How to Pay for Short-Term Elder Care: Medicare, Medicaid, VA, and Out-of-Pocket Costs in 2026

Most families pay out of pocket for short-term elder care because they misunderstand what Medicare, Medicaid, and VA benefits actually cover. This guide explains exactly what each funding source pays for — and what it doesn't — so you can avoid surprise bills and make a financially sound decision for a temporary care episode.

By Editorial Team

medicare coverage

medicaid waiver

respite care

skilled nursing facility

short-term care

📄

A printable version of this guide is available. Use your browser's print function (Ctrl+P / ⌘P) to save or print.

The Hard Truth: Most Short-Term Care Is Paid Out of Pocket

When a parent is discharged from the hospital after a hip replacement or needs a few weeks of supervision while you recover from your own surgery, the natural assumption is that Medicare or your health insurance will cover the bill. That assumption is almost always wrong — and it costs families thousands of dollars in surprise expenses.

The reality is that most short-term elder care — including respite stays, adult day programs, short-term assisted living, and even some rehabilitation services — is paid entirely out of pocket. A 2025 caregiver survey found that 68% of caregivers report that caregiving has created at least some financial strain, and much of that strain comes from uncovered care episodes that families did not anticipate.

The gap between what families expect insurance to cover and what it actually covers is the central problem this guide addresses. Medicare, Medicaid, and VA benefits each cover specific types of short-term care under specific conditions — and the conditions are narrower than most people realize. Understanding exactly what each funding source pays for, and what it does not, is the difference between a financially manageable short-term care episode and a cascade of uncovered costs.

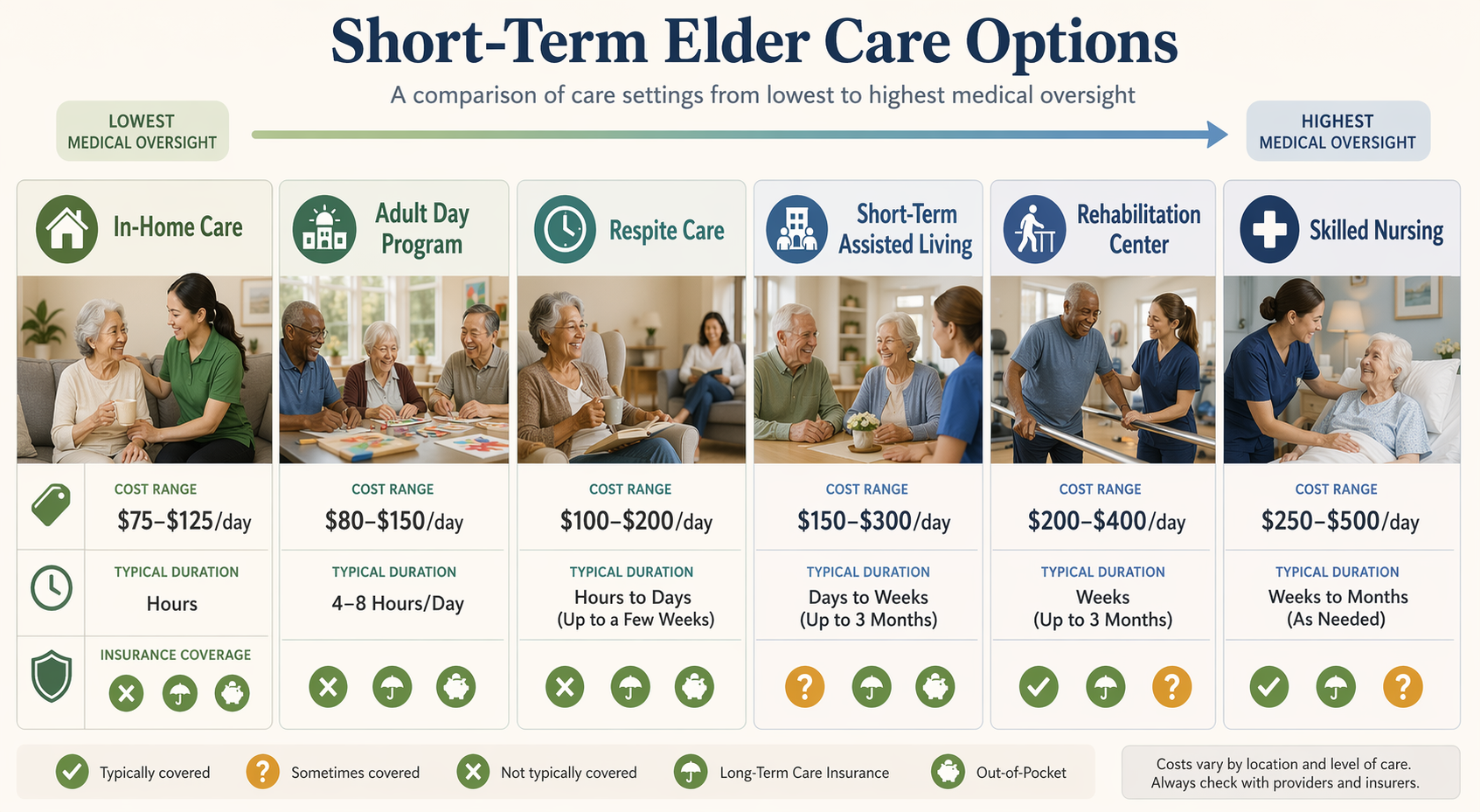

Short-term elder care options span a wide range of costs and medical oversight levels. Most are paid out of pocket.

