How Medicare Still Helps After an Assisted Living Move

Reviewed: 2026-07-09

How Medicare Still Helps After an Assisted Living Move

Medicare doesn't pay for assisted living room and board, but it still covers many medical services for residents. This guide explains what benefits remain available after move-in — hospital stays, doctor visits, skilled nursing rehab, home health, and hospice — and how to use them to reduce your family's out-of-pocket costs.

By Editorial Team

new caregiver

experienced caregiver

long-distance caregiving

spousal caregiver

working caregiver

daily routines

medication management

personal hygiene

care coordination

first steps

ADLs

IADLs

“Medicare doesn’t cover assisted living” is true only if everyone is talking about the assisted living bill itself: the apartment, meals, help with bathing or dressing, medication reminders, housekeeping, and the other daily support that makes the place livable. Medicare says plainly that it does not cover most long-term care, including non-skilled personal care and room and board in assisted living facilities.[1]

That does not mean Medicare stops mattering after your parent moves in. The resident still has a Medicare card. Hospital stays, doctor visits, outpatient care, screenings, some home health services, hospice, and short-term skilled nursing facility rehab may still be covered when the usual Medicare rules are met.[2]

That split is the part families need to hold onto: assisted living is the housing and daily-support setting; Medicare pays for eligible medical care delivered to or used by the person who lives there. If those two streams get blurred, families either expect Medicare to pay an invoice it will not touch, or they stop asking about covered medical benefits that could still reduce out-of-pocket costs.

Separate the assisted living invoice from the medical bills

The monthly assisted living bill is usually built around room, board, supervision, meals, activities, and personal assistance. Those services are valuable, but Medicare treats them as custodial or supportive care rather than skilled medical care. That is why the bill from the facility and the bill from a physician’s office live under different payment rules.

A resident may receive help from assisted living staff every morning and still have a Medicare-covered cardiology visit that afternoon. A nurse may come into the facility under a home health order, or the resident may be transported to an outpatient imaging appointment. The address has changed; the Medicare coverage category has not automatically changed with it.

AARP makes the same practical distinction when explaining why Medicare generally does not pay for assisted living or long-term nursing home custodial care, even though Medicare can cover skilled care in specific medical settings and situations.[3] For a caregiver, that distinction is not academic. It tells you which office to call, which question to ask, and which denial may be worth challenging.

What your parent needs

Where Medicare may still fit

Caregiver question to ask

Monthly assisted living rent, meals, supervision, personal care

Generally not covered by Medicare

Is any part of this invoice medical, or is it all room, board, and custodial support?

Hospital care after an acute illness or injury

Part A may apply

Was my parent admitted as an inpatient or kept under observation?

Doctor visits, outpatient tests, therapy, durable medical equipment

Part B may apply

Is the provider billing Medicare, and what cost-sharing applies?

Short-term rehab after a qualifying hospital stay

Skilled nursing facility benefit may apply

Did the stay meet the 3-day inpatient rule, and is the SNF Medicare-certified?

Intermittent skilled care at the assisted living facility

Home health benefit may apply if eligibility rules are met

Has a physician ordered home health, and is my parent homebound under Medicare rules?

End-of-life care

Hospice benefit may apply if criteria are met

Has the doctor certified hospice eligibility, and what services will the hospice team provide?

What Medicare can still cover after move-in

The cleanest way to think about Medicare and assisted living is to stop asking whether Medicare covers the facility and start asking what kind of service is being billed. The same resident can have several payment streams running at once: private funds or another program for assisted living, Medicare for covered medical care, a supplemental or Medicare Advantage plan for some cost-sharing, and possibly other public benefits outside Medicare.

Hospital care still runs through Medicare Part A

If your parent falls, develops pneumonia, has a stroke, or needs another covered inpatient hospital service, the fact that they live in assisted living does not make them uninsured for hospital care. Original Medicare Part A is still the hospital insurance path when the person is admitted and the stay meets Medicare rules.

The word to listen for is “inpatient.” Families often hear “in the hospital for three nights” and assume that is enough for later skilled nursing facility coverage. It may not be. Observation status can feel identical at the bedside, but it does not count the same way for Medicare’s skilled nursing facility benefit. Before discharge planning moves too far, ask the hospital case manager: “Was this an inpatient admission, and what date did inpatient status begin?”

