How Much Does Senior Health Care Cost in 2026? A Guide for Family Caregivers

This guide breaks down the real costs of senior health care in 2026, explains what Medicare and Medicaid do and don't cover, and offers actionable budgeting strategies for family caregivers managing care at home.

By Editorial Team

new caregiver

experienced caregiver

long-distance caregiving

spousal caregiver

working caregiver

daily routines

medication management

personal hygiene

care coordination

first steps

ADLs

IADLs

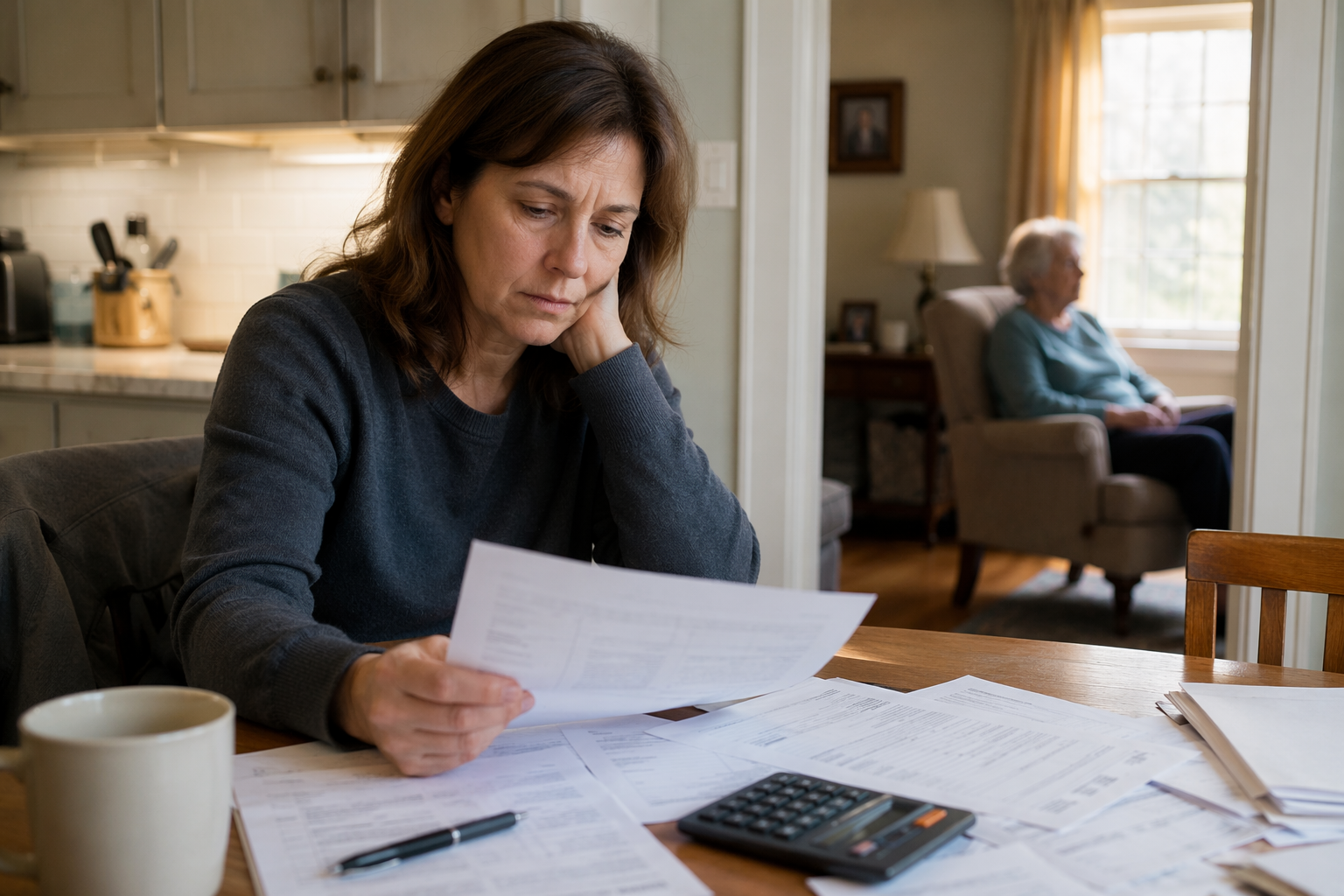

The most expensive misunderstanding in senior health care is the belief that Medicare will pay when an aging parent needs help getting through an ordinary day. Families usually do not learn the boundary in a benefits seminar. They learn it after Dad has fallen twice, Mom is no longer safe in the shower, or a spouse has been sleeping in a chair because nighttime wandering has become part of the household routine.

In 2026, the first budget shock is often home care. A Place for Mom’s 2026 market estimate puts median non-medical in-home care around $34 to $35 per hour, with state-level estimates ranging from about $25 to $44 per hour.[1] That sounds manageable when the family is picturing “a few hours.” It looks different when the care plan says 20 hours a week, help with bathing, meal preparation, medication reminders, transportation, and someone reliable enough to show up every Tuesday and Thursday.

At $35 an hour, 20 hours a week is about $36,400 a year before taxes, agency minimums, holiday rates, supplies, and everything the family is still doing unpaid. At 44 hours a week, the same hourly rate annualizes to a little over $80,000.[1] That is why the real question is not “How much does senior health care cost?” It is “How many hours of which kind of care are we actually buying, and for how long?”

Family caregivers also spend their own money. An AARP Public Policy Institute survey reported that family caregivers spent nearly $7,000 out of pocket in 2016, equal to about 20% of caregiver income; Hispanic and Latino caregivers in that survey spent up to 44% of income.[2] That figure is not fresh enough to use as a clean 2026 price tag, but it still describes the shape of the problem: caregiving expenses do not arrive as one neat invoice. They leak into groceries, gas, copays, home repairs, missed work, and the sibling who keeps saying, “I’ll cover it this month.”