Medicare Part A: Skilled Nursing Facility (SNF) Coverage

Medicare Part A covers skilled nursing facility care, but only under a specific set of circumstances that many families do not fully understand. This is the only short-term care scenario that Medicare covers comprehensively, and even then, the coverage has strict limits.

The Qualifying Criteria

For Medicare to pay for a skilled nursing facility stay, all of the following conditions must be met:

The senior must have had a qualifying inpatient hospital stay of at least 3 consecutive days (not including the day of discharge).

They must enter a Medicare-certified SNF within a short time of leaving the hospital — generally within 30 days.

They must need daily skilled care, such as nursing services or physical therapy, that can only be provided in a skilled nursing facility.

A doctor must certify the need for daily skilled care.

2026 Cost Breakdown

For each benefit period in 2026, Medicare Part A covers SNF care according to the following structure:

Medicare Part A Skilled Nursing Facility coverage in 2026. Source: Medicare.gov.

Days

Cost to You

What Medicare Pays

Days 1–20

$0

Full cost after the Part A deductible ($1,736 per benefit period)

Days 21–100

$217 per day

All costs above the daily coinsurance amount

Day 101 and beyond

All costs

Nothing

The benefit period begins the day you enter a Medicare-certified SNF and ends after you have been out of the facility for 60 consecutive days. If you re-enter a SNF after a new 60-day gap, a new benefit period starts, and the deductible applies again.

Medicare Part A SNF coverage timeline for 2026. The 3-day qualifying hospital stay is the critical gate.

What This Means for Short-Term Care Planning

If your parent needs a short-term rehabilitation stay after a hip replacement or stroke, and they meet the qualifying criteria, Medicare will cover the first 20 days in full. Days 21 through 100 will cost $217 per day out of pocket — a significant expense that many families do not budget for. After day 100, the full cost of the SNF stay falls on the family.

It is also critical to understand that observation stays — where a patient is in a hospital bed but classified as "under observation" rather than "admitted" — do not count toward the 3-day qualifying stay. This distinction has caught many families off guard, resulting in denied SNF coverage.

Medicare and Respite Care: Only Under the Hospice Benefit

One of the most persistent misconceptions among family caregivers is that Medicare covers respite care — a short-term stay designed to give the primary caregiver a break. The truth is far more limited.

Medicare Part A covers respite care only when the senior is already enrolled in the hospice benefit. Under that benefit, Medicare will pay for up to 5 consecutive days of respite care in a Medicare-approved hospital, skilled nursing facility, or hospice inpatient unit. The respite stay can be used no more than once per benefit period.

Some Medicare Advantage (Part C) plans may offer respite care as a supplemental benefit, but this is not guaranteed. You must check your specific plan's benefits document. For most families, respite care — whether at home, in an adult day center, or in a facility — is a private-pay expense.

For a detailed breakdown of how respite care differs from home health, home care, and hospice, see our side-by-side comparison guide.

Medicaid: State-Dependent Waiver Programs, Not a Standard Benefit

Medicaid is often cited as a potential funding source for short-term care, but the reality is that respite care and short-term custodial care are not standard Medicaid benefits. Coverage depends entirely on state-specific waiver programs, primarily Home and Community-Based Services (HCBS) waivers.

These waivers allow states to offer services — including respite care, adult day health, and in-home personal care — to seniors who would otherwise require nursing home care. However, the availability, eligibility criteria, services covered, and waitlist lengths vary dramatically from state to state.

Some states offer generous respite coverage through HCBS waivers, while others have limited or no respite benefits.

Eligibility is typically based on both financial need (income and asset limits) and functional need (requiring a nursing home level of care).

Waitlists for HCBS waivers can be months or even years long in some states, making them impractical for an immediate short-term care need.

For recipients already enrolled in a Medicaid HCBS waiver, some states will pay for inpatient respite care in an approved facility — the first 5 days at 100% of cost, and after that at the rate of routine home care.

VA Benefits: Up to 30 Days of Respite Care for Eligible Veterans

For families of veterans, the Department of Veterans Affairs offers one of the most generous short-term care benefits available — but it is still underutilized because many families do not know it exists.

Respite care is part of the Veterans Health Administration Standard Medical Benefits Package. All enrolled veterans are eligible if they have a clinical need for respite care. The VA offers two main types:

Home respite care: A home health aide or nurse comes to the veteran's home to provide care while the primary caregiver takes a break.

