Clinical term

How Medicare Pays for Skilled Nursing Facility Care in 2026: A Complete Guide for Caregivers

The Financial Shock of a Hospital Discharge: What Medicare Will and Won't Pay For

The phone call comes from the hospital discharge planner: your parent is stable enough to leave, but not well enough to go home. They need a skilled nursing facility for rehabilitation. Your first question, spoken or unspoken, is almost always the same: "How are we going to pay for this?"

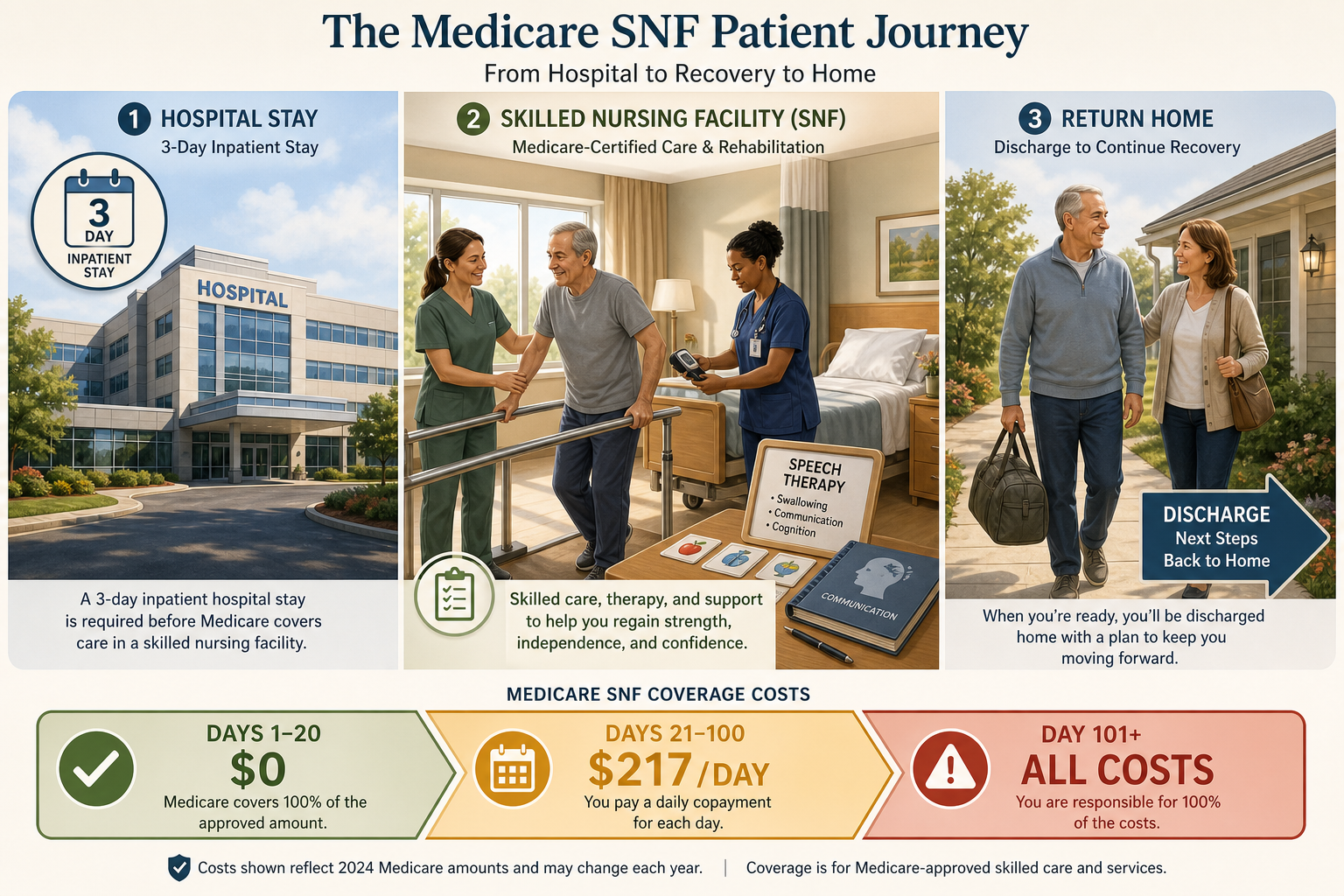

A skilled nursing facility (SNF) is a temporary, Medicare-covered setting for short-term rehabilitation after a hospitalization. It is not a nursing home for long-term custodial care, though the two terms are often confused. Medicare Part A covers up to 100 days per benefit period in a Medicare-certified SNF, but the rules governing that coverage are strict, and the costs escalate quickly after the first three weeks. Understanding these rules before discharge can mean the difference between a manageable recovery and a financial crisis.