Doctors, outpatient care, and screenings still run through Medicare Part B

Assisted living staff may notice symptoms, help schedule appointments, or arrange transportation, but the physician visit itself is still medical care. Medicare Part B may cover doctor visits, outpatient services, preventive screenings, diagnostic tests, therapy services, and other covered outpatient care when Medicare requirements are met.[2]

This is where families can lose money quietly. If the facility has a preferred visiting clinician, pharmacy arrangement, therapy provider, or mobile service, do not assume the billing is the same as your parent’s prior doctor. Ask whether the provider accepts Medicare, whether it is in network if your parent has Medicare Advantage, and whether the service is being billed as covered outpatient care or as a private convenience charge.

Home health may apply inside assisted living, but only when the medical criteria are met

The phrase “home health” can be misleading after an assisted living move because the resident’s home is now a facility apartment. Medicare’s home health benefit is not a way to pay the assisted living aides who help every day with meals, toileting, transfers, or reminders. It is a medical benefit for eligible services ordered by a doctor, such as intermittent skilled nursing or therapy, when the person meets Medicare’s requirements.

A useful question is not “Can Medicare pay for more help?” but “Has there been a medical change that might qualify for home health?” After a hospitalization, medication change, wound, decline in mobility, or new therapy need, the discharge planner or primary-care clinician can tell you whether a home health referral is appropriate. The assisted living facility may coordinate with the agency, but the agency’s Medicare eligibility and billing are separate from the facility’s monthly fee.

Hospice can be provided where the resident lives

Hospice is another benefit families sometimes miss because they think of it as a place. Under Medicare, hospice is a benefit for people who meet hospice eligibility criteria, and care can often be delivered where the person lives, including an assisted living facility.[2]

Hospice does not convert the assisted living room-and-board bill into a Medicare-covered charge. The facility still charges for housing and daily support. What changes is that the hospice team may cover and coordinate services related to the terminal illness under the hospice benefit. When a parent’s goals shift from repeated hospital transfers to comfort-focused care, ask the physician and facility whether a hospice evaluation is appropriate and how hospice staff and facility staff divide responsibilities.

