Glossary entry

Skilled Nursing Facility (SNF): What It Is and When Medicare Covers It

What Is a Skilled Nursing Facility (SNF)?

A skilled nursing facility is a Medicare-certified care setting where patients receive short-term, medically necessary nursing and rehabilitation services following a hospital stay. The emphasis is on short-term recovery — physical therapy after a hip replacement, wound care after surgery, or IV antibiotic treatment that cannot safely be managed at home.

SNFs can be operated as standalone facilities, as dedicated wings within a larger nursing home, or as hospital-based units. This is where the confusion most often arises: a patient may be placed in what looks and feels like a nursing home — the same building, the same hallways — but be occupying an SNF bed under a legally and financially distinct Medicare benefit. The care type, the coverage rules, and the billing are entirely different from long-term residential nursing home care.

The distinction matters enormously at the moment of hospital discharge. When a discharge planner says your parent is being transferred to "skilled nursing," they mean a Medicare-covered, time-limited rehabilitation stay — not a permanent placement. Understanding that difference is the first step to navigating the coverage rules correctly.

Services an SNF Provides

An SNF provides a range of medical and rehabilitative services that require licensed professionals to deliver or supervise. These are not services a family member could provide at home without clinical training.

- Skilled nursing care by registered nurses (RNs) and licensed practical nurses (LPNs), including complex wound care and post-surgical monitoring

- Physical therapy (PT) to restore mobility and strength, such as walking rehabilitation after a fracture

- Occupational therapy (OT) to rebuild the ability to perform daily tasks like dressing, bathing, and meal preparation

- Speech-language therapy for swallowing difficulties, communication impairments, or cognitive rehabilitation

- Intravenous (IV) medications and injections that require clinical administration

- Medication management, including monitoring for interactions and side effects

- Medical social services for discharge planning and community resource coordination

- Dietary counseling and nutritional support

- Medical supplies and equipment used during the SNF stay, such as catheters, splints, and dressings

- A semi-private room and meals for the duration of the covered stay

All of these services are provided with the goal of enabling the patient to return home or transition to a lower level of care. The SNF benefit is not designed for indefinite residential care.

Skilled Care vs. Custodial Care: Why the Distinction Determines Coverage

Medicare's SNF benefit covers only skilled care — services so medically complex that they require a licensed nurse or therapist to deliver or closely supervise. It does not cover custodial care — help with everyday activities like bathing, dressing, eating, or getting in and out of bed when that help does not require a licensed professional.

This boundary is the single most common source of wrongful SNF denials. A patient who needs help dressing every morning but does not need a nurse to manage wounds or a therapist to rebuild mobility may be told their care is custodial and therefore not covered. That determination is sometimes correct — and sometimes not.

| Skilled Care (Medicare may cover) | Custodial Care (Medicare does not cover on its own) |

|---|---|

| Wound care requiring sterile technique and clinical assessment | Assistance with bathing and grooming |

| IV antibiotic administration and monitoring | Help with dressing and undressing |

| Physical therapy to restore gait and balance after a fracture | Assistance with eating meals |

| Observation and management of an unstable medical condition | Routine assistance getting in and out of bed |

| Speech therapy for post-stroke swallowing dysfunction | Companionship and supervision |

| Skilled nursing oversight of a complex medication regimen | Reminders to take medications already set up by a nurse |

When Medicare Part A Covers SNF Care: The Five Eligibility Conditions

All five conditions below must be met for Medicare Part A to cover an SNF stay. If any one condition is not met, Medicare will not pay — and the financial exposure is significant.

- Active Part A enrollment with benefit period days remaining. The patient must be enrolled in Medicare Part A and must have available days in the current benefit period. A benefit period begins on the day a patient is admitted to a hospital or SNF and ends after 60 consecutive days outside both settings.

- A qualifying 3-day inpatient hospital stay. The patient must have been formally admitted as an inpatient to a hospital for at least three consecutive days. The admission day counts; the discharge day does not. Time spent in the emergency room or under observation status does not count toward this requirement.

