Home Care vs. Home Health Care: A Decision Framework for Seniors With Chronic Conditions in 2026

Adult children caregivers often confuse non-medical home care with skilled home health care, leading to wasted time and money. This guide provides a clear comparison, explains how 2026 Medicare changes affect coverage, and offers a step-by-step framework for combining both services for a parent with multiple chronic conditions.

By Editorial Team

new caregiver

care coordination

medication management

ADLs

first steps

📄

A printable version of this guide is available. Use your browser's print function (Ctrl+P / ⌘P) to save or print.

Why Confusing Home Care and Home Health Care Is the Most Costly Mistake Caregivers Make

You have just realized your parent needs more help than you can provide alone. The search begins, and you encounter two phrases that sound almost identical: home care and home health care. It is a small distinction in language but a massive one in practice — and getting it wrong costs families thousands of dollars and delays critical medical support.

The numbers make the stakes clear. According to the National Council on Aging, 93% of adults age 65 and older have at least one chronic condition, and 79% have two or more. Hypertension affects 61% of older adults, arthritis affects 51%, and diabetes affects 24%. A parent managing multiple chronic conditions likely needs both daily living support and skilled medical oversight — but those two needs are met by entirely different services with different costs, different insurance coverage, and different provider qualifications.

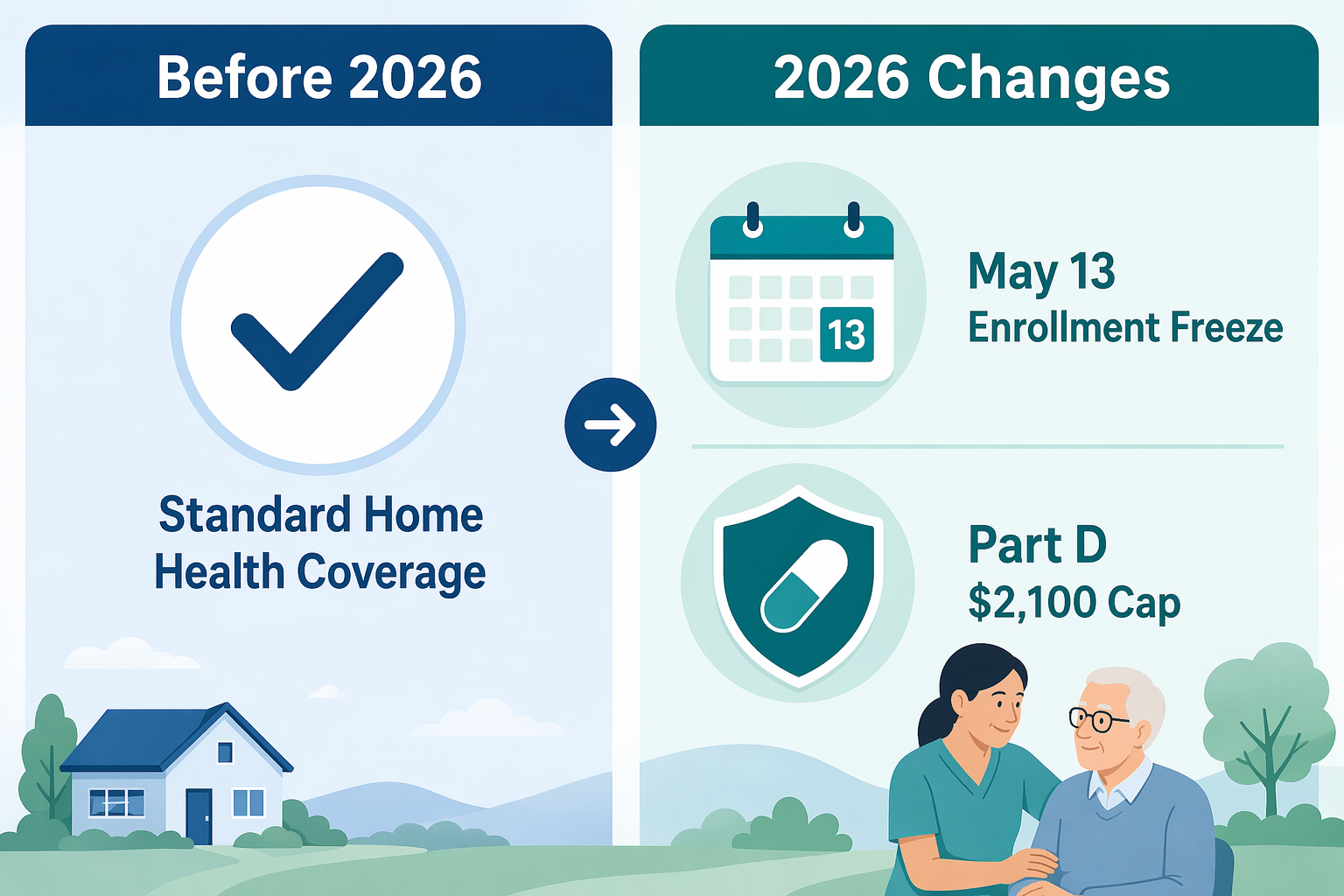

The urgency is heightened by 2026 policy changes. On May 13, 2026, the Centers for Medicare & Medicaid Services (CMS) implemented a six-month freeze on new home health agencies and hospice providers enrolling in Medicare. Existing beneficiaries are not affected, but the freeze signals a tightening of the home health landscape. Meanwhile, Medicare Part D now has a $2,100 annual out-of-pocket cap on prescription costs, and the Part B premium has risen to $202.90 per month. These changes directly affect how families pay for skilled home health — but they do nothing for non-medical home care, which remains almost entirely out-of-pocket.

Understanding the difference between these two services is not an academic exercise. It is the first and most important decision you will make as a caregiver navigating the home-based care system.

