How to Tell If Your Parent Needs Home Health or Home Care

For: adult childReviewed: 2026-07-09

How to Tell If Your Parent Needs Home Health or Home Care

After a hospitalization, many families struggle to distinguish skilled home health care from non-medical home care. This guide explains the core difference—Medicare-covered clinical services vs. out-of-pocket personal assistance—and provides a decision framework to help you choose the right care immediately.

By Editorial Team

new caregiver

experienced caregiver

long-distance caregiving

spousal caregiver

working caregiver

daily routines

medication management

personal hygiene

care coordination

first steps

ADLs

IADLs

The risky moment is usually not the day your parent gets sick. It is the day someone in the hospital says, “We’ll set up care at home,” and everyone in the family hears something different.

For one family, that may mean Medicare-covered home health: a nurse checking a wound, a physical therapist working on transfers after surgery, or a speech therapist helping after a stroke. For another family, it may mean someone coming in to help with bathing, meals, laundry, transportation, and supervision. Those sound close when you are standing in a hospital hallway. They are not close when the bill arrives.

The first question is not “Does Mom need help?” She probably does. The first question is: does she need skilled medical care ordered by a doctor, or non-medical daily help that the family must arrange and usually pay for privately?

The Short Version: Home Health Is Clinical, Home Care Is Daily Help

Home health care is skilled care. Under Medicare, covered home health services can include part-time or intermittent skilled nursing care, physical therapy, occupational therapy, speech-language pathology services, medical social services, and certain home health aide services when eligibility requirements are met.[1]

To qualify for Medicare-covered home health care, the person generally must be under a doctor’s care, need skilled services, be certified as homebound, and receive care from a Medicare-certified home health agency.[1] The National Council on Aging explains the same basic point plainly: Medicare home health is tied to skilled care, not general household help.[2]

Home care is non-medical help. It may include help bathing, dressing, preparing meals, light housekeeping, errands, transportation, companionship, or supervision. The National Institute on Aging describes these kinds of in-home supports as services that help older adults continue living at home, but they are not the same thing as Medicare-covered skilled home health care.[3]

If the main need is...

Start with...

Usual payment reality

Wound care, injections, medication changes, therapy after surgery, stroke recovery, fracture recovery, or another skilled clinical need

Home health

May be covered by Medicare if eligibility rules are met and the agency is Medicare-certified

Bathing, dressing, meals, housekeeping, errands, companionship, transportation, or supervision