This guide walks through the 2026 payment mechanics step by step: the qualifying rules, the exact costs you will face, what is covered and what is not, how Medicare Advantage plans differ, and — critically — your rights to appeal if coverage is denied or terminated. For a full definition of what an SNF is and a basic eligibility overview, see our companion article: Skilled Nursing Facility (SNF): What It Is and When Medicare Covers It.

The Qualifying Event: What Counts as a 3-Day Inpatient Hospital Stay

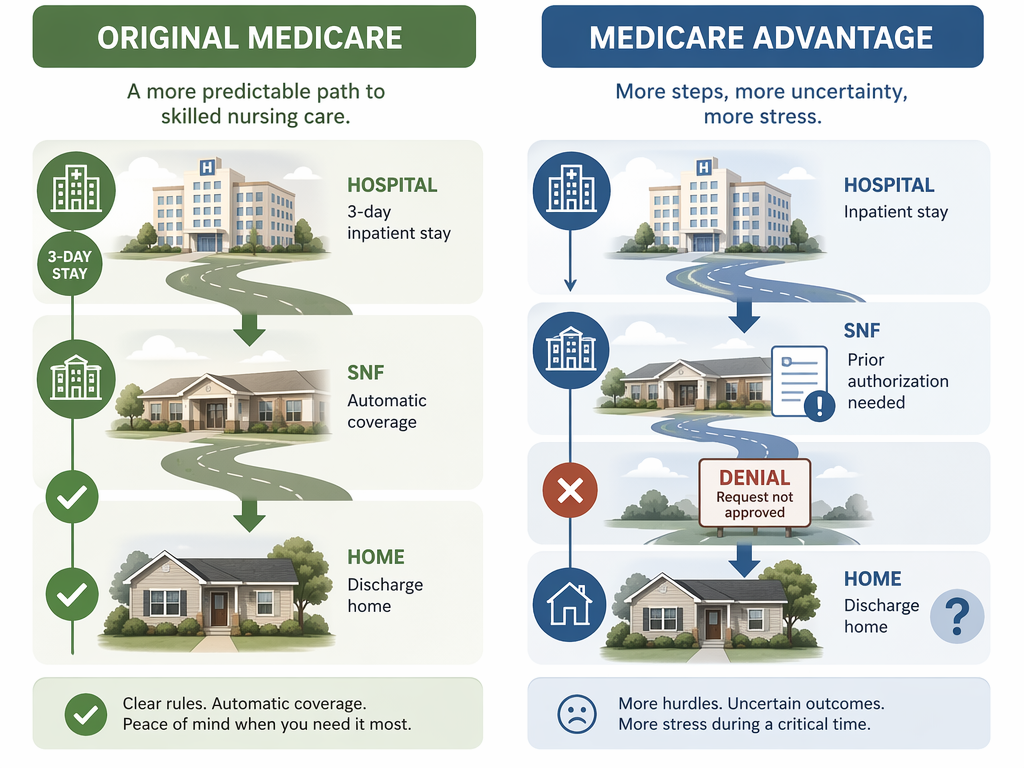

The single most important rule for Medicare SNF coverage is this: the patient must be formally admitted as an inpatient at a hospital for at least three consecutive days. The clock starts ticking the day of admission and stops the day of discharge. The day of discharge itself does not count toward the three-day total.

Here is what does not count toward the three-day requirement:

- Time spent in the emergency room, even if it lasts many hours.

- Time spent under observation status, even if the patient occupies a hospital bed overnight.

- The day of discharge from the hospital.

- Outpatient surgery or procedures, even if followed by an overnight stay in a recovery area.

The observation status trap is a common source of denied SNF claims. A patient may spend two or three nights in a hospital bed, receive medications and monitoring, and still be classified as an outpatient under observation. Because observation status does not count as an inpatient admission, the patient never triggers the three-day qualifying clock. The hospital is required to provide a Medicare Outpatient Observation Notice (MOON) if observation lasts more than 24 hours, but in the chaos of a hospitalization, this notice is easy to miss.

Once the three-day inpatient requirement is met, the patient must be admitted to a Medicare-certified SNF within 30 days of leaving the hospital. If the patient is readmitted to a hospital during that 30-day window, the clock resets, and they must be admitted to the SNF within 30 days of the most recent discharge.