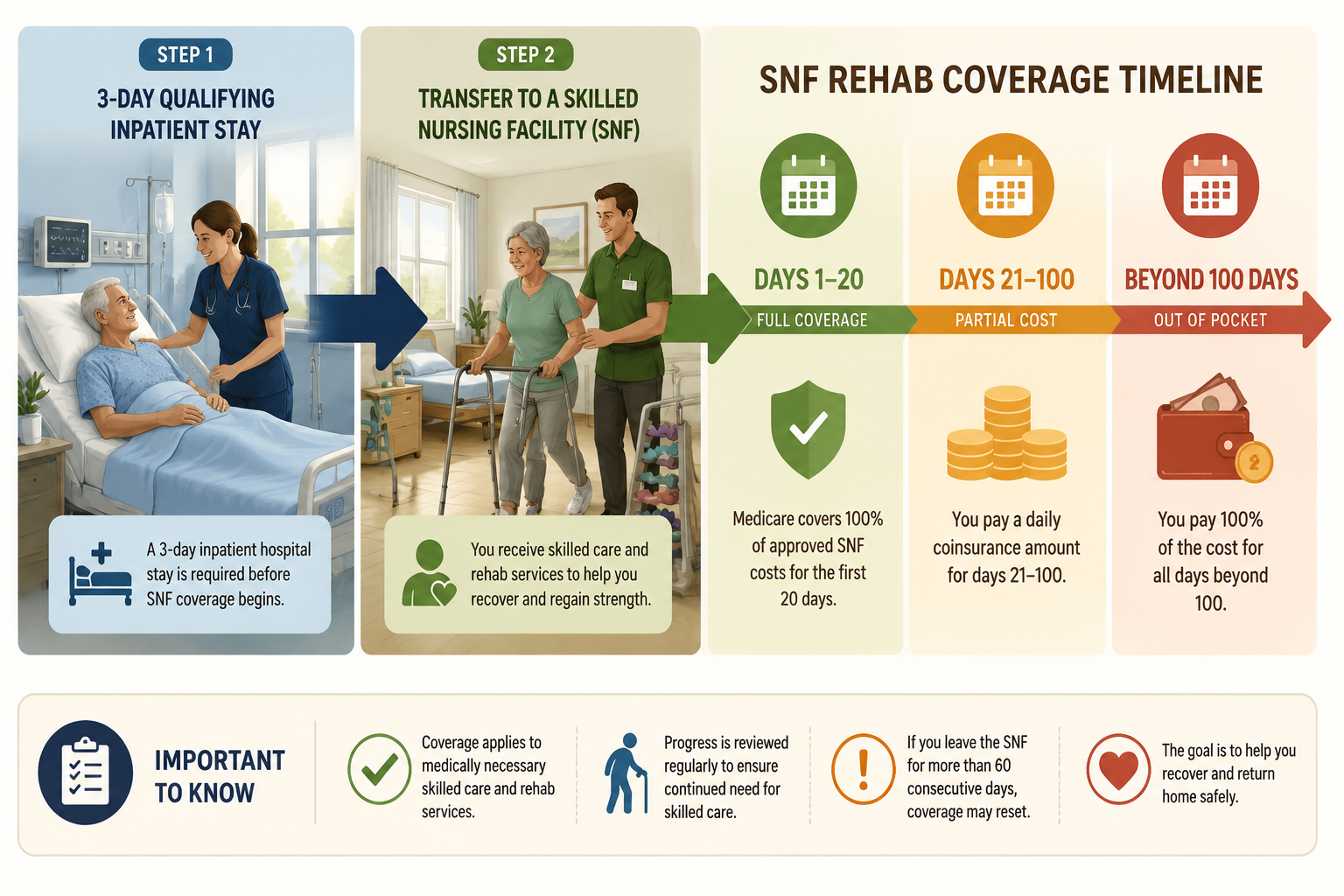

The skilled nursing rehab benefit is the big one families need to understand before discharge

The most consequential Medicare benefit after an assisted living move is often not inside assisted living at all. It is short-term care in a Medicare-certified skilled nursing facility after a qualifying hospitalization. This is the rehab pathway people usually mean when they say, “Medicare paid for rehab after Mom broke her hip.”

Medicare’s skilled nursing facility coverage can last up to 100 days in a benefit period, but only when the requirements are met. One central requirement is a qualifying 3-day inpatient hospital stay before the SNF admission.[4]

In 2026, the cost-sharing structure for covered SNF care under Original Medicare is $0 for days 1 through 20, $217 per day for days 21 through 100, and all costs after day 100 in the same benefit period.[4] That day-by-day structure is why the discharge paperwork matters. A family may be looking at a short rehab stay with little Medicare cost-sharing, a longer stay with a daily coinsurance charge, or a noncovered stay if the qualifying rules were not met.

SNF days in a Medicare benefit period

2026 Original Medicare cost-sharing

What to verify

Days 1-20

$0 for covered services

The SNF is Medicare-certified and the stay follows a qualifying inpatient hospital stay

Days 21-100

$217 per day for covered services

Whether a Medigap policy, retiree coverage, Medicaid, or Medicare Advantage plan changes the family’s actual bill

Day 101 and after

All costs out of pocket

Whether continued stay is still skilled rehab, long-term custodial care, or another level of care

The benefit-period language can feel like fine print until someone is on day 19 and the social worker is talking about next steps. Medicare’s 100-day limit is not a promise that every person receives 100 days. Coverage depends on continued need for skilled care and the other Medicare rules. A resident can be discharged earlier if skilled goals are met or if the care no longer qualifies.

This is also where “assisted living” and “skilled nursing facility” get mixed up. A skilled nursing facility is a medical rehab or nursing setting that can bill Medicare for covered skilled care. An assisted living facility is a residential support setting. Your parent may go from assisted living to the hospital, then to a SNF for rehab, then back to assisted living. Medicare may be relevant at the hospital and SNF stages, while the assisted living room-and-board bill remains outside Medicare.

If a hospital discharge planner says “rehab,” slow the conversation down. Ask where the rehab will happen, whether the facility is a Medicare-certified SNF, whether your parent had a qualifying inpatient stay, what day of the SNF benefit period this is expected to be, and what happens if therapy recommends discharge before the family feels ready. For more on the transition period itself, see how to pay for short-term elder care.

Why the distinction matters financially

The reason families keep circling back to Medicare is obvious: assisted living is a large recurring bill, and a parent’s income usually covers only part of it. Recent cost figures show a June 2026 median assisted living cost of $6,313 per month and a January 2026 average Social Security benefit of $2,071 per month. Those figures should not be treated as a quote for any one facility, but they explain why even partial medical coverage matters.

Medicare will not erase the monthly assisted living charge. But if it properly covers a hospital admission, outpatient specialist visits, home health episode, hospice services, or a short-term SNF stay, the family’s total cash exposure can still be very different from what it would be if every medical bill were paid privately.

