Caregiver decision guide

How to Pay for a PERS Medical Alert System: Medicare, Medicaid, VA, and Other Coverage Options

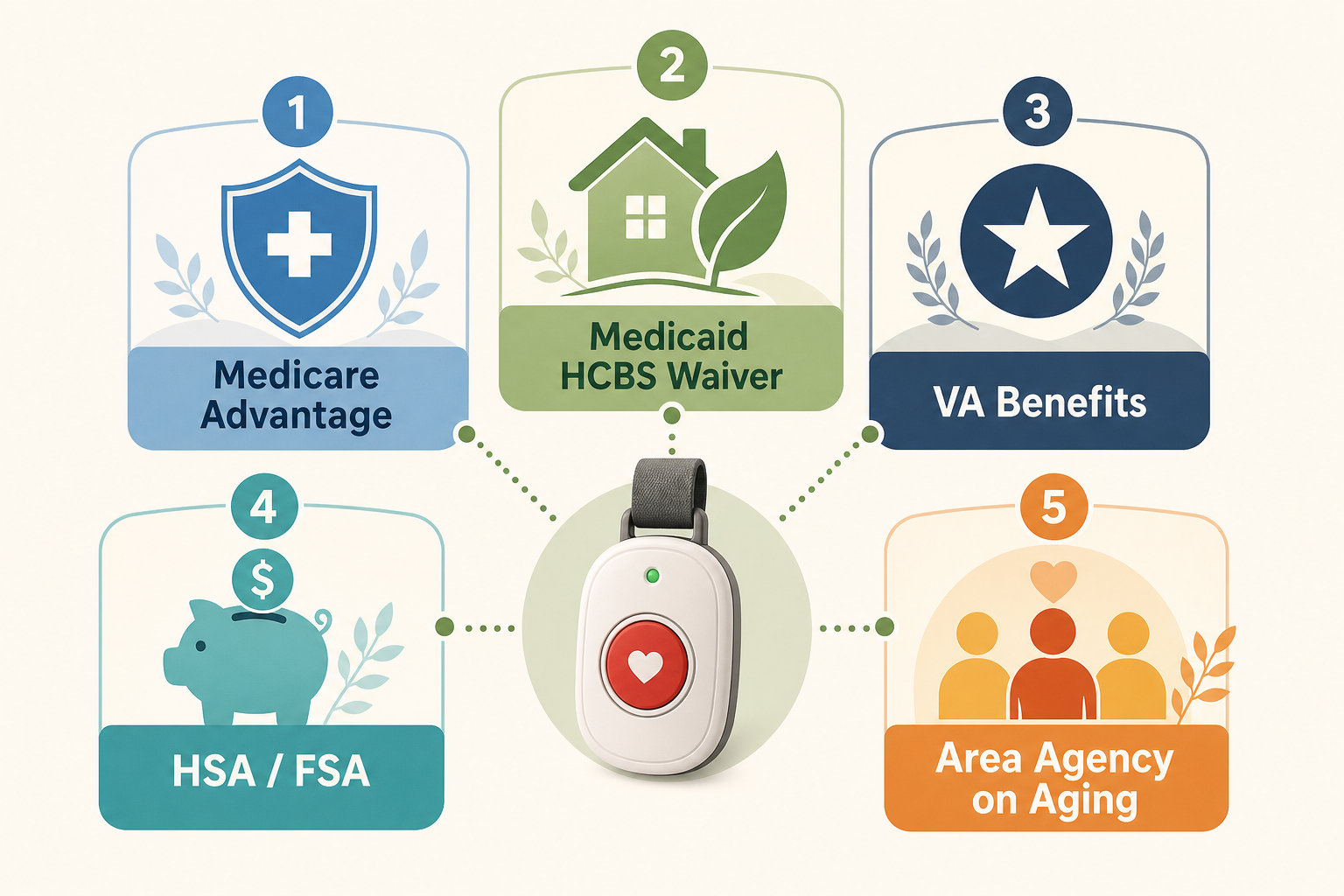

Most families assume personal emergency response systems are a full out-of-pocket expense, but a layered set of coverage pathways — including Medicaid HCBS waivers, Medicare Advantage supplemental benefits, VA programs, and HSA/FSA accounts — can substantially reduce or eliminate PERS costs for eligible seniors. This guide explains each pathway clearly and provides a step-by-step checklist for exploring every option before paying full price.