Home Care vs. Home Health Care: What Each Service Actually Does

The names are similar, but the services are fundamentally different. One provides hands-on medical treatment; the other provides assistance with the activities of daily living that a person can no longer manage alone.

Home Care (Non-Medical)

Home care, also called personal care or companion care, involves non-medical assistance with daily activities. A home care aide — typically a certified nursing assistant (CNA) or home health aide (HHA) — helps with:

Bathing, dressing, grooming, and toileting (activities of daily living, or ADLs)

Light housekeeping, laundry, and meal preparation

Companionship and supervision to prevent falls or wandering

Transportation to medical appointments or grocery shopping

Medication reminders (but not administering injections or managing complex medication regimens)

Home care does not require a doctor's order. It can begin at any time, continue indefinitely, and is paid almost entirely out-of-pocket. The national median cost in 2026 is $34 to $35 per hour, according to both A Place for Mom and U.S. News CareScout surveys. For 44 hours per week, that translates to roughly $6,673 per month.

Home Health Care (Skilled Medical)

Home health care is skilled medical care provided by licensed professionals. It requires a physician's order and a documented need for intermittent skilled services. The care team may include:

Registered nurses (RNs) or licensed practical nurses (LPNs) for wound care, IV therapy, medication administration, and health monitoring

Physical therapists (PTs) for mobility and strength rehabilitation after a fall, surgery, or stroke

Occupational therapists (OTs) for retraining in daily activities like dressing, cooking, and bathing

Speech-language pathologists for swallowing or communication disorders

Medical social workers for care coordination and counseling

The National Institute on Aging emphasizes that Medicare covers home health services only if they are short-term, medically necessary, and provided by a Medicare-certified agency. The goal is recovery and stabilization, not long-term custodial care. A private duty nurse costs a national median of $90 per hour ($17,160 per month for 44 hours per week), though Medicare and some private insurance plans cover a portion of these costs when eligibility criteria are met.