Full Eligibility Checklist for Medicare SNF Coverage

Before Medicare will pay for SNF care, all of the following conditions must be met. Use this checklist as a quick reference when speaking with the hospital discharge planner or the SNF admissions coordinator.

- The patient has Medicare Part A coverage.

- The patient had a qualifying inpatient hospital stay of at least three consecutive days (not counting the day of discharge).

- The patient is admitted to a Medicare-certified SNF within 30 days of hospital discharge.

- A physician certifies that the patient needs daily skilled nursing care or skilled therapy services (physical, occupational, or speech-language pathology).

- The skilled care is for a condition that was treated during the qualifying hospital stay, or for a condition that arose while in the SNF for that stay.

- The SNF is Medicare-certified and accepts Medicare assignment.

"Daily" skilled care means seven days a week for nursing, or nursing and therapy combined. For therapy alone, "daily" means at least five days a week. The care must be provided by or under the supervision of licensed professionals — registered nurses, licensed practical nurses, physical therapists, occupational therapists, or speech-language pathologists.

Understanding Benefit Periods and the 60-Day Reset

Medicare does not give you a fresh 100 days of SNF coverage every calendar year. Instead, coverage is organized around something called a "benefit period." A benefit period starts the day the patient is admitted to a hospital or SNF as an inpatient. It ends after the patient has been out of a hospital or SNF for 60 consecutive days.

Here is how this works in practice:

- Your parent is hospitalized for a hip replacement (benefit period begins).

- They are discharged to a SNF for rehabilitation and use 40 days of SNF coverage.

- They return home and do not go back to a hospital or SNF for 60 days (benefit period ends).

- If they are later hospitalized again for a different condition, a new benefit period begins, and they have a fresh 100 days of SNF coverage available.

The 60-day reset is one of the most important concepts for caregivers to understand because it means that a patient who has multiple hospitalizations separated by more than 60 days can potentially qualify for multiple rounds of SNF coverage. Conversely, a patient who is readmitted to a hospital within 60 days of leaving a SNF remains in the same benefit period, and the SNF coverage clock continues from where it left off.

For definitions of technical terms like "benefit period" and "coinsurance," see our SNF Medicare Coverage Glossary: 25+ Key Terms for Family Caregivers (2026).

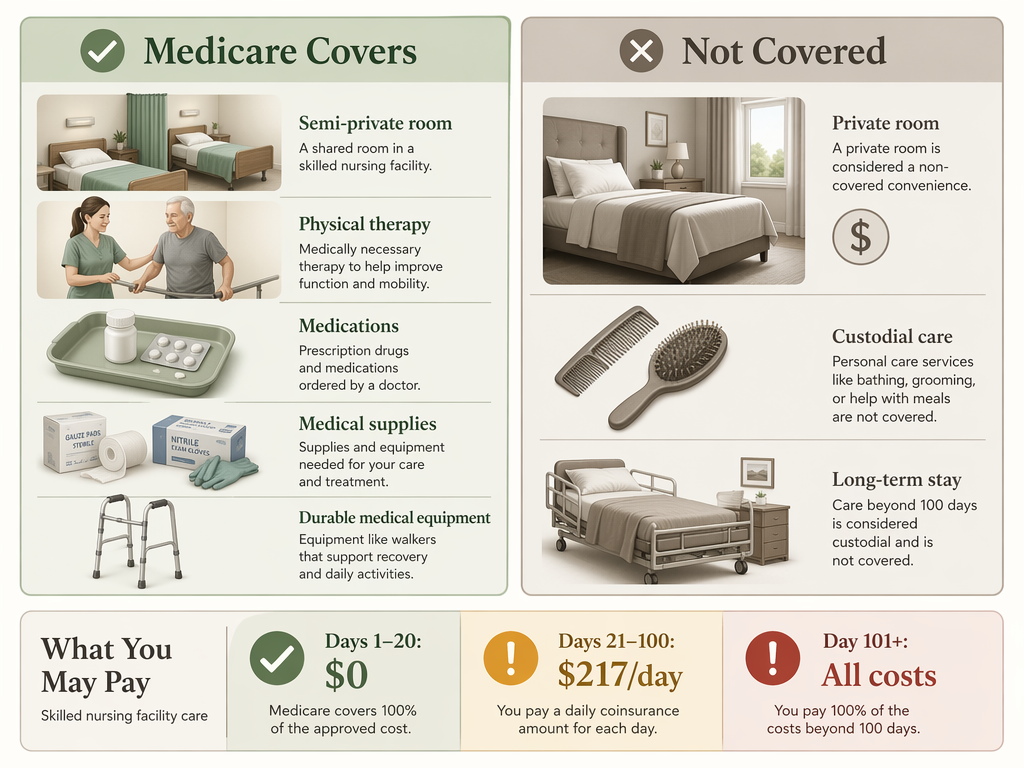

2026 Cost Breakdown: What You Will Pay for Days 1 Through 100 and Beyond

Medicare SNF coverage is not free after day 20. The cost structure for 2026 is as follows:

| Days | Patient Cost (2026) | What Medicare Pays |

|---|---|---|

| Days 1–20 | $0 (after Part A deductible met) | All covered costs |

| Days 21–100 | $217 per day coinsurance | All costs above $217/day |

| Day 101 and beyond | All costs (no Medicare coverage) | $0 |

Before Medicare pays anything for SNF care, the patient must first meet the Part A deductible for the benefit period. In 2026, that deductible is $1,736. If the patient has already met the Part A deductible during the same benefit period (for example, during the qualifying hospital stay), they do not need to pay it again for the SNF stay.

The $217 per day coinsurance for days 21 through 100 is up from $209.50 in 2025. This means that for a patient who uses all 100 days of SNF coverage in a single benefit period, the total out-of-pocket cost for days 21 through 100 would be $217 multiplied by 80 days, or $17,360 — plus the Part A deductible if not already met.

The average SNF stay is about 28 days, according to CMS 2022 data cited by A Place for Mom. This means most patients will not reach the $217/day coinsurance period. However, for patients who need extended rehabilitation — for example, after a stroke or complex orthopedic surgery — the costs can accumulate quickly.

What Medicare Covers in a SNF — and What It Does Not

Understanding the boundary between covered and non-covered services is essential for avoiding surprise bills. Medicare Part A covers a specific set of services when provided in a Medicare-certified SNF. Anything outside that set is the patient's financial responsibility.

| Covered by Medicare Part A | Not Covered by Medicare |

|---|---|

| Semi-private room (2–4 beds per room) | Private room upgrades |

| All meals, including special dietary needs | Personal convenience items (TV, phone, internet) |

| Skilled nursing care (RNs and LPNs) | Long-term or custodial care (help with bathing, dressing, eating) |

| Physical therapy, occupational therapy, speech-language pathology | Care beyond 100 days per benefit period |

| Medical social services | Private-duty nursing |

| Medications provided in the SNF | Medications not related to the SNF stay |

| Medical supplies and equipment used in the SNF | Non-prescription supplies |

| Ambulance transportation (when other transport would endanger health) | Transportation for non-medical reasons |

| Dietary counseling | Haircuts, manicures, or other personal services |

The most important distinction is between skilled care and custodial care. Skilled care requires the involvement of licensed medical professionals — nurses, therapists, or social workers. Custodial care — help with activities of daily living like bathing, dressing, eating, and toileting — is not covered by Medicare Part A when it is the only care needed. However, if a patient is receiving skilled care (for example, physical therapy after a hip replacement), the custodial care provided alongside it is covered as part of the overall SNF stay.

The TEAM Model: A New 3-Day Rule Waiver for 2026–2030

A significant change in 2026 is the CMS Transforming Episode Accountability Model (TEAM), a demonstration program that waives the three-day inpatient stay requirement for certain surgical episodes in participating hospitals. Under the TEAM model, patients who undergo specified surgical procedures at participating hospitals can be admitted directly to a SNF for post-acute care without first meeting the three-day inpatient rule.

The TEAM model is designed to test whether eliminating the three-day rule for certain episodes reduces costs and improves outcomes by enabling earlier discharge to SNF-level care. For caregivers, this means that if your parent is having a qualifying surgical procedure at a participating hospital, you may have more flexibility in timing the transition to a SNF. However, because this is a demonstration program, the rules may vary by hospital and by surgical episode. Always confirm directly with the hospital's discharge planning team.

Medicare Advantage Plans: Different Rules, Prior Authorization, and Denial Risks

If your parent has a Medicare Advantage (Part C) plan instead of Original Medicare, the SNF coverage rules may be significantly different. Medicare Advantage plans are offered by private insurance companies and can set their own rules for SNF coverage, as long as they meet or exceed Original Medicare's minimum standards.

Key differences to watch for:

- Prior authorization: Many Medicare Advantage plans require prior authorization before the patient can be admitted to a SNF. Without it, the plan may deny coverage even if the patient meets all other criteria.