What PERS Devices Actually Cost: Monthly Fees, Equipment, and Add-Ons

Understanding the full cost picture is the first step toward finding ways to reduce it. PERS costs fall into three categories: monthly monitoring fees, upfront equipment costs, and optional add-on features.

| Cost Component | Typical Range | Notes |

|---|---|---|

| Monthly monitoring fee | $20–$60/month | The ongoing subscription to a 24/7 response center; required for all monitored systems |

| One-time equipment fee | $0–$200 | Some providers charge for the device itself; others include it with a contract |

| Automatic fall detection add-on | $5–$12/month | Optional sensor that detects falls without pressing the button; billed on top of base monitoring fee |

| GPS/mobile service add-on | $5–$15/month | For mobile PERS units that work outside the home; requires cellular data plan |

| Annual total (base monitoring only) | $240–$720/year | Equipment cost additional in year one; ongoing fee continues annually |

For a senior living on Social Security alone — roughly 35% of Social Security beneficiaries rely on it as their primary income source — a $300–$900 annual PERS cost represents a meaningful financial barrier. That barrier is real, but it is not fixed. Several coverage pathways can substantially reduce or eliminate these costs for eligible individuals.

Original Medicare (Parts A and B): Why PERS Is Not Covered

This is one of the most common misconceptions families encounter. Original Medicare — Parts A (hospital) and B (medical) — does not cover personal emergency response systems.

The reason is categorical: Medicare Part B covers durable medical equipment (DME) such as wheelchairs, walkers, and oxygen equipment. PERS devices do not meet the DME classification under current Medicare rules. They are not prescribed as medically necessary equipment in the same way, and the monitoring service component — which is the ongoing cost — falls entirely outside Medicare's covered services framework.

The gap in original Medicare coverage is precisely why the pathways described below — Medicare Advantage, Medicaid HCBS waivers, VA programs, and others — are worth pursuing systematically.

Medicare Advantage (Part C): Supplemental Benefits That May Cover PERS

Medicare Advantage plans — private insurance plans that provide Medicare benefits — are permitted to offer supplemental benefits beyond original Medicare. PERS coverage is one of those optional supplemental benefits, and a growing number of plans have added it in recent years.

Coverage varies significantly from plan to plan and changes annually with the Medicare Advantage bid cycle. One plan may cover the monitoring fee entirely; another may offer a partial monthly credit; a third may not include PERS at all. There is no uniform standard.

To find out whether a specific Medicare Advantage plan covers PERS, take the following steps:

- Locate the plan's Annual Notice of Change (ANOC) or Evidence of Coverage (EOC) document — these are mailed each fall and list all covered supplemental benefits for the coming year.

- Search the document for terms including "personal emergency response," "PERS," "medical alert," "home safety," or "supplemental health benefit."

- Call the plan's member services number (on the back of the insurance card) and ask directly: "Does my plan cover personal emergency response systems or medical alert devices? If so, what is covered and what is the process to access that benefit?"

- Request a coverage determination in writing if the representative confirms coverage. This protects against verbal misrepresentations and documents the benefit for reimbursement purposes.

- If the current plan does not cover PERS, note this for the next Medicare Open Enrollment period (October 15 – December 7 each year), when switching to a plan that does include PERS coverage becomes an option.

Medicaid HCBS Waivers: The Largest Coverage Pathway for Low-Income Seniors

For seniors who qualify for Medicaid, Home and Community-Based Services (HCBS) waivers represent the most substantial PERS coverage pathway available. Most states cover PERS under HCBS waivers as a "personal emergency response service" — a recognized category of home-based support that helps seniors remain safely in their own homes rather than moving to institutional care.

HCBS waivers are state-administered programs that operate under federal Medicaid rules. Each state designs its own waiver programs, which means eligibility criteria, covered services, and reimbursement rates vary. However, PERS is a commonly included service across many state waiver programs.

