How to Choose the Right Care for an Elderly Person at Home

For: adult childReviewed: 2026-07-09

How to Choose the Right Care for an Elderly Person at Home

New to caring for an elderly parent at home? This guide walks you through the types of in-home care, typical costs, the decision between an agency and a private caregiver, and the first steps to get started without a costly mistake.

By Editorial Team

new caregiver

experienced caregiver

long-distance caregiving

spousal caregiver

working caregiver

daily routines

medication management

personal hygiene

care coordination

first steps

ADLs

IADLs

The first hard moment is usually not a medical crisis. It is smaller and more ordinary: a parent has skipped meals, mixed up pills, stopped showering regularly, or become nervous about being alone. Someone in the family types “care for elderly at home” into a search bar, and suddenly every result seems to use the same phrase for very different kinds of help.

That distinction matters before prices, provider names, or availability. A companion cannot safely be treated as a nurse. A home health visit is not the same thing as someone staying through dinner. A home care aide may be exactly right for bathing and meal support, but not for wound care or medication changes. The first decision is not “Who can come tomorrow?” It is “What tasks actually need to be covered, and what level of care is allowed to do them?”

Most families are not unusual for wanting to make home work if it can be made safe. Pew Research Center reported in 2026 that 93% of adults ages 65 and older live in their own homes, and 60% of older adults who live at home said they would want to stay there with a caregiver rather than move if they could no longer manage independently. The same Pew report found that only 21% of adults 65 and older have long-term care insurance, which is one reason the cost question becomes real very quickly. [1]

The uncertainty is normal, too. In a widely cited NAC and AARP caregiver study summarized by Family Caregiver Alliance, 84% of family caregivers said they needed more information on at least 14 specific topics; the top two were keeping their loved one safe and managing their own stress, each named by 42%. [2] A care plan should reduce that stress, not quietly move all of the coordination work onto one overwhelmed daughter, son, spouse, or sibling.

