Updates: Digital Assets and Remote Notarization

As of 2026, two meaningful changes have affected POA practice in many states, though adoption is not universal and state laws continue to vary.

- Digital asset authority: Many states have updated their POA statutes to explicitly authorize agents to manage digital assets — including online banking accounts, email, social media profiles, subscription services, and in some cases cryptocurrency holdings. If a parent's POA document predates these updates, it may not clearly grant authority over digital accounts. An elder law attorney can advise on whether the existing document needs to be updated or supplemented.

- Remote notarization: Many states have permanently authorized remote online notarization (RON) for POA documents, allowing the signing and notarization process to occur via video conference rather than in person. This significantly improves access for seniors with mobility limitations or for families managing eldercare from a distance. Not all states have adopted permanent remote notarization — confirm current rules with a local elder law attorney.

POA, Advance Directives, and Living Wills: How They Work Together

These three terms are frequently used interchangeably in caregiving conversations — and that confusion creates real gaps in eldercare planning. Each document serves a distinct function.

| Document | What It Does | Appoints a Decision-Maker? | Specifies Medical Wishes? |

|---|---|---|---|

| Healthcare Power of Attorney | Authorizes a named agent to make medical decisions when the principal cannot communicate | Yes — appoints a specific agent | No — the agent decides based on their knowledge of the principal's values |

| Living Will | Documents the principal's specific wishes about life-sustaining treatment in defined medical situations | No — does not name an agent | Yes — specifies the principal's preferences directly |

| Advance Directive | Umbrella term for documents that address future medical care, including healthcare POA and living will | Depends on the specific document | Depends on the specific document |

The Alzheimer's Association clarifies the distinction precisely: a living will is a type of advance directive that expresses how an incapacitated person wishes to be treated in specific medical situations — it generally comes into play once a physician determines the person is incapacitated and unable to communicate. It does not appoint anyone to act on their behalf.

Common Caregiver Mistakes — and How to Avoid Them

The following mistakes are the most consequential ones adult-child caregivers make around POA. Each is correctable — but only before the capacity window closes.

- Waiting until after a diagnosis to start the process. A diagnosis creates urgency — it does not eliminate the option. But waiting further, hoping the situation stabilizes, risks losing the window entirely. Act on a diagnosis, not after the next decline event.

- Assuming a dementia diagnosis bars signing. It does not automatically. A parent in early-stage dementia may still have legal capacity. Consult an elder law attorney immediately to assess whether a valid POA can still be executed.

- Believing one document covers both healthcare and financial decisions. In most states, these are two separate documents with separate requirements. Having a financial POA does not give an agent authority to make medical decisions, and vice versa.

- Failing to notify financial institutions and healthcare providers. A POA document sitting in a drawer is not the same as a POA that institutions know about and have accepted. Proactive distribution and confirmation of acceptance is essential.

- Not verifying that HIPAA language is current. An older healthcare POA may not contain the HIPAA authorization language that current providers require. Have an elder law attorney review the document and update it if needed.

- Not discussing the agent role with the chosen person in advance. Being named as an agent is a significant legal and personal responsibility. The person should understand what they are agreeing to, where the document is kept, and what the principal's wishes are — before a crisis, not during one.

- Assuming a general (non-durable) POA is sufficient. A general POA without durable language terminates at incapacity. If an existing document does not contain explicit durable language, it will not protect the family when it is needed most.

Quick-Reference FAQ

- Can I get a POA for my parent without their consent? No. A POA cannot be created for someone else or over someone else. The principal must initiate the process and sign voluntarily while mentally competent. If your parent lacks capacity, the only legal option is court-supervised guardianship or conservatorship.

- Does a dementia diagnosis prevent my parent from signing a POA? Not automatically. Legal capacity is assessed at the time of signing based on whether the person understands the document's implications — not based on a diagnosis alone. A parent in early-stage dementia may retain sufficient capacity. An elder law attorney can advise, and a physician can document capacity at signing as a protective measure.

- Does POA give me authority to override my parent's decisions? No. A POA agent's authority to make decisions on the principal's behalf only activates when the principal lacks the capacity to make those decisions themselves. While the principal retains legal capacity, they retain the right to make their own decisions — the agent cannot override them.

- What is the difference between a healthcare POA and a living will? A healthcare POA appoints a named person to make medical decisions when the principal cannot communicate. A living will documents the principal's specific wishes about life-sustaining treatment in defined situations — but does not appoint a decision-maker. Both are typically needed together for complete advance care planning.

- Does a POA expire? A durable POA remains valid from signing until the principal dies or revokes it, unless the document itself specifies an expiration date. A limited POA may expire when its specified task is completed or its time period ends. The principal can revoke a POA at any time while they retain legal capacity.

- Who should I choose as agent? The agent should be someone the principal trusts completely, who is organized and capable of handling the relevant responsibilities, who is willing to take on the fiduciary obligation, and who is likely to be available and reachable when decisions need to be made. Geographic proximity matters for financial POA tasks. Discuss the role with the person before naming them — do not name someone without their knowledge and agreement.

Browse more in the Glossary.