This is why a blunt “no, Medicare does not pay for assisted living” is incomplete advice. It answers the facility-invoice question and leaves the caregiver with no map for the next bill. A better working rule is: Medicare does not pay for assisted living as housing, but Medicare may still pay for covered medical care the resident needs.

Medicare Advantage adds network rules, not a new assisted living entitlement

If your parent has Medicare Advantage instead of Original Medicare, do not assume the answer is either better or worse without checking the plan. Medicare Advantage plans must cover Medicare-covered services, but they can use networks, prior authorization, referral rules, and plan-specific cost-sharing. A hospital, SNF, home health agency, or visiting clinician that works smoothly for one resident may be out of network or require extra steps for another.

The practical question becomes: “How does this plan cover the same service?” For a planned outpatient procedure, call before the appointment. For a hospital discharge to rehab, ask the case manager and the plan which SNFs are in network and what authorization is required. For home health, ask which agencies the plan uses and whether the physician’s order has been accepted.

Some Medicare Advantage plans offer supplemental benefits, but those benefits vary by plan and do not turn ordinary assisted living rent and custodial care into a standard Medicare-covered service. Treat plan extras as something to verify in the Evidence of Coverage, not as something to assume from a brochure.

The narrow I-SNP exception is worth knowing, not counting on

Institutional Special Needs Plans, or I-SNPs, are a type of Medicare Advantage Special Needs Plan for people who need an institutional level of care for 90 or more consecutive days.[5] They are often discussed in connection with nursing home residents, and in some circumstances plan design and state policy may make an assisted living resident eligible.

That “may” is doing important work. I-SNP availability depends on where your parent lives, what plans operate there, how the plan defines eligibility, and whether the resident meets institutional-level-care criteria. It is not a general workaround for assisted living costs and should not be the first assumption in a family budget.

If your parent has complex needs and the facility mentions an I-SNP, ask for the plan documents, eligibility criteria, provider network, drug coverage, prior authorization rules, and what changes compared with the current Medicare coverage. The right comparison is not “I-SNP or nothing.” It is “this specific plan versus the coverage my parent already has.”

When the need is long-term custodial support, look beyond Medicare

Once the main cost is ongoing help with daily living rather than short-term medical treatment, Medicare is usually the wrong payer to keep pressing. Families then have to look at private funds, long-term care insurance, state Medicaid programs, veterans benefits, and local support programs. For a broader view of those payment streams, see how to pay for senior care in 2026.

Medicaid is the public program families most often hear about next, but it is state-specific and does not work like Medicare. KFF reported that 41 states cover home care services in assisted living facilities through home- and community-based services waivers, while only 10 states require assisted living facilities to accept new Medicaid residents.[6] That means Medicaid may be important, but availability, eligibility, waitlists, covered services, and facility participation can vary sharply.

VA Aid & Attendance is also separate from Medicare. It may help some eligible veterans or surviving spouses with care-related costs, but it is not a Medicare benefit and should be evaluated under VA rules. The same is true of long-term care insurance: it may help with assisted living if the policy covers it, but the answer sits in the policy contract, not in Medicare.

If your family is still comparing care settings, the payment answer should be part of the placement decision. Assisted living, home care, and nursing home care are not interchangeable medically or financially. A resident who mainly needs supervision and meals is in a different situation from someone who needs 24-hour skilled nursing. For cost and setting comparisons, see home care vs. assisted living vs. nursing home.

What to verify after your parent moves in

After move-in, the job is not to make Medicare pay for assisted living. It is to keep the covered medical pieces from falling through the cracks while you solve the long-term support bill separately.

Keep Medicare coverage active and confirm whether your parent has Original Medicare, Medicare Advantage, Medigap, retiree coverage, Medicaid, or another payer that changes cost-sharing.

For any hospital stay, ask whether your parent is admitted as an inpatient or under observation, and write down the inpatient admission date.

Before a rehab transfer, confirm the facility is a Medicare-certified skilled nursing facility and ask how the 2026 SNF day limits and cost-sharing apply.

When your parent’s condition changes, ask the physician whether home health or hospice criteria may be met instead of assuming the assisted living facility must handle everything privately.

If a Medicare Advantage plan or I-SNP is suggested, review the actual plan rules, network, authorizations, and eligibility before changing coverage.

For the ongoing custodial-care bill, look beyond Medicare to Medicaid, veterans benefits, long-term care insurance, savings, home-sale planning, or other family resources.

Families who keep those categories separate are in a better position to question the right bill. The assisted living invoice has one logic. The resident’s medical care has another. Medicare still belongs in the second conversation.

Comments

Join the discussion with an anonymous comment.