The True Cost of Elderly Care: What $34 Per Hour Doesn't Tell You About the Hidden Financial Burden on Family Caregivers

The $34–$35/hr headline cost of professional in-home care masks a much larger financial story for family caregivers. This article reveals the hidden costs — lost wages, depleted savings, and reduced retirement — that can dwarf the hourly rate, and provides a budgeting framework and resources to help adult children navigate the full financial picture.

- Last Reviewed

- 2026-06-18

- caregiver burnout

- caregiver stress

- financial planning

- respite care

- working caregiver

The Headline Number: $34–$35 Per Hour and Why It Understates the True Cost

If you have recently searched for the cost of professional in-home care for an aging parent, you have likely seen a figure around $34 to $35 per hour. That number comes from two of the most widely cited national surveys. A Place for Mom's 2026 Costs of Long-Term Care and Senior Living Report puts the national median for private nonmedical in-home care at $34 per hour. The CareScout (Genworth) Cost of Care Survey, fielded from July through November 2025, reports a national median of $35 per hour for a non-medical caregiver, reflecting a 3% year-over-year increase.

These figures are useful as a starting point. At 44 hours per week — roughly the equivalent of a full-time work week — the annual cost at the $35/hour median reaches $80,080. That is a staggering number on its own. But here is the problem: for the family caregiver who is also paying these bills, the hourly rate is the least consequential figure in the entire financial picture.

The real financial weight of caregiving does not come from the check you write to a home care agency. It comes from the income you stop earning, the savings you drain, the retirement contributions you skip, and the health costs you absorb because you are too busy caring for someone else to care for yourself. These hidden costs can dwarf the per-hour expense, and they are almost never included in the headline rate.

If you are an adult child who has just started paying for a parent's care and feel financially blindsided, you are not alone. The goal of this article is to surface the full financial picture — the costs that do not appear on any invoice — and give you a framework to understand your own situation. For a broader orientation on what to expect in the early weeks of caregiving, our First 30 Days as a Family Caregiver guide provides a step-by-step onboarding path.

The 5 Hidden Costs of Family Caregiving That Add Up Faster Than the Hourly Rate

The $34–$35 per hour you pay for a home health aide is a direct, visible cost. The five categories below are indirect, often invisible, and cumulatively far more expensive. Understanding them is the first step toward making informed decisions rather than reactive ones.

1. Lost Income and Career Setbacks

This is the single largest hidden cost for most family caregivers. According to the Family Caregiver Alliance, as cited by A Place for Mom, 70% of working caregivers suffer work-related difficulties due to their dual roles. These difficulties take many forms: reducing hours, turning down promotions, using unpaid leave, or leaving the workforce entirely.

The long-term impact is staggering. A MetLife study cited by RubyWell found that women who leave the workforce early to provide caregiving lose an average of $131,351 in Social Security benefits over their lifetime. That figure does not include lost wages during the caregiving years, missed 401(k) matching contributions, or the compounding growth of retirement accounts that never get funded.

2. Increased Household Expenses

When a parent moves in or requires daily attention, household costs rise across the board. Utility bills increase from additional laundry, cooking, and climate control. Grocery bills climb to accommodate dietary needs and additional meals. Medical supplies — adult incontinence products, nutritional supplements, over-the-counter medications — become a recurring line item. These costs are easy to overlook because they blend into regular household spending, but they are real and they accumulate.

3. Caregiver Health Costs

Caregivers consistently neglect their own health. The A Place for Mom article on hidden costs notes that this neglect leads to increased chronic conditions. When you skip your own annual physical, delay filling a prescription, or ignore back pain from lifting, the eventual medical cost is often higher than the preventive care would have been. Add to that the cost of therapy, stress-related illness, and the simple fact that an exhausted caregiver is more prone to accidents and illness.

4. Home Modifications

Making a home safe for an aging parent is rarely optional. Grab bars, shower chairs, raised toilet seats, ramps, stair lifts, and widened doorways all carry costs that range from modest to substantial. A single bathroom modification can run several thousand dollars. These are one-time expenses, but they often arrive at the worst possible time — right when the family is already absorbing new ongoing costs. Our Caregiver's Guide to Home Modifications breaks down what actually works, what it costs, and what to prioritize first.