Home care

Usually private pay unless another benefit or state program applies

Both recovery care and daily personal help

Both home health and home care

Medicare may cover the skilled part; the daily help may still be out-of-pocket

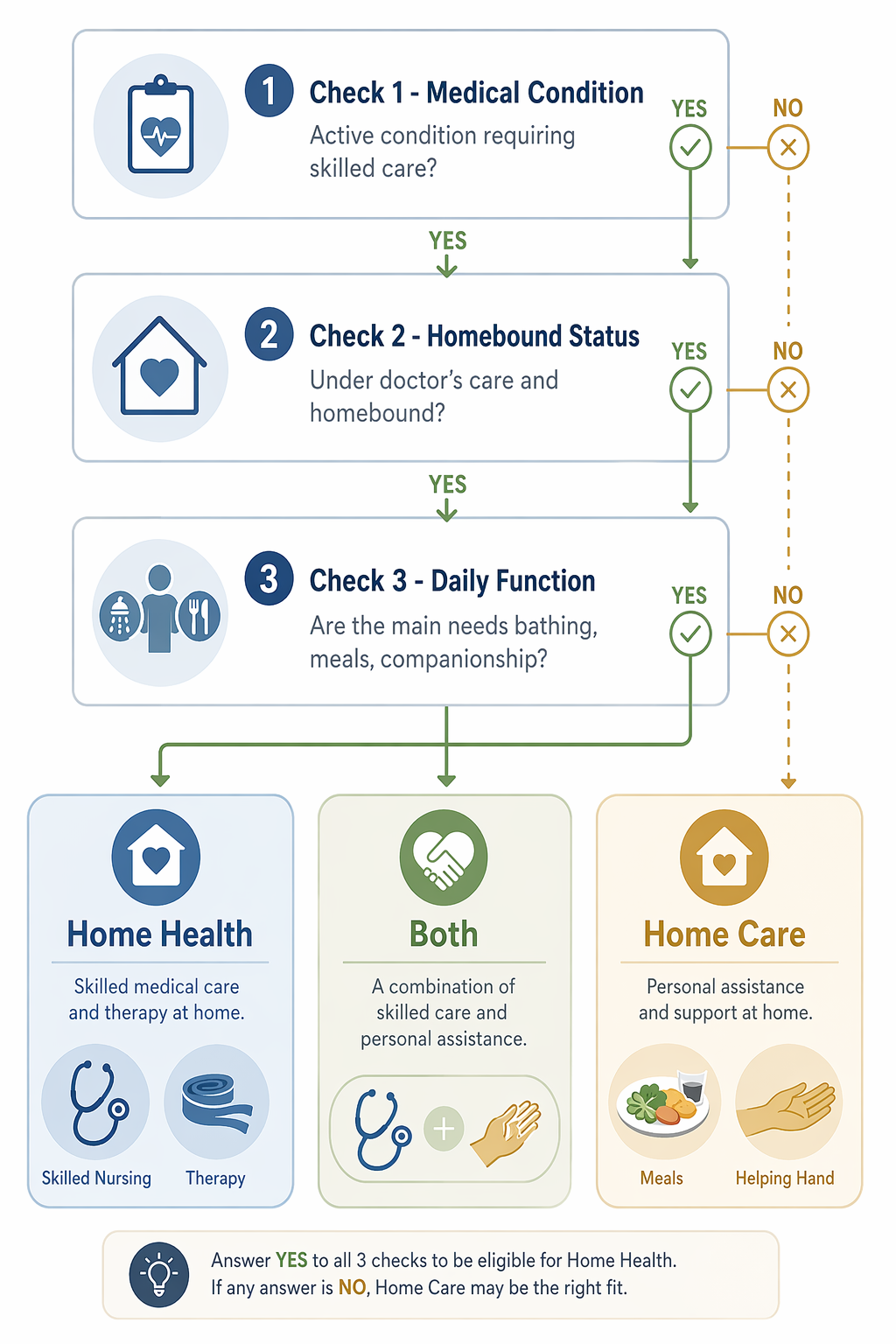

Run the Decision in This Order

When discharge is close, do not start by calling every agency in town. Start by sorting the need. A home care agency may sound helpful, but it cannot replace skilled nursing or therapy when those are medically indicated. A home health agency may provide essential clinical follow-up, but it is not an all-day bathing, cooking, and companionship solution.

Check 1: Is There an Active Medical Condition That Requires Skilled Care?

Start here if your parent is coming home after surgery, a stroke, a fall with fracture, a heart failure flare, a serious infection, a wound, a new medication regimen, or a hospitalization that clearly changed strength, mobility, swallowing, cognition, or safety. Johns Hopkins Medicine lists home health services such as nursing care, physical therapy, occupational therapy, speech therapy, and medical social services among the types of care that may be provided at home when medically needed.[4]

This is where families should slow down before trying to “manage with an aide.” If the discharge instructions include dressing changes, medication monitoring, therapy goals, weight-bearing limits, new oxygen use, signs of infection, or follow-up after a stroke or fracture, ask whether skilled home health is being ordered. Saving money by skipping necessary skilled care is not a plan; it is a risk shifted onto the parent and the family member watching them decline at home.

The wording matters. “Needs help at home” is not the same as “needs skilled home health.” Ask the hospitalist, surgeon, primary care doctor, or discharge planner: “What skilled service is being ordered, and what diagnosis or recovery need supports it?” If nobody can answer that, you may be dealing with a functional support problem rather than a Medicare home health problem.

Check 2: Does Your Parent Meet the Medicare Home Health Criteria?