- SNF admission within 30 days of hospital discharge. The patient must enter the SNF within 30 days of being discharged from the qualifying hospital stay. A gap longer than 30 days breaks the connection and eliminates SNF coverage eligibility for that stay.

- Physician-ordered daily skilled care. A physician must certify that the patient requires skilled nursing services seven days per week, or skilled therapy services at least five days per week. This is the "daily skilled care" threshold.

- Care in a Medicare-certified SNF for a covered condition. The SNF must be Medicare-certified, and the care must be for a condition that was treated during the qualifying hospital stay — or for a new condition that arises while the patient is already receiving covered SNF care.

The 3-Day Inpatient Rule and the Observation-Status Trap

Observation status is one of the most consequential — and least understood — billing designations in Medicare. A hospital can classify a patient as an outpatient "under observation" even during a multi-day stay that looks, from the patient's perspective, identical to an inpatient admission: the same bed, the same nurses, the same meals. But the billing category is entirely different.

Observation stays are billed under Medicare Part B, not Part A. They do not count toward the 3-day inpatient requirement for SNF coverage. Neither does time spent in the emergency room before admission. The discharge day itself also does not count. A patient who spends four nights in the hospital but was classified as observation for two of them may have only two qualifying inpatient days — one short of the threshold.

The Alexander v. Becerra class action, litigated by the Center for Medicare Advocacy, established the right for certain Medicare beneficiaries to appeal their observation status classification. A retrospective appeal deadline of January 2, 2026 applied to prior claims — that window has now closed for past stays. However, forward-going appeal rights remain in effect: beneficiaries who believe they were incorrectly classified as observation during a current or recent hospital stay may still challenge that designation.

- On the day of admission, ask the admitting nurse or patient services representative: "Is my family member admitted as an inpatient or under observation?"

- If the answer is observation, ask the attending physician whether inpatient admission is medically appropriate and request that the status be changed if it is.

- Watch for the MOON notice — if it arrives, read it carefully and keep a copy.

- Contact your State Health Insurance Assistance Program (SHIP) counselor for free guidance on appealing observation status classifications.