5. Lost Retirement Savings

This is the most insidious hidden cost because its impact is delayed. Every year you reduce your work hours or leave the workforce, you lose not just that year's income but also the compounding growth of that income for the next 10, 20, or 30 years. You miss employer matching contributions. You draw down existing retirement accounts to cover current expenses. The $131,351 average loss in Social Security benefits for women is just one piece of this. The total lifetime impact — lost wages, lost growth, and depleted savings — can easily exceed $300,000 for a caregiver who leaves the workforce for several years.

The Data Behind the Burden: What Working Caregivers Actually Face

The statistics paint a clear picture of financial strain that goes well beyond the hourly rate. These numbers come from multiple sources — A Place for Mom, AARP research cited by RubyWell, and the Family Caregiver Alliance — and they consistently tell the same story.

- 70% of working caregivers suffer work-related difficulties due to their dual caregiving and employment roles (Family Caregiver Alliance, via A Place for Mom).

- 22% of caregivers report using all their short-term savings to cover caregiving costs (A Place for Mom).

- 12% of caregivers have exhausted all their long-term savings (A Place for Mom).

- Family caregivers spend an average of over $7,200 per year in out-of-pocket costs (AARP research, cited by RubyWell).

- Caregivers spend roughly 20% of their income on caregiving-related expenses (A Place for Mom).

- About 60% of family caregivers also work full or part time (RubyWell, citing AARP).

These numbers are not abstract. They represent real families making impossible trade-offs: paying for a parent's medication instead of contributing to a 401(k), using vacation days for doctor appointments instead of rest, or watching a retirement account dwindle because the monthly care bill leaves nothing left to save. If you are in this position, the data confirms that your experience is not an exception — it is the norm. For a deeper look at why so many caregivers start without full readiness, see our guide on why 70% of caregivers start unprepared and how to build a care foundation.

Why Financial Stress Is a Primary Driver of Caregiver Burnout

Caregiver burnout is often discussed in terms of physical exhaustion and emotional strain — the sleepless nights, the constant worry, the feeling of being pulled in too many directions. Those are real. But financial stress is a primary, and often underacknowledged, driver of burnout.

The data from A Place for Mom shows that 40% of family caregivers find caregiving highly stressful. When you layer financial insecurity on top of the physical and emotional demands, the result is a compounding effect. You are not just tired and worried — you are also watching your financial future erode. You are making decisions not based on what is best for your parent or for you, but on what you can afford right now. That loss of agency is profoundly draining.

The Haven Healthcare Advocates article on financial stress and burnout makes this connection explicit: caregiver burnout is not just physical and emotional — financial stress is a primary contributor. The constant arithmetic — how much did we spend this month, how much is left, what do we cut next — becomes a mental load that never lifts.

Acknowledging the financial stress is not defeat — it is the first step toward addressing it. The budgeting framework in the next section is designed to help you move from feeling overwhelmed to having a clearer picture of your actual situation. Sometimes clarity alone reduces the stress.