Original Medicare does not cover home health simply because a person is old, tired, unsafe alone, or difficult for the family to manage. Medicare says the patient must need part-time or intermittent skilled services, be under the care of a doctor or allowed practitioner, have a plan of care, be homebound, and use a Medicare-certified home health agency.[1]

“Homebound” does not mean the person never leaves the house. Medicare’s home health coverage page explains that leaving home must require a considerable and taxing effort, and absences may still occur for medical treatment or short, infrequent non-medical reasons.[1] This is worth clarifying before discharge because a parent who can drive to outpatient therapy without major difficulty may be handled differently from a parent who cannot safely leave home without help.

If the criteria are met and the services are approved, Original Medicare covers home health services at 100% for covered services; Medicare.gov lists $0 for covered home health care services under Original Medicare, though durable medical equipment is handled differently.[1]

That $0 figure is important, but it is not a blank check for all help at home. It applies to covered home health services. It does not turn housekeeping, meal preparation, companionship, or long-term personal care into Medicare-covered benefits.

Check 3: Is the Main Problem Functional Daily Assistance?

Now look at what actually has to happen between 7 a.m. and bedtime. Can your parent get to the bathroom? Shower safely? Put on clean clothes? Heat food? Remember meals? Get to appointments? Avoid wandering out? Change bedding? Take out trash? Manage stairs? These are the gaps that create the family scramble after discharge.

If the primary need is bathing, dressing, meals, housekeeping, errands, transportation, companionship, or supervision, you are usually looking at home care. The National Institute on Aging includes personal care, household chores, meals, money management, and transportation among the types of services that can support older adults at home.[3] Those supports may be necessary. They are just not the same as Medicare-covered skilled home health.

If you are unsure whether the problem is medical, functional, or both, make a plain list of activities of daily living and instrumental activities of daily living before you call agencies. A structured in-home care needs assessment can keep the conversation from turning into vague phrases like “a little help” or “someone to check on her.”

The Medicare Trap: An Aide Is Not an Open-Ended Personal-Care Benefit

This is the part families often hear too late: Medicare may cover certain home health aide services only when they are part of an eligible home health plan of care. Medicare does not cover 24-hour-a-day care at home, meals delivered to the home, homemaker services when that is the only care needed, or personal care when that is the only care needed.[1]

The Medicare Rights Center makes the same distinction in its home health guidance: Medicare home health care is for people who meet specific requirements, and aide services are connected to the need for skilled care rather than a standalone long-term custodial benefit.[5]

So if the home health nurse says an aide may come a few times, do not build your whole care plan around that covering morning and evening routines indefinitely. Ask exactly what is ordered, how often the aide is expected, what tasks are included, and when services will be reassessed. If your parent needs more personal-care hours than the home health plan provides, that remaining need belongs in the home care plan.

Families who believe a parent is eligible for more aide support under a Medicare home health plan may need to ask pointed questions about the plan of care and documented need. A deeper guide to Medicare home health aide hours is useful when the issue is not whether Medicare ever covers aide services, but whether the current plan reflects the person’s eligible needs.

The Both-And Situation Is Common After a Hospital Stay

A parent can need Medicare-covered home health and still need private-pay home care. That is not a failure to understand the system. It is how the system is divided.

Take a parent coming home after a hip fracture. The doctor may order physical therapy and skilled nursing through a Medicare-certified home health agency if the parent meets the coverage criteria. That covers the clinical recovery piece: mobility work, safety training, medication or wound follow-up if ordered, and progress reporting back to the clinician.

But the same parent may be unable to shower alone, stand long enough to cook, carry laundry, change sheets, or get safely to the toilet at night. Those are real needs. They may also be non-medical home care needs that Medicare does not cover as standalone services. Amedisys describes home health and home care as distinct services that may be used together, with home health focused on medical care and home care focused on daily living support.[6]

This is where families need two lists, not one. List the skilled tasks ordered by the doctor. Then list the daily tasks that still have to be covered when the nurse or therapist is not there. If nobody is assigned to the second list, the work usually falls to the adult child who thought “home health” meant someone would be there for the day.