Typical reimbursement under Medicaid HCBS waivers includes a one-time installation or startup fee (roughly $40–$200) and an ongoing monthly service fee (roughly $25–$75/month), though these figures vary by state and are subject to change. The covered amount generally corresponds to a standard PERS unit; higher-feature systems may require the beneficiary to pay the difference.

- Eligibility for HCBS waiver services typically requires meeting both financial and functional criteria — meaning income and asset limits apply, and the individual generally must demonstrate a level of care need consistent with nursing facility eligibility.

- Waiver programs often have enrollment caps and waiting lists. Applying as early as possible — even before a PERS is urgently needed — is advisable.

- To find your state's HCBS waiver programs, contact your state Medicaid office directly or ask a local Area Agency on Aging to help identify which waivers include PERS coverage.

- Consumer-directed Medicaid programs in some states allow beneficiaries to select their own PERS provider and, in some cases, choose a higher-feature system (such as one with GPS or fall detection) if the cost offsets other Medicaid-covered services they choose not to use.

VA Programs: PERS Access for Eligible Veterans

Veterans enrolled in VA healthcare may be able to access PERS devices at no cost or significantly reduced cost through VA programs, depending on their service-connected disability rating, clinical need, and the specific VA medical center they use.

The VA does not have a single national PERS program with uniform eligibility rules. Access is typically initiated through a veteran's VA primary care provider, who assesses clinical need and can write a referral or order for the device if it is clinically justified. The process works best when the caregiver or veteran comes to the appointment prepared.

- Contact the veteran's VA primary care provider and request an appointment specifically to discuss fall risk and home safety needs.

- Ask the provider directly: "Can you document a clinical need for a personal emergency response system and initiate a referral through the VA?"

- If the primary care provider is not familiar with PERS coverage, ask to speak with the VA social worker or care coordinator assigned to the veteran's care team — they are often the most knowledgeable about available assistive technology programs.

- Veterans with higher service-connected disability ratings generally have access to a broader range of VA-covered assistive devices, so confirming the veteran's current disability rating before the appointment is useful.

- If VA-provided PERS is not available or the wait is long, ask whether the VA can refer the veteran to a community care provider who participates in VA-funded programs.

Area Agencies on Aging and Nonprofit Assistance Programs

Beyond federal programs, a network of local resources exists specifically to help older adults access safety equipment like PERS. Area Agencies on Aging (AAAs) are the primary gateway to this network.

The Eldercare Locator, operated by the U.S. Administration on Aging, connects callers and website visitors to their local AAA. AAAs maintain current information about local PERS financial assistance programs, which may include sliding-scale subsidies, one-time equipment grants, or connections to nonprofit organizations that donate or loan PERS devices.

- The Eldercare Locator (eldercare.acl.gov) can be reached online or by phone at 1-800-677-1116. Provide the senior's zip code to be connected to the appropriate local AAA.

- When contacting the AAA, ask specifically: "Are there any local programs that help cover the cost of a personal emergency response system or medical alert device for a senior on a fixed income?"

- PACE (Program of All-Inclusive Care for the Elderly) is another pathway for eligible seniors — those who are 55 or older, certified as needing nursing facility-level care, and living in a PACE service area. PACE covers a comprehensive range of services including home safety equipment, and PERS may be included as part of an individual's care plan.

- Some state-funded senior assistance programs — separate from Medicaid — also include PERS coverage. AAAs are the most reliable local source for identifying these programs, as availability varies widely by county and state.

HSA and FSA Accounts: Using Pre-Tax Dollars for PERS

Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA) offer a tax-advantaged way to pay for PERS costs — but eligibility depends on having the right type of health coverage and, in most cases, documentation of medical need.

The IRS generally allows HSA and FSA funds to be used for medical devices and services that are primarily for the diagnosis, treatment, or prevention of disease. PERS devices can qualify when a licensed medical professional has documented that the device is medically necessary — for example, due to fall risk, a cardiac condition, or a history of medical emergencies.

- HSA eligibility requires enrollment in a qualifying high-deductible health plan (HDHP). Funds can be used for qualified medical expenses including PERS when medical necessity is documented.