Assisted living is not a cheap fallback, either. CareScout’s cost-of-care data lists assisted living at about $64,200 per year nationally, with substantial variation by state and market.[3] That comparison matters because many families assume aging at home is automatically less expensive. Sometimes it is. Sometimes, once paid help expands from companionship to daily hands-on care, the home-based plan can rival or exceed a residential setting while still leaving family members responsible for coordination.

Start by separating the bills

Senior health care is not one bill. It is a stack of different expenses with different payers, rules, and emotional consequences. A family can make a decent plan only after separating medical care from daily care, and short-term recovery from long-term support.

Cost category

What it often includes

Why families misjudge it

Medical care

Doctor visits, preventive screenings, hospital care, prescriptions, rehabilitation after an illness or injury

Families often assume coverage for medical care means coverage for daily help at home.

Non-medical home care

Help with bathing, dressing, meals, errands, transportation, reminders, supervision, companionship

The hourly rate looks manageable until hours become recurring every week.

Household and safety costs

Grab bars, ramps, bathroom changes, medical equipment, cleaning help, delivery fees, extra utilities

These are rarely listed in the care plan, but they affect the monthly household budget.

Family caregiver costs

Gas, unpaid time, reduced work hours, missed retirement contributions, sibling reimbursements

The person coordinating care often absorbs costs before anyone calls them caregiving expenses.

Residential care comparison

Assisted living, memory care, nursing home care

Families may compare only the monthly rent, not the care level, medication fees, or what Medicaid may or may not cover in their state.

This separation is not bookkeeping trivia. It changes the decision. A parent recovering after surgery may need short-term skilled care, follow-up visits, transportation, and help with meals for a few weeks. A parent with progressive mobility loss may need bathing assistance every Monday, Wednesday, and Friday for the foreseeable future. Those are different financial problems.

If the immediate need is temporary, a narrower guide to paying for short-term elder care can help sort Medicare, Medicaid, VA benefits, and out-of-pocket options. If the need is ongoing help with daily activities, the family needs a longer budget horizon.

What home care really costs when the hours become real

The hourly home care number is useful only after the family translates it into a schedule. “A few hours” can mean three different budgets.