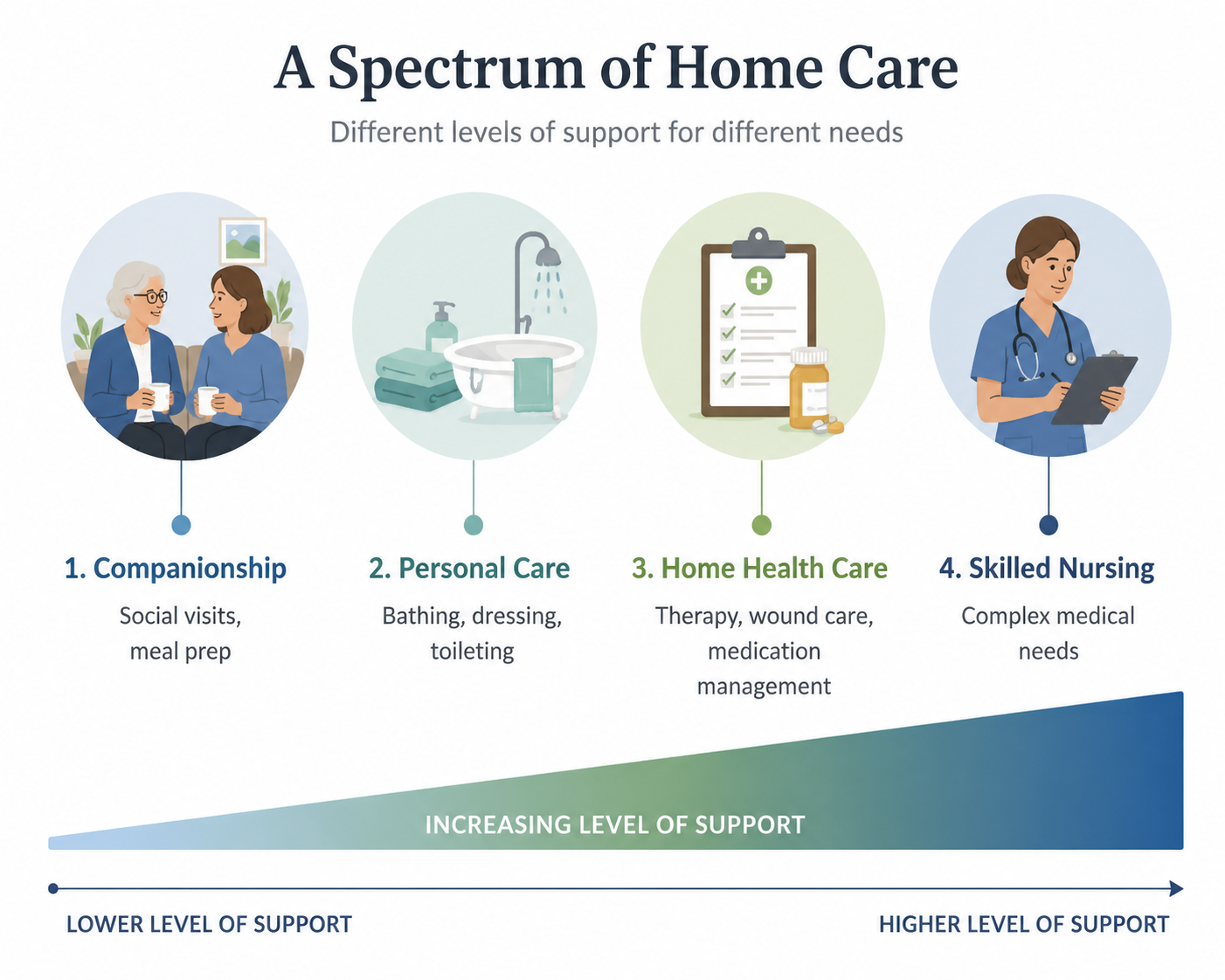

Start with the care-type spectrum

“Home care” is often used as an umbrella term, but families usually need to separate it into four practical levels. The boundaries are not just vocabulary. They determine who can be hired, what the caregiver can do, how much the plan may cost, and whether insurance or Medicare is even relevant.

Care type

Best fit

Common tasks

Important boundary

Companionship

A parent is mostly independent but lonely, forgetful, or unsafe alone for stretches of the day.

A family meeting that begins with “Mom needs help” often goes in circles. One person imagines a friendly visitor. Another imagines a trained aide. Someone else assumes Medicare will send a nurse. The cleaner starting point is a written list of what is actually happening during the week.

Separate the list into daily living tasks, household tasks, safety concerns, and medical concerns. This is where activities of daily living, often called ADLs, and instrumental activities of daily living, or IADLs, become useful. They are not paperwork for its own sake; they keep the family from hiring for the wrong problem.

ADLs: bathing, dressing, grooming, toileting, eating, moving from bed to chair, and walking safely.

Safety concerns: falls, wandering, missed meals, stove use, confusion at night, unsafe driving, or being unable to respond in an emergency.

Medical concerns: wound care, injections, medication changes, new symptoms, therapy needs, post-hospital instructions, or equipment that requires trained monitoring.

The phrase “lowest safe level” is deliberate. It does not mean the cheapest person available. It means not overbuying clinical care for social support, and not underbuying non-medical help when a parent needs hands-on assistance.

When companionship may be enough

Companionship can be a good fit when the parent is still physically able to bathe, dress, eat, and use the bathroom independently, but the day has become too thin or too risky. Maybe meals are skipped because cooking feels like too much. Maybe appointments are missed. Maybe the family caregiver is calling three times a day just to make sure everything is all right.

A companion can make lunch, drive to the grocery store, sit during a few vulnerable hours, notice that the refrigerator is empty, and tell the family if something seems different. That last part matters. Observation is often the quiet value of early help at home.

When personal care is the real need

If bathing, toileting, dressing, grooming, transfers, or fall-risk support are the problem, the family is usually beyond companionship. This is where a home care aide or personal care aide may fit. The work is intimate, physical, and trust-heavy. It also needs enough hours to cover the moments when help is actually needed, not just the hours that are easiest to schedule.

For example, a parent who needs help showering and dressing may need morning coverage, not a convenient afternoon visit. A parent who becomes confused after dinner may need evening coverage, even if the family would rather not pay for that time. Matching care to the actual day prevents a common waste: paying for help that arrives after the hardest part is already over.

When home health care or skilled nursing belongs in the plan

Medical needs should not be pushed onto a non-medical caregiver because the family likes the caregiver, wants fewer people involved, or is trying to control cost. If a parent needs wound care, injections, skilled monitoring, therapy after hospitalization, or care ordered by a clinician, ask the physician what level of home health or nursing service is appropriate.

Home health care and personal home care can exist at the same time. A nurse or therapist may visit intermittently for clinical tasks, while a non-medical aide helps with bathing, meals, and supervision. Families sometimes expect one service to cover both. That expectation creates gaps.

Estimate hours before comparing prices

Hourly rates only become useful after the family has a rough weekly schedule. Three mornings a week is a different decision from every evening. Overnight supervision is different from a two-hour shower-and-breakfast visit. A parent recovering from surgery may need a short-term burst of help, while dementia-related supervision may grow over time.

For 2026 planning, A Place for Mom reports a national median of $34 per hour for in-home care, while SeniorLiving.org reports $35 per hour. The difference is small enough to treat as a planning range rather than a contradiction; cost sources use different data windows, provider samples, and geographic weighting. Both sources also show that state and skill level matter. A Place for Mom reports non-medical home care ranging from $25 to $44 per hour depending on state, and SeniorLiving.org places skilled nursing at roughly $50 to $75 per hour. [3][4]

Scenario

Example schedule

What to price

Light support

A few short visits each week

Companionship, errands, meal help, check-ins.

Daily personal care

Morning or evening coverage most days

Hands-on bathing, dressing, transfers, meals, and safety support.

Home health services or skilled nursing, plus any separate non-medical care.