Head-to-Head Comparison: Services, Cost, Insurance, and Provider Qualifications

The table below lays out the key differences side by side. Use it as a quick reference when evaluating which service — or combination of services — fits your parent's situation.

Comparison of home care and home health care across key decision factors. Sources: A Place for Mom Cost of Care Survey, U.S. News CareScout Survey, NIA, CMS.

$90 per hour (private duty nurse); skilled therapy visits billed per session

Typical monthly cost (44 hrs/week)

~$6,673

~$17,160 (private duty nursing); varies widely for intermittent therapy

Medicare coverage

Not covered (no medical benefit)

Covered if short-term, medically necessary, and from a Medicare-certified agency

Medicaid coverage

Varies by state; some states offer home- and community-based services (HCBS) waivers

Varies by state; typically covers skilled services if eligibility criteria are met

Duration of service

Can continue indefinitely

Typically limited; Medicare recertification required every 60 days

Best for

Seniors who need help with daily activities but do not require ongoing medical treatment

Seniors recovering from surgery, illness, or injury, or managing unstable chronic conditions

How 2026 Medicare Changes Affect Home Health Coverage — Not Personal Care

Several significant Medicare changes took effect in 2026, and every one of them affects skilled home health care — not non-medical home care. Understanding this distinction is critical because it means the financial and access landscape for home health is shifting, while the cost of personal care remains entirely on families.

The May 2026 CMS Home Health Enrollment Freeze

On May 13, 2026, CMS implemented a six-month freeze on new home health agencies and hospice providers enrolling in the Medicare program. This is a significant regulatory action that does not affect current beneficiaries — your parent's existing home health services continue uninterrupted — but it has important implications:

Fewer new agencies entering the market may reduce competition and choice in some areas.

Agencies already enrolled in Medicare may see increased demand, potentially affecting wait times for new patients.

If your parent needs to switch agencies or start home health for the first time, you may need to verify that the agency is already Medicare-certified and not affected by the freeze.

2026 Part B Premium and Deductible Increases

The standard Medicare Part B monthly premium rose to $202.90 in 2026 (up from $185 in 2025), and the annual deductible increased to $283 (up from $257), according to the official CMS fact sheet. These increases affect all Medicare beneficiaries, including those receiving home health services. Since Medicare Part B covers home health, the higher premium and deductible mean slightly higher out-of-pocket costs before coverage kicks in.

Part D $2,100 Out-of-Pocket Cap and New Drug Prices

Starting January 1, 2026, Medicare Part D has an annual out-of-pocket cap of $2,100 for covered prescription medications. This is a significant benefit for seniors managing multiple chronic conditions who take several medications. Additionally, CMS has implemented newly negotiated prices for 10 prescription drugs, which may lower costs further. These changes do not affect home care costs, but they reduce the financial burden of medications for seniors receiving home health services.

Medicare Advantage Plan Changes

According to a KFF analysis, 67% of Medicare Advantage plans with Part D (MA-PDs) will charge no additional premium in 2026. However, the share of plans offering certain supplemental benefits has declined: the over-the-counter allowance dropped from 73% to 66%, and the meal benefit dropped from 65% to 57%. For families considering home health, this means fewer MA plans may offer non-medical supplemental benefits that could offset some home care costs.

Key 2026 Medicare changes that specifically affect skilled home health coverage, not personal care services.

When You Need One, Both, or Neither: A Decision Framework for Chronic Conditions

Every senior's situation is different, but common patterns emerge when managing multiple chronic conditions. The following scenarios illustrate when home care alone is sufficient, when home health is required, when both are needed simultaneously, and when a higher level of care may be more appropriate.

Scenario 1: Home Care Alone Is Sufficient

Your parent has well-managed hypertension and arthritis. They take their medications correctly, see their primary care doctor regularly, and have no recent hospitalizations. However, they struggle with bathing, meal preparation, and housekeeping due to joint pain and reduced mobility.