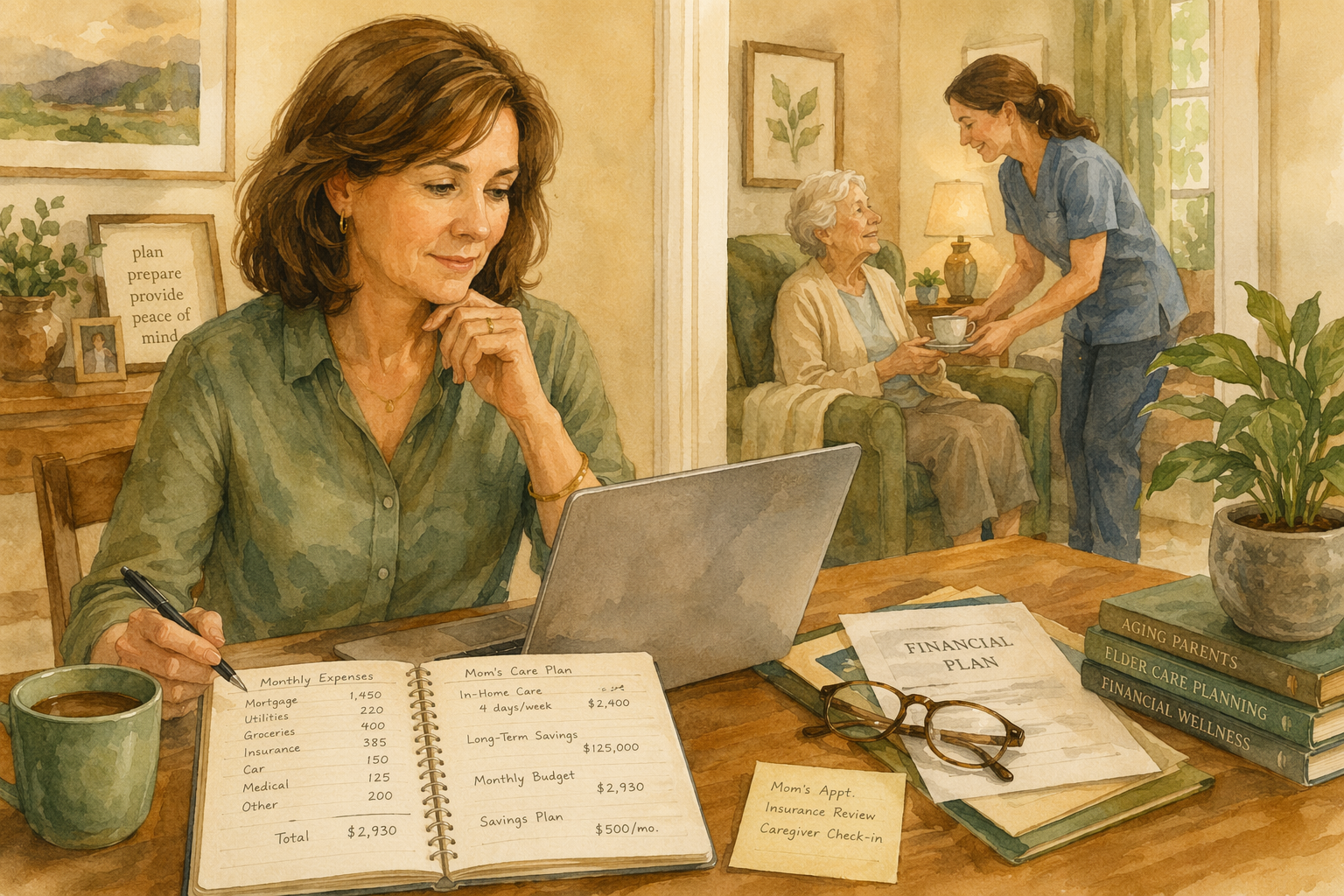

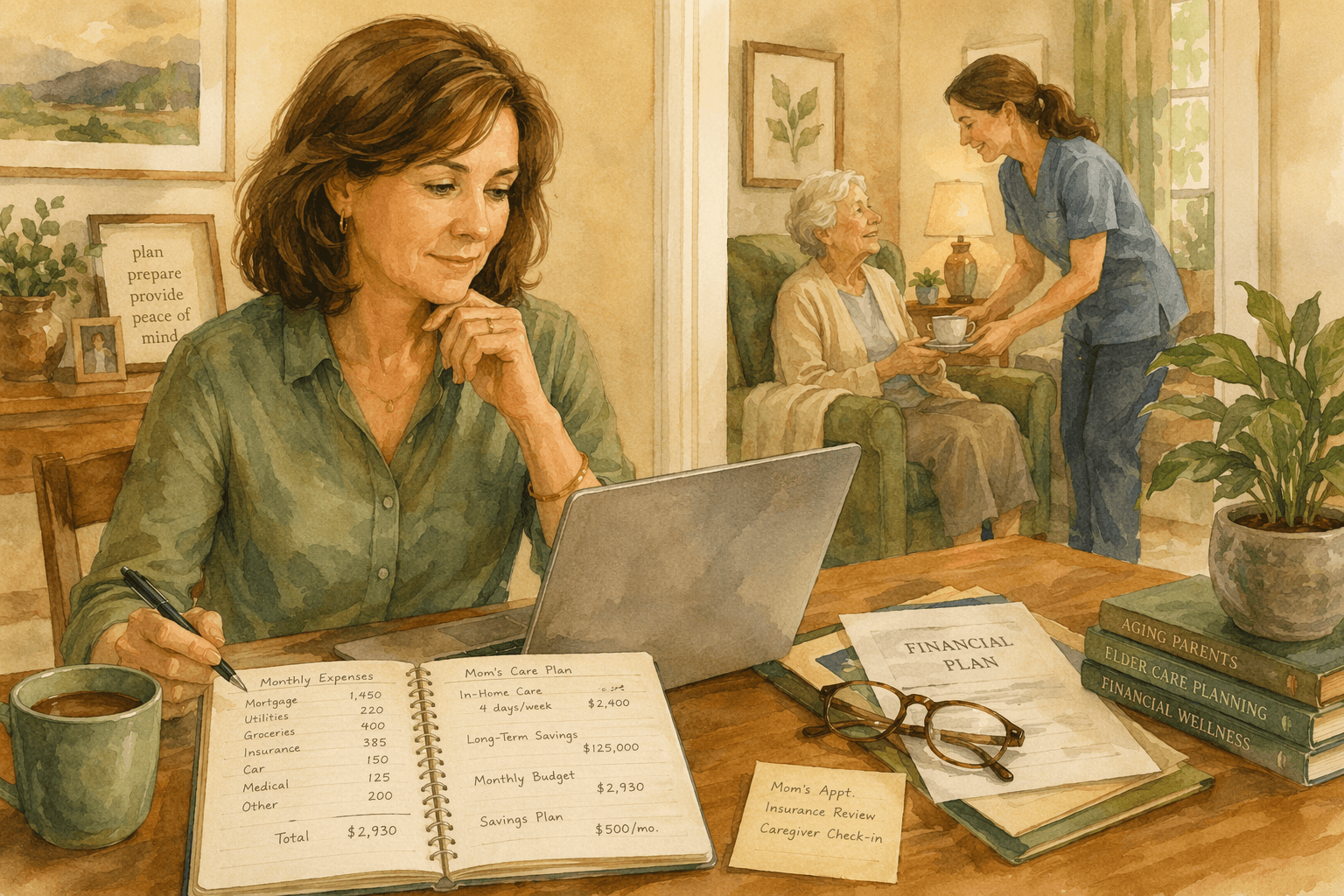

A Budgeting Framework to Surface the Hidden Costs in Your Own Situation

You cannot manage what you have not measured. The following framework is designed to help you calculate your own true cost of caregiving. It is not a one-size-fits-all budget — it is a diagnostic tool to surface the costs that are hiding in plain sight.

| Cost Category | What to Include | Monthly Estimate |

|---|---|---|

| Direct care costs | Agency or independent caregiver hours, adult day care, respite care | |

| Lost wages | Reduced hours × your hourly rate; unpaid leave days; missed promotions (estimate conservatively) | |

| Increased household expenses | Additional groceries, utilities, medical supplies, laundry, transportation to appointments | |

| Home modifications | Grab bars, ramps, stair lifts, bathroom modifications (divide one-time costs by 12 for monthly view) | |

| Your own health costs | Missed preventive care, therapy, stress-related medical visits, medications you delayed filling | |

| Retirement impact | Missed 401(k) contributions, lost employer match, retirement account withdrawals (annualize and divide by 12) |

Continue Your Caregiving Journey

When you are ready, these resources can help with specific caregiving tasks.

- Setting Caregiving Boundaries Without the Guilt: A Practical Guide for Family Caregivers

Learn how to set clear, compassionate boundaries with your loved one and family without being paralyzed by guilt. This guide provides a framework for understanding the three root sources of caregiver guilt and offers concrete scripts and a decision table to help you protect your own well-being while sustaining your caregiving role.

- The Unprepared Caregiver: Why 70% Start Without Full Readiness and How to Build a Care Foundation in 5 Steps

Most family caregivers begin without feeling fully prepared. This article normalizes that experience and provides a practical 5-step framework — from needs assessment to support building — to help adult children caring for aging parents move from overwhelm to action.

- The 4 Stages of Caregiver Burnout: A Self-Recognition Framework

Recognize which stage of caregiver burnout you're in—Warning, Control, Survival, or Burnout—using concrete behavioral and emotional signals, and take stage-specific action to recover before reaching crisis.

Comments

Join the discussion with an anonymous comment.