Example schedule

At $35/hour

What it may realistically cover

8 hours/week

About $1,213/month; about $14,560/year

One or two visits for errands, light meal help, companionship, or a bathing routine if the timing is predictable

20 hours/week

About $3,033/month; about $36,400/year

Weekday blocks for personal care, meals, transportation, and respite for the family caregiver

44 hours/week

About $6,673/month; about $80,080/year

Substantial weekday coverage, though not full 24-hour supervision

These are simple calculations from a national market estimate, not a quote from a local agency. State rates, minimum shift rules, weekend pricing, overnight arrangements, caregiver availability, and whether the family hires privately or through an agency can all change the final bill. A family in a lower-cost area may pay less. A family that needs reliable bathing assistance at 7 a.m., dementia supervision, or weekend coverage may find the posted hourly number is only the starting point.

The first practical move is to write down the care schedule before calling it affordable. List the exact days and tasks: bathing, dressing, toileting, meals, laundry, transportation, medication reminders, supervision, social visits, and respite. Then mark which tasks are safety-critical. A missed grocery trip is inconvenient. A missed transfer from bed to wheelchair can become an emergency.

This is also where families need vocabulary. Companion care, personal care, home health, skilled nursing, respite care, and overnight care are not interchangeable labels. For a fuller breakdown of service types, use a guide to elderly help services before comparing prices. If the worry is nighttime wandering, toileting, fall risk, or a spouse who can no longer sleep, look specifically at overnight care costs. Overnight care is a different financial and staffing conversation than a four-hour daytime visit.

The hidden household costs

The care worker’s invoice is only the visible part. Aging at home often brings smaller expenses that repeat quietly: disposable briefs, gloves, wipes, nutritional drinks, medication organizers, extra laundry, transportation, meal delivery, snow removal, lawn care, cleaning help, and pharmacy delivery fees. A daughter may not count the $18 parking fee at the specialist as senior health care. Her checking account does.

Home safety costs can be one-time or staged over several years. Grab bars and better lighting may be modest. A bathroom remodel, ramp, stair lift, or widened doorway can be a major household project. Before spending, families should distinguish convenience changes from medically necessary modifications and keep documentation if they plan to ask a tax professional about deductibility. A home modification decision framework can help prioritize safety changes instead of reacting after each fall or near miss.

Then there is the cost that rarely shows up in family texts: the caregiver’s own finances. Reduced hours at work, unpaid leave, delayed promotions, lower retirement contributions, and credit card balances are not side effects to brush aside. They are part of the cost of care. If one sibling provides labor and another provides money, the family should say that plainly before resentment turns into policy.

What Medicare covers—and where the disappointment begins

Medicare is essential, but it is not a long-term caregiving plan. It is built around medical care: preventive services, acute care, physician services, hospital care, prescription drug coverage through Part D or Medicare Advantage drug coverage, and certain limited post-acute services when eligibility rules are met. Medicare’s own preventive-services guide is full of screenings, vaccines, counseling, and wellness services—not ongoing help with bathing, dressing, cooking, toileting, or supervision at home.[4]

That boundary is where families get hurt. A parent can have Medicare and still need to privately pay for the daily support that keeps them safe at home. Medicare may cover medically necessary skilled care under specific conditions. It generally does not pay for long-term custodial care when that is the only care needed. Custodial care means help with activities of daily living—bathing, dressing, eating, transferring, toileting, and continence support. Those tasks are exactly what many aging-at-home parents need most.

A common family sequence goes like this: Mom is hospitalized, discharged to rehab, improves enough to go home, and everyone assumes Medicare will keep sending help. Then the covered episode ends or the service is limited, but Mom still cannot shower safely. The family is not wrong to feel blindsided. The language sounds similar—home health, home care, skilled care, personal care—but the payment rules are not similar.

Need

Medicare is more likely to be relevant when...

Family should prepare to pay or find another program when...