In this case, home care is the right choice. A home care aide can assist with ADLs, prepare meals, and provide companionship. No skilled medical oversight is needed because the chronic conditions are stable. The cost is out-of-pocket, but it is significantly lower than home health care.

Scenario 2: Home Health Care Is Required

Your parent was recently discharged from the hospital after a hip replacement surgery. They have diabetes that requires insulin management and blood sugar monitoring. The surgeon ordered physical therapy to regain mobility and an occupational therapist to assess home safety.

Home health care is essential here. A nurse will visit to monitor the surgical wound, check blood sugar, and administer insulin. A physical therapist will guide rehabilitation exercises. These services are covered by Medicare Part B because they are short-term, medically necessary, and ordered by a physician. The goal is recovery and stabilization, not long-term support.

Scenario 3: Both Services Are Needed Simultaneously

Your parent has congestive heart failure, diabetes, and early-stage mobility decline. They were recently hospitalized for fluid overload and now need a nurse to monitor weight, blood pressure, and medication adjustments. At the same time, they cannot safely bathe, prepare meals, or manage housekeeping on their own.

This is the most common scenario for seniors with multiple chronic conditions, and it requires both services. A home health agency provides the skilled nursing visits (covered by Medicare), while a separate home care agency provides daily living support (paid out-of-pocket or through long-term care insurance). The two services operate on different schedules and with different goals, but together they enable the senior to remain safely at home.

Scenario 4: When a Higher Level of Care May Be Needed

Your parent has advanced dementia, requires 24-hour supervision, has frequent falls, and is incontinent. They also have multiple chronic conditions that are poorly controlled despite home health visits.

In this situation, home care and home health care together may not be sufficient. The cost of 24/7 home care averages $25,479 per month, and even with skilled nursing visits, the level of supervision and medical oversight needed may exceed what can be safely provided at home. An assisted living facility with memory care or a skilled nursing facility may be more appropriate and, in some cases, more cost-effective.

Decision Flowchart: Home Care vs. Home Health Care for Your Parent

The following flowchart is designed for crisis-mode decision-making. Start at the top and follow the path that matches your parent's current situation.

Use this flowchart to quickly determine whether your parent needs home care, home health care, both, or a higher level of care.

Questions to Ask Home Care and Home Health Agencies Before You Hire

Vetting a home care or home health agency requires asking the right questions. The following checklist covers the essential areas: licensing, insurance acceptance, caregiver training, backup plans, and coordination between services. Print this list and take it with you when you call or visit agencies.

Questions for Any Agency

Is your agency licensed and bonded in this state? Can you provide proof of licensure?

Do you conduct background checks on all caregivers? What level of screening do you perform?

What training and certification do your caregivers have? Are they CNAs, HHAs, or RNs?

Do you have a backup plan if the regular caregiver is sick or unavailable?

How do you handle emergencies after hours? Is there a 24/7 contact number?

Can you provide references from current or recent clients with similar needs?

What is your policy for replacing a caregiver who is not a good fit?

Questions Specific to Home Health Agencies

Is your agency Medicare-certified? (This is essential for Medicare coverage.)

Are you affected by the May 2026 CMS enrollment freeze? If so, what does that mean for new patients?

Do you accept Medicare Part B, Medicare Advantage, Medicaid, or private insurance? Can you verify my parent's specific coverage?

How do you coordinate care with the patient's primary care physician and specialists?

What is the typical frequency and duration of skilled nursing or therapy visits?

How do you handle medication management? Do nurses administer injections or IV therapies?

What is your process for recertification every 60 days under Medicare?

Questions Specific to Home Care Agencies

What is your hourly rate? Are there additional fees for weekends, holidays, or overnight shifts?

Do you accept long-term care insurance? Do you bill the insurance company directly?

Can you provide a written care plan that outlines the specific tasks the aide will perform?