- No prior hospital stay requirement: Some Medicare Advantage plans do not require a prior three-day inpatient hospital stay. This can be an advantage for patients who need SNF-level care after an outpatient procedure or a period of observation.

- Network restrictions: Medicare Advantage plans typically have a network of preferred SNFs. Going out of network may result in higher costs or denied coverage.

- Higher denial rates: There have been reports of Medicare Advantage plans denying SNF coverage more frequently than Original Medicare. The CaringInfo source notes that "there have been reports of denial of skilled nursing care by these plans."

For a broader review of how Medicare Parts A, B, C, and D work, see our Medicare Definition for Caregivers: What Parts A, B, C, and D Actually Cover.

What Happens After Day 100: Medicaid, Long-Term Care Insurance, and Private Pay

When Medicare SNF coverage ends — whether at day 100 or earlier — the patient has three primary options for continuing care: Medicaid, long-term care insurance, or private pay. Understanding these options before day 100 arrives is critical for avoiding a coverage gap.

Medicaid

Medicaid is the primary payer for long-term institutional care in the United States. According to KFF data from 2023, Medicaid paid for 44% of long-term institutional care costs. For nursing facility residents specifically, Medicaid is the primary payer for 63% of residents, while Medicare covers only 14%.

Medicaid covers long-term custodial care in nursing homes — the kind of care that Medicare does not cover. However, Medicaid eligibility is based on strict income and asset limits that vary significantly by state. In most states, the patient must have limited income and assets (often below $2,000 in countable assets, excluding a primary home and certain other exempt assets) to qualify.

Long-Term Care Insurance

If the patient has a long-term care insurance policy, it may cover SNF care after Medicare benefits are exhausted. Policies vary widely in what they cover, daily benefit amounts, elimination periods (the waiting period before benefits begin), and maximum benefit periods. Review the policy carefully and contact the insurance company to confirm coverage details.

Private Pay

Without Medicaid or long-term care insurance, the patient must pay out of pocket. The costs are substantial. According to the Genworth 2025 Cost of Care Survey, the national median monthly cost of a nursing home is $9,277 for a semi-private room and $10,646 for a private room. At these rates, a few months of private-pay care can quickly deplete a family's savings.

The average nursing home stay is 485 days, according to HHS 2019 data cited by A Place for Mom. This means that a patient who transitions from Medicare-covered SNF care to long-term nursing home care may face many months or years of out-of-pocket costs before qualifying for Medicaid.

Your Right to Appeal: How to Challenge a Denial and the Jimmo Maintenance Standard

One of the most important things a caregiver can do is understand that Medicare SNF coverage decisions can be appealed. If the SNF or Medicare proposes to terminate coverage, or if a claim is denied, the patient has the right to challenge that decision.

When the SNF Proposes to Terminate Coverage

If the SNF believes the patient no longer needs skilled care, it must provide written notice before terminating Medicare-covered services. This notice must offer the patient the right to an "expedited" (fast-track) review. The patient or caregiver must request this review within a specific timeframe — typically within the same day the notice is received.

- Do not sign any document agreeing to terminate coverage without understanding your rights.

- Request the expedited review immediately if you believe the patient still needs skilled care.

- Contact the Medicare Beneficiary Ombudsman or the Center for Medicare Advocacy for assistance.

The Jimmo Maintenance Standard

A common reason SNFs give for terminating coverage is that the patient has stopped improving — that they have reached a "plateau" and no longer need skilled therapy. However, the Jimmo v. Sebelius settlement (a class-action lawsuit) confirmed that Medicare covers skilled services to maintain a patient's condition or slow a decline, even if the patient is not expected to improve.

The Center for Medicare Advocacy provides detailed guidance on appealing SNF coverage denials and understanding the Jimmo standard. Their website offers sample appeal letters, step-by-step instructions, and contact information for Medicare beneficiary advocates.

How to Appeal a Denial

The Medicare appeals process has five levels:

- Redetermination by the Medicare Administrative Contractor (MAC) — request within 120 days of the denial.

- Reconsideration by a Qualified Independent Contractor (QIC) — request within 180 days of the redetermination.

- Hearing by an Administrative Law Judge (ALJ) — for claims of $180 or more.

- Review by the Medicare Appeals Council.

- Judicial review in federal district court.

For SNF coverage terminations, the expedited review process is faster than the standard appeals process. The patient or caregiver should request the expedited review immediately upon receiving a termination notice. The SNF must continue providing care during the review process if the patient requests the review before the termination date.

Browse more in the Glossary.