Do not stop at the hourly number. Ask whether there is a minimum shift length, weekend differential, holiday rate, assessment fee, care-management fee, cancellation policy, mileage charge, or higher rate for more complex care. A lower hourly rate can become less useful if the schedule is rigid or backup coverage is weak.

Agency or private caregiver: decide who will run the system

The agency-versus-private choice is not simply “expensive” versus “affordable.” It is a decision about who handles the operating work. Someone has to screen the caregiver, confirm skills, manage schedules, handle pay, cover sick days, respond when the match is not working, and replace the person if they leave.

What an agency usually buys

A home care agency typically costs more because it is not only selling caregiver time. It is also providing screening, payroll administration, scheduling, supervision, liability coverage, care-plan setup, and backup staffing. Quality still varies, and families should still interview carefully. But when an aide is sick, quits, or is not a good fit, the agency is supposed to have a process.

That structure can be worth paying for when the family caregiver works full time, lives far away, is already exhausted, or cannot become the dispatcher every time a shift changes. It can also help when the parent’s needs are likely to increase and the schedule may need to change quickly.

What private hiring shifts onto the family

Private caregivers may cost 20% to 30% less than agency care, according to A Place for Mom, but the family takes on employer responsibilities such as background checks, payroll taxes, scheduling, and backup coverage. [5] That discount can be real. It is not automatically a bargain.

Private hiring can work well when the family has time, organization, local backup, and a clear plan for taxes and supervision. It can be risky when everyone assumes someone else is checking references, arranging coverage, or making sure the caregiver is paid legally. The hidden labor usually lands on the most responsive family member, not the one who argued most strongly for the cheaper option.

Question

Agency care

Private caregiver

Who screens the caregiver?

The agency should screen and assign caregivers.

The family must verify identity, references, background, and fit.

Who handles payroll and taxes?

Usually the agency.

The family must handle or outsource employer obligations.

Who covers sick days?

The agency should arrange backup, though availability varies.

The family must have a backup plan.

Who changes the schedule?

The agency coordinates changes within its policies.

The family negotiates directly and finds replacements if needed.

Who supervises quality?

The agency may provide oversight and care-plan review.

The family must observe, document concerns, and manage performance.

If this choice is the main sticking point, read How to Choose Between a Home Care Agency and a Private Caregiver before committing. The right answer depends less on family philosophy and more on who can reliably manage the work that happens after the first good interview.

Check payment limits before assuming coverage

Payment rules are where many families lose time. Medicare may cover certain medically necessary home health services when eligibility rules are met, but it does not cover custodial or non-medical home care such as ongoing help with bathing, dressing, meals, housekeeping, or supervision by itself. The National Institute on Aging states this distinction plainly in its guidance on services for older adults living at home. [6]

That does not mean there are no payment paths. It means the path depends on the kind of care, the parent’s insurance, income and assets, veteran status, state programs, long-term care insurance if they have it, and whether the need is medical or custodial. For a fuller payment walkthrough, use What Will Pay for Senior Home Healthcare in 2026?.

Make the first calls with a specific plan

Once the family has named the care type, estimated hours, and decided whether agency or private hiring is realistic, the first calls become much more productive. The goal is not to sound like an expert. It is to give enough detail that the provider cannot slide into a generic sales script.

Write down the parent’s ADL, IADL, safety, and medical needs.

Mark which needs are non-medical and which require clinical review.

Draft the actual weekly schedule: mornings, evenings, overnights, weekends, transportation, and caregiver respite.

Ask agencies or private candidates what tasks they can and cannot perform under state rules and their own policies.

Request the full rate structure, including minimum shifts, weekend rates, cancellations, and backup coverage.

For private hiring, decide who will handle background checks, payroll taxes, scheduling, supervision, and emergency coverage.

A good home plan should respect the parent’s wish to remain at home without pretending that every home situation can be made safe with a few hours of help. If a parent needs constant supervision, complex medical care, two-person transfers, or more coverage than the family can afford or manage, the next decision may be broader than home care.

That does not make home care a failure. Sometimes home care is a bridge after hospitalization, a way to delay a move, a respite plan for a family caregiver, or one part of a larger care arrangement. If the options are widening, The Complete Spectrum of Senior Care Options: A Decision Framework for Families (2026) can help compare home care with adult day services, assisted living, memory care, and nursing care.

The family caregiver’s capacity belongs in the decision, too. If the plan only works because one person never gets sick, never travels, never sleeps badly, and never reaches a breaking point, it is not a plan yet. Respite and burnout resources are not extras; they are part of keeping care at home stable.

A grounded first plan

Start with the parent’s actual week. Write down what is unsafe, what is unfinished, what is medical, and what is simply too much for the family to keep absorbing. Match those needs to companionship, personal care, home health care, or skilled nursing. Price the likely hours before falling in love with a rate. Compare agency and private hiring by asking who will do the operating work. Then make the first calls without assuming the cheapest or fastest option is the safest fit.

Comments

Join the discussion with an anonymous comment.