How do you ensure consistency of caregivers? Will my parent see the same aide regularly?

Do your aides provide medication reminders? (Note: they cannot administer medications without a nurse's license.)

How do you communicate with the family about changes in my parent's condition?

How to Combine Home Care and Home Health Care for Seniors With Multiple Chronic Conditions

For seniors managing multiple chronic conditions, the best approach is often a combination of both services. Home health care addresses the medical needs — wound care, medication management, physical therapy — while home care handles the daily living support that keeps the senior safe and comfortable at home. Here is a step-by-step framework for setting up both services simultaneously.

Step 1: Get a Doctor's Order for Home Health Care

Home health care cannot begin without a physician's order. Schedule an appointment with your parent's primary care doctor or, if they were recently hospitalized, work with the discharge planner. The doctor must certify that your parent is homebound and needs intermittent skilled nursing, physical therapy, occupational therapy, or speech therapy. Be specific about the chronic conditions involved — diabetes management, post-surgical recovery, heart failure monitoring — so the order is precise.

Step 2: Find a Medicare-Certified Home Health Agency

Use the Medicare Home Health Compare tool on the CMS website to find agencies in your area that are Medicare-certified. Verify that the agency is not affected by the May 2026 enrollment freeze. Ask the agency whether they accept your parent's specific Medicare Advantage plan or Medicaid coverage, if applicable. Request a written estimate of what Medicare will cover and what your out-of-pocket costs will be.

Step 3: Hire a Separate Home Care Agency for Daily Living Support

Home health agencies provide skilled visits on an intermittent schedule — typically a few hours per week. They do not provide the daily personal care that a senior with multiple chronic conditions often needs. For that, you will need a separate home care agency. Look for an agency that offers flexible scheduling (a few hours a day to full-time) and can assign a consistent caregiver who will build rapport with your parent.

Step 4: Establish a Care Coordination Plan

The biggest risk when using two agencies is poor communication. Create a simple care coordination plan that includes:

A shared medication list that both agencies update after every visit

A contact list with phone numbers for the home health nurse, home care aide, primary care doctor, and family caregiver

A daily log where the home care aide records observations (appetite, mood, mobility, any changes) that the home health nurse reviews during visits

A clear protocol for what to do in an emergency — who to call first, when to go to the ER, and when to notify the doctor

If coordination becomes overwhelming, consider hiring a geriatric care manager — a nurse or social worker specializing in geriatrics who can identify needs, create care plans, and coordinate services. The National Institute on Aging notes that geriatric care managers charge by the hour and are not covered by Medicare or Medicaid, but they can save families significant time and stress.

Step 5: Monitor and Adjust Over Time

Chronic conditions change over time. A parent who needs only home care today may need home health care after a hospitalization. A parent receiving home health for post-surgical recovery may eventually need only home care. Review the care plan every 60 days (aligned with Medicare's recertification schedule) and adjust as needed. The goal is to provide the right level of support at each stage without overpaying for services that are no longer necessary.

Five-step framework for combining home care and home health care for seniors with multiple chronic conditions.

Step

Action

Key Consideration

1. Get a doctor's order

Schedule an appointment with the primary care physician or discharge planner

Be specific about the chronic conditions and the type of skilled care needed

2. Find a Medicare-certified agency

Use Medicare Home Health Compare; verify certification and insurance acceptance

Confirm the agency is not affected by the May 2026 enrollment freeze

3. Hire a home care agency

Look for flexible scheduling and consistent caregiver assignments

Home care is paid out-of-pocket; ask about long-term care insurance coverage

4. Establish coordination

Create a shared medication list, contact list, daily log, and emergency protocol

Consider a geriatric care manager if coordination becomes difficult

5. Monitor and adjust

Review the care plan every 60 days; adjust as chronic conditions change

Avoid paying for services that are no longer medically necessary

Comments

Join the discussion with an anonymous comment.