Preventive care

The service is a covered screening, vaccine, counseling visit, or wellness-related benefit

Transportation, time off work, or follow-up household help is needed

Short-term skilled care

A doctor orders medically necessary skilled services and Medicare conditions are met

The need becomes ongoing personal care rather than skilled medical care

Bathing, dressing, toileting, meals

These are part of a covered skilled episode and not the sole reason for care

The main need is long-term custodial support

Supervision and companionship

There is a covered medical service involved under plan rules

The goal is safety monitoring, social support, or respite for the family caregiver

Medicare Advantage plans may offer supplemental benefits that traditional Medicare does not, and plans vary. Families should read the Evidence of Coverage, ask whether a benefit is medical, supplemental, short-term, or condition-limited, and get the answer in writing when possible. The question is not “Does Mom have Medicare?” The question is “Which exact service is covered, for how many visits or hours, under what conditions, and what happens when that period ends?”

A timely telehealth note

Telehealth can reduce transportation strain, missed work, and the physical toll of getting a frail parent to an appointment. It does not replace hands-on help at home. For 2026 planning, families should also treat telehealth rules as time-sensitive: Medicare telehealth flexibilities have been extended through 2027, according to a 2026 policy update summarizing CMS-related changes.[5] A practical telehealth for seniors guide can help decide when a virtual visit is appropriate and when an in-person exam is still necessary.

Medicaid is the long-term care path many families discover late

Medicaid is often the public program that becomes relevant when long-term care costs outrun private resources. It can help pay for nursing home care and, depending on the state and program, some home- and community-based long-term services. But Medicaid is not one national caregiving benefit that works the same way everywhere.

The state-by-state variation is the part families cannot afford to ignore. Eligibility rules, income limits, asset limits, estate recovery, waiver availability, waiting lists, covered services, and whether certain home care supports are available can differ by state. A family that moves money, adds a name to a deed, pays a relative informally, or sells a home before getting advice may create problems if Medicaid is needed later.

The words “look-back period” should slow everyone down. Medicaid long-term care eligibility commonly examines certain asset transfers made before the application. The details depend on the state and the category of Medicaid involved. Before transferring assets, reimbursing relatives, changing ownership of a home, or assuming a parent will simply “spend down” later, talk with the state Medicaid office, an elder law attorney, or a qualified benefits counselor familiar with local rules.

This is not about protecting an inheritance before protecting care. It is about avoiding a preventable gap: the parent needs help, private funds are depleted, Medicaid is not yet approved, and the adult child is suddenly paying the agency bill on a credit card. That is the kitchen-table crisis many families could have softened with earlier information.

Private pay and family cost-sharing need rules before resentment sets in

When Medicare does not cover the need and Medicaid is not yet available, families enter the private-pay zone. The money may come from the older adult’s income, savings, home equity, long-term care insurance, Veterans benefits if eligible, adult children, or some combination. The cleanest plans are not always the wealthiest ones. They are the ones where everyone can see the same numbers.

A family care budget should include at least four monthly lines: paid care, medical out-of-pocket costs, household support, and caregiver reimbursement. If one person is driving 300 miles a month, buying supplies, and missing work, pretending those costs are “just what family does” may keep the peace for a few weeks. It does not build a sustainable care plan.

Put the parent’s income and recurring expenses in one shared document, if the parent consents or the legal authority is in place.

Separate medical bills from daily-care costs so Medicare assumptions do not hide private-pay obligations.

Name the unpaid labor: scheduling, bathing help, transportation, medication tracking, overnight supervision, bill management.

Agree on which expenses will be reimbursed and how receipts will be handled.

If siblings contribute differently, document whether the difference is money, time, distance, or availability—not love.

Review the plan every few months or after any hospitalization, fall, diagnosis change, or caregiver burnout signal.

Long-term care insurance, if the parent has it, needs an early policy review. Families should check elimination periods, daily or monthly benefit limits, inflation protection, covered settings, caregiver qualifications, and whether care must be provided by a licensed agency. Waiting until the family has already hired help can lead to frustrating denials or delayed reimbursement.