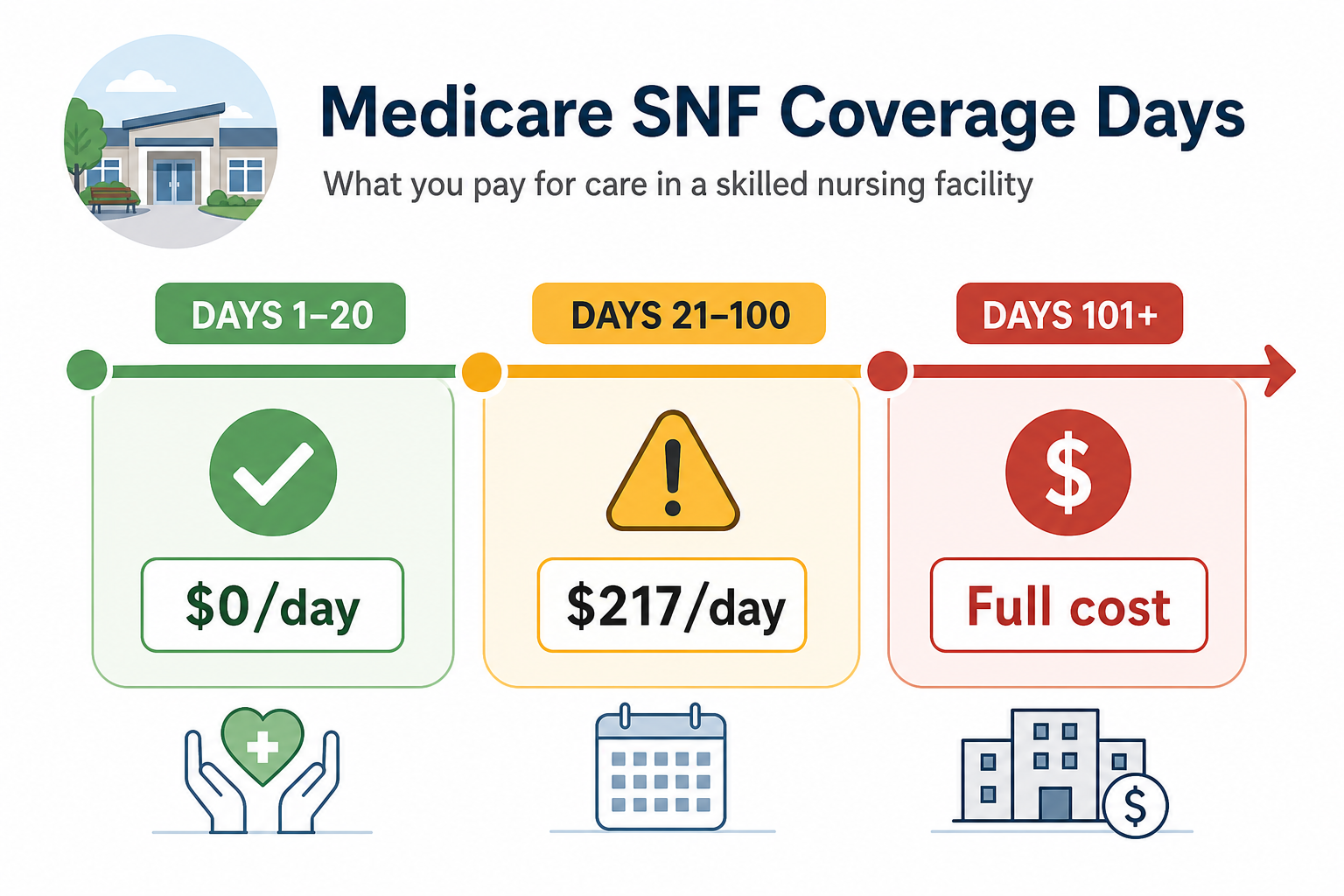

2026 Medicare SNF Cost Structure

Medicare SNF costs in 2026 follow a three-tier structure tied to the length of the stay within a single benefit period. Understanding this timeline before discharge prevents financial surprises.

| Coverage Period | Daily Cost to Patient (2026) | Notes |

|---|---|---|

| Days 1–20 | $0 per day | Covered in full after the $1,736 Part A deductible. If the deductible was already paid during the qualifying hospital stay in the same benefit period, no additional deductible applies. |

| Days 21–100 | $217 per day | Patient pays this coinsurance amount each day. Medigap plans (C, D, F, G, M, N) typically cover this cost for Original Medicare beneficiaries. |

| Days 101 and beyond | All costs | Medicare Part A coverage ends. Patient is responsible for the full daily rate, which varies by facility. |

The benefit period concept is equally important. A benefit period begins when a patient is admitted to a hospital or SNF and ends after 60 consecutive days outside both settings. Once a benefit period closes, a new one can begin — but only after a new qualifying 3-day inpatient hospital stay. A new benefit period brings a new 100-day SNF allotment and a new Part A deductible.

What Medicare Does NOT Cover in an SNF

Even when a patient is in a Medicare-covered SNF stay, certain costs and services fall entirely outside the benefit.

- Long-term custodial care. Medicare does not pay for ongoing residential care in a nursing home. Once the need for daily skilled care ends, Medicare SNF coverage ends — regardless of whether the patient still needs help with daily activities.

- A private room, unless a physician certifies that a private room is medically necessary (for example, for infection control).

- Personal convenience items such as a television, telephone service, or personal toiletries beyond basic necessities.

- Care that no longer meets the daily skilled-care threshold. If the patient's condition stabilizes and the physician cannot certify that daily skilled nursing or therapy is still required, Medicare coverage stops — even if the patient remains in the SNF building.