- FSA accounts are employer-sponsored and do not require an HDHP. However, FSA funds are use-it-or-lose-it within the plan year (with some grace period exceptions), so timing matters.

- To use HSA or FSA funds for PERS, request a Letter of Medical Necessity (LMN) from the senior's primary care provider. The letter should state the medical condition, why the PERS device is medically necessary, and the expected duration of need.

- Keep all receipts for PERS equipment and monitoring fees. Submit for reimbursement through the HSA or FSA administrator with the LMN attached. Some administrators may require the PERS provider's itemized invoice as well.

- Not all HSA/FSA administrators interpret PERS eligibility the same way. If a claim is denied, ask the administrator to specify the reason and whether a Letter of Medical Necessity would change the determination.

Other Ways to Reduce PERS Costs

Even when formal coverage programs are not available or pending, several practical strategies can meaningfully reduce what a family pays out of pocket.

- Prepayment discounts: Many PERS providers offer a reduced rate — sometimes 10–20% off — when the annual monitoring fee is paid upfront rather than monthly. If cash flow allows, this is one of the simplest ways to lower the total annual cost.

- Free trial periods: A number of providers offer 30-day free trials. Using a trial period to confirm the device meets the senior's needs before committing to a full contract reduces the risk of paying for a device that gets abandoned.

- AARP member discounts: AARP has negotiated discounts with certain PERS monitoring service categories. Check current AARP member benefits for applicable offers, as these change periodically.

- Sliding-scale programs: Some nonprofit PERS providers and monitoring centers offer income-based sliding-scale pricing for seniors who do not qualify for Medicaid but still face financial hardship. Ask any provider directly whether they have a financial hardship or reduced-rate program.

- Seasonal promotions: PERS providers frequently run promotional pricing around fall (September–November) and the winter holidays. If a purchase is not urgent, timing it around these windows can reduce equipment and first-month costs.

- No-contract plans: Avoiding long-term contracts preserves flexibility to switch providers if a better-priced option becomes available or if a coverage program is approved. Month-to-month plans typically cost slightly more per month but reduce the risk of being locked into a higher rate.

Step-by-Step Action Checklist: Exploring Every Coverage Option

Work through these steps in order before committing to full out-of-pocket payment. The steps are sequenced by effort and likelihood of yielding coverage.

- Check Medicare Advantage plan documents. Locate the Evidence of Coverage or Annual Notice of Change for the senior's Medicare Advantage plan. Search for "personal emergency response," "PERS," or "medical alert." If coverage is listed, call member services to confirm the process and request a coverage determination in writing.

- Contact the state Medicaid office. If the senior has or may qualify for Medicaid, ask about HCBS waiver programs that include personal emergency response services. Request information on eligibility criteria, current enrollment status (including any waiting lists), and how to apply.

- Use the Eldercare Locator. Visit eldercare.acl.gov or call 1-800-677-1116 to reach the local Area Agency on Aging. Ask about local PERS financial assistance programs, sliding-scale options, and whether the senior may qualify for PACE.

- Contact the VA if the senior is a veteran. Schedule an appointment with the VA primary care provider to discuss fall risk and request a referral for a PERS device. Ask to speak with the VA social worker if the primary care provider is unfamiliar with the process.

- Check HSA or FSA eligibility. Determine whether the senior or their spouse has an active HSA or FSA. If so, request a Letter of Medical Necessity from the primary care provider and submit for reimbursement after purchase.

- Ask the PERS provider about hardship or sliding-scale programs. Before signing any agreement, ask directly whether the provider offers income-based pricing, nonprofit rates, or any other cost-reduction programs.

- Apply cost-reduction strategies for any remaining out-of-pocket cost. If some cost remains after exhausting coverage options, evaluate prepayment discounts, free trial periods, AARP member benefits, and month-to-month versus annual contract pricing.

Questions to bring to a clinician or OT

This is not medical, legal, or a family's final decision — only a framework. Bring these questions to a clinician, occupational therapist, or your local Area Agency on Aging.

Find Local HelpRelated reading

Noticed something outdated or inaccurate on this page? Flag a correction. We review every report against CDC, NIA, and AARP HomeFit guidance before updating a page.