Why the pressure keeps landing on families

Most older adults are not living in nursing homes. Population Reference Bureau analysis reports that only about 5% of older Americans live in nursing homes and that 69% of older adults who receive care get only unpaid care from family members.[6] That explains why so many households feel as if they have stumbled into a private problem with no front desk. For many families, there is no formal system until the crisis is severe enough to force one.

The family bench is also getting thinner. PRB, citing Census Bureau projections, reports that the caregiver support ratio is expected to fall from about 6 potential caregivers per older adult in 2025 to about 3 by 2040.[6] That does not mean every older adult will lack help. It means the old assumption—someone in the family will absorb it—will become harder to sustain.

The unpaid contribution is enormous. AARP has estimated the annual economic value of unpaid family caregiving at $873 billion.[6] That number is useful not because it makes a family’s Tuesday afternoon feel grand, but because it names what usually goes unnamed: unpaid care is labor, and when one household loses that labor capacity, the bill has to be paid somewhere else.

Health and household finances are tied together in less obvious ways, too. America’s Health Rankings’ 2026 Senior Report found that 13% of adults age 60 and older face food insecurity, up 6% from 2022 to 2023.[7] When an older adult cannot reliably afford food, transportation, medication, or safe housing, the caregiving plan becomes a financial triage plan. A family may be discussing home care hours while also quietly paying for groceries.

Build the budget around care levels, not optimism

A workable senior health care budget has to leave room for decline, recovery, and surprises. It should not assume that the current level of need will stay flat because everyone is exhausted by the thought of more help.

Planning question

Why it matters

What can the older adult pay monthly without using emergency reserves too quickly?

This shows how long the current plan can last before Medicaid, housing changes, or family contributions must be considered.

How many paid hours are needed for safety, not comfort?

Safety-critical tasks should be funded first: bathing, transfers, toileting, meals, medication routines, and supervision.

Which family tasks are becoming unsustainable?

The first paid hours often need to replace the task that is breaking the caregiver, not the task that is easiest to outsource.

What would trigger a change in setting?

Repeated falls, unsafe wandering, caregiver illness, or overnight needs may change the math quickly.

What Medicaid rules apply in this state?

Waiting until funds are nearly gone can leave too little time to correct planning mistakes.

What is the caregiver risking financially?

Retirement savings, work stability, credit card debt, and household relationships belong in the plan.

Families often start with the cheapest question: “What is the minimum we can buy?” Sometimes that is necessary. But the better first question is, “Which risk are we trying to reduce?” If the risk is falls in the shower, a weekly companion visit will not solve it. If the risk is caregiver collapse, two hours of help during the parent’s easiest time of day may not help much. If the risk is medication confusion, the plan may need pharmacy packaging, reminders, nurse oversight, or a simpler prescribing routine—not just more generic hours.

Use the market numbers as benchmarks, then localize them. Call at least two agencies and ask about minimum shifts, weekend rates, overnight options, dementia experience, caregiver replacement policies, transportation, and whether the quoted rate includes all fees. If hiring privately, ask about payroll taxes, workers’ compensation, backup coverage, liability, and what happens when the caregiver is sick. A lower hourly rate can become expensive if the adult child becomes the backup plan every time coverage falls through.

Protecting the caregiver’s future is part of the care plan

There is a point in many families when the default caregiver stops using real numbers. She says she is fine. He says the missed work is temporary. The spouse says the nights are manageable because admitting otherwise would force a decision no one wants to make. That is when the care plan becomes financially dangerous.

Protecting the caregiver’s retirement savings, household cash flow, marriage, job, and health is not selfish. It is what keeps the care arrangement from collapsing. If the only plan works because one person silently absorbs every gap Medicare does not cover, it is not a plan. It is a delay.

Senior health care in 2026 is expensive because medical coverage, daily support, housing, food, transportation, and family labor all meet in the same household. Early planning will not make care cheap. It can keep the family from mistaking an emergency expense for a multi-year obligation, from assuming Medicare will pay for custodial care, and from finding Medicaid rules only after decisions have already narrowed. Sustainable caregiving begins when the family puts the whole cost on the table—including the cost borne by the person doing the most.

Comments

Join the discussion with an anonymous comment.