- Assisted living and memory care. These are separate care settings, not SNFs, and are not covered by Medicare Part A regardless of the level of care provided.

When Medicare Stops Paying: Medigap, Medicare Advantage, and Medicaid

The $217/day coinsurance for days 21–100 adds up quickly — up to $17,360 over that period if the stay runs its full course. Several coverage options can offset this cost, but each comes with its own rules.

For beneficiaries on Original Medicare, Medigap (Medicare Supplement Insurance) plans C, D, F, G, M, and N typically cover the days 21–100 coinsurance. The specific amount covered varies by plan letter — some cover the full coinsurance, others cover a portion. Medigap plans must be verified with the insurer before relying on this coverage.

For patients who exhaust Medicare SNF coverage and have limited financial resources, Medicaid may cover ongoing nursing home care for those who qualify. Medicaid eligibility and SNF coverage rules vary significantly by state. Contact your state Medicaid office or a SHIP counselor for guidance specific to your situation — Medicaid SNF rules are complex enough to warrant separate, individualized guidance.

Appealing an SNF Coverage Denial

SNF coverage denials occur with significant frequency, and many are wrongful. Caregivers who understand their appeal rights — and assert them — can often reverse incorrect coverage terminations.

The Jimmo Maintenance Standard

One of the most important — and most frequently misapplied — Medicare coverage rules is the maintenance standard established by the Jimmo v. Sebelius settlement (2013). Under this settlement, CMS clarified that Medicare must cover skilled nursing and therapy services when a patient needs skilled care to maintain their current condition or prevent or slow further decline — not only when measurable improvement is expected.

"The Jimmo Settlement Agreement may reflect a change in practice for those providers, adjudicators, and contractors who may have erroneously believed that the Medicare program covers nursing and therapy services under these benefits only when a beneficiary is expected to improve."

Despite being legally established, the maintenance standard is inconsistently applied by individual SNFs and Medicare contractors. If a denial letter implies that coverage is ending because the patient has "plateaued" or is "not making progress," that reasoning may be legally incorrect under Jimmo. Caregivers should not accept this framing without challenge.

The Expedited Review Right

Before an SNF can terminate Medicare coverage, it must issue a written Notice of Medicare Non-Coverage to the patient. This notice triggers the right to a fast-track review by a Quality Improvement Organization (QIO) — an independent reviewer contracted by Medicare. The patient does not have to leave the SNF or begin paying out of pocket while the expedited review is pending.

- When you receive the Notice of Medicare Non-Coverage, read it carefully and note the deadline for requesting an expedited review — it is typically the day before coverage is scheduled to end.

- Contact the QIO listed in the notice to request a fast-track review. This can often be done by phone.

- If the SNF refuses to submit a claim to Medicare, you can demand that it do so. The patient is not required to pay the SNF directly until Medicare officially processes and denies the claim.

- Contact a SHIP counselor for free, unbiased assistance navigating the appeal process. SHIP counselors are trained Medicare specialists and do not represent any insurance company or facility.

Related Glossary Terms

- Benefit period: The span of time during which Medicare Part A pays for hospital and SNF care; it begins on the day of inpatient admission and ends after 60 consecutive days outside a hospital or SNF. Each benefit period carries its own Part A deductible and 100-day SNF allotment.

- Custodial care: Non-medical assistance with activities of daily living — bathing, dressing, eating, toileting, transferring — that does not require a licensed professional to deliver. Medicare does not cover custodial care on its own.

- Medigap: Private supplemental insurance that fills gaps in Original Medicare coverage, including the SNF coinsurance for days 21–100. Also called Medicare Supplement Insurance. Plan letters C, D, F, G, M, and N include SNF coinsurance coverage.

- Part A deductible: The amount a Medicare beneficiary pays before Part A hospital or SNF benefits begin in a benefit period. In 2026, the Part A deductible is $1,736. It applies once per benefit period, not once per year.

Browse more in the Glossary.