Need after discharge

Likely category

Question to ask

Physical therapy after surgery

Home health

Has the doctor ordered PT through a Medicare-certified home health agency?

Wound dressing checks

Home health

Is skilled nursing included in the plan of care?

Help showering because standing is unsafe

Often home care, unless limited aide help is part of an eligible home health plan

How many aide visits are actually ordered, and what remains uncovered?

Meal preparation while non-weight-bearing

Home care

Who is cooking when therapy is not present?

Companionship or supervision during the afternoon

Home care

How many hours are needed, and who pays?

What the Cost Difference Looks Like

For approved home health services under Original Medicare, the listed patient cost is $0 for covered home health care services.[1] Again, that does not include every possible item or service in the home, and Medicare’s page separately notes that durable medical equipment has its own cost-sharing rules.[1]

For non-medical home care, families should expect an hourly private-pay model unless another program, long-term care insurance policy, veterans benefit, or state-funded service applies. A Place for Mom reports a national median in-home care cost of about $35 per hour in 2026.[7] SeniorLiving.org, using CareScout/Genworth cost data, reports an average senior in-home care cost of about $34 per hour in 2026, with state figures ranging from $23 per hour in Louisiana to $44 per hour in South Dakota.[8]

At 20 hours per week, those national hourly figures put a family roughly in the $2,720 to $2,800 per month range before considering local minimums, care complexity, agency rules, overtime, or weekend rates.[7][8] Different cost sources use different methods, so do not treat one national number as a quote. Treat it as a warning that “just a few hours a day” can become a serious monthly expense.

That cost reality should not push families to skip needed clinical care. It should push them to classify the needs correctly. If skilled home health is appropriate and covered, use it. If daily assistance remains, price that separately and decide how much can be handled by paid care, family shifts, community programs, or a different living arrangement.

What to Ask Before Discharge

Before your parent leaves the hospital, rehab facility, or emergency department, ask direct questions. Soft answers create unpaid work later.

Is skilled home health being ordered, or are you recommending non-medical help at home?

What skilled service is ordered: nursing, PT, OT, speech therapy, medical social work, or something else?

Which doctor or allowed practitioner will sign and oversee the home health plan of care?

Does my parent meet the homebound requirement as Medicare uses that term?

Is the agency Medicare-certified?

What day will the first visit happen, and who do we call if nobody contacts us?

What daily tasks are not covered by the home health plan?

The last question is the one that protects the family from false confidence. A safe discharge plan should not only say who changes the dressing. It should also say who helps the parent get to the bathroom at 10 p.m. if that is the actual weak point.

If the Answer Is Home Care, Start Planning It as Its Own Service

Once it is clear that the remaining need is non-medical help, switch modes. You are no longer asking whether Medicare will send a nurse. You are deciding how many hours of help are needed, what tasks must be covered, what the family can realistically do, and whether to hire through an agency or a private caregiver.

If your parent’s needs are not tied to a recent hospital stay, surgery, fracture, or acute decline, this decision may be less about discharge and more about managing a stable long-term condition. In that case, use the separate home care vs. home health framework for chronic conditions so the plan reflects an ongoing pattern rather than a short recovery window.

The Monday-Morning Action Plan

If discharge is happening now, do these in order.

Ask the discharge planner or doctor whether skilled home health is being ordered, not just whether your parent “needs help.”

Confirm the skilled service, the ordering clinician, the diagnosis or recovery need, and whether the agency is Medicare-certified.

Ask whether your parent is considered homebound for Medicare home health purposes.

Write down the ADL and IADL gaps that remain: bathing, dressing, toileting, meals, laundry, transportation, medication reminders, supervision, and overnight safety.

Separate the covered skilled-care plan from the private-pay daily-help plan.

If the remaining gaps are non-medical, begin home care planning with a real hourly estimate instead of assuming Medicare will fill the schedule.

The right question is not whether your parent deserves help. The right question is which kind of help is being ordered, which kind is being hired, and who is responsible for paying for each one.

Comments

Join the discussion with an anonymous comment.