Nursing home respite care: The veteran stays in a VA facility or a community nursing home for a short period, typically up to 30 days per year.

The cost to the veteran depends on their service-connected disability status and financial situation. Some veterans pay nothing; others may have a copay. The National Council on Aging confirms that eligible veterans may receive up to 30 days of respite care per year in a VA facility.

Additional VA Benefits That Can Help

Beyond the standard respite benefit, the VA offers two other programs that can help fund short-term care:

VA Aid and Attendance: A monthly cash benefit added to the veteran's pension for those who need help with daily activities. This money can be used to pay for in-home care, adult day care, or assisted living.

VA Housebound Benefit: A similar monthly cash benefit for veterans who are substantially confined to their home due to a permanent disability.

To apply for VA respite care, contact the social work department at your local VA medical center. For Aid and Attendance or Housebound benefits, you will need to file a claim with the VA Pension Management Center.

Long-Term Care Insurance: Policy-Dependent, Often Overlooked

Long-term care insurance policies vary so widely that it is impossible to make a general statement about what they cover. However, many policies do include benefits for short-term care — if the policy was purchased before the care was needed.

Common short-term care benefits found in LTC insurance policies include:

Respite care coverage: Some policies reimburse a portion of respite care costs, either at home or in a facility.

Home health care coverage: Many policies cover in-home care services, which can be used for short-term post-hospital recovery.

Adult day services: Some policies include coverage for adult day programs.

Nursing home and assisted living coverage: Most policies cover facility-based care, but typically with an elimination period (a waiting period of 30 to 90 days before benefits begin).

The key takeaway is that long-term care insurance can be a valuable resource for short-term care, but only if the policy was purchased before the need arose and only if the specific type of care you need is covered. Contact the insurance company directly to verify coverage before making any commitments.

Private Pay: What Short-Term Care Actually Costs in 2026

For the majority of families, short-term elder care is a private-pay expense. Understanding the actual costs is essential for budgeting and avoiding financial surprises.

Average daily costs for common short-term elder care types in 2026. Sources: StoryPoint, A Place for Mom, Genworth Cost of Care Survey.

Care Type

Daily Cost Range

Typical Duration

Insurance Coverage

Adult day programs

$75–$125 per day

4–10 hours per day

Some Medicaid waivers; rarely covered by Medicare

Short-term assisted living

$99–$250+ per day

1–4 weeks

Almost always private pay

In-home care (home health aide)

$150–$300 per day

2–8 hours per day

Medicare covers only skilled home health; custodial care is private pay

Rehabilitation center

$200–$500 per day

1–4 weeks

Often covered by Medicare if qualifying criteria are met

Skilled nursing facility

$250–$500 per day

Up to 100 days (Medicare)

Medicare covers days 1–20 fully; days 21–100 at $217/day coinsurance

Hospice respite care

$10,000–$15,000 per month

Up to 5 days per stay

Covered by Medicare Part A under the hospice benefit

These costs add up quickly. A two-week stay in a short-term assisted living community at $175 per day totals $2,450. A month of in-home care at $200 per day totals $6,000. For families who assumed Medicare would cover these expenses, the financial impact can be devastating.

For a deeper look at home care costs and how to build a layered funding strategy, see our guide on affording $34–$35/hour care.

A quick-reference comparison of the four main payment pathways for short-term elder care.

State and Local Programs: The National Family Caregiver Support Program and Area Agencies on Aging

While federal programs like Medicare and Medicaid get most of the attention, state and local programs can be a valuable source of funding for short-term care — especially for families who do not qualify for VA benefits or Medicaid.

National Family Caregiver Support Program (NFCSP)

The NFCSP, administered through local Area Agencies on Aging (AAAs), provides grants to states to support family caregivers. These grants can be used for a range of services, including:

Respite care vouchers or subsidies

Counseling and support groups

Caregiver training and education

Supplemental services (e.g., home modifications, assistive devices)

Funding is limited and varies by state, but the NFCSP is one of the few federal programs specifically designed to support family caregivers. To find your local AAA, call the Eldercare Locator at 1-800-677-1116 or visit the ACL website.

State-Funded Sliding-Scale Adult Day Centers

Some states fund adult day centers that operate on a sliding-scale fee structure based on income. These programs can be an affordable option for short-term care, with daily costs as low as $30–$50 for qualifying families. Availability varies widely, and waitlists are common.

To find these programs, contact your local Area Agency on Aging or state department of aging. They can provide a list of licensed adult day centers in your area and information about any state-funded subsidies.

Action Checklist: What to Ask Before Committing to Any Short-Term Care Arrangement

Before you sign any agreement or make a payment, use this checklist to ensure you understand the full financial picture. These questions will help you avoid surprise bills and identify funding sources you may have overlooked.

Does this facility or agency accept Medicare, Medicaid, or VA benefits? Get the answer in writing.

If Medicare is an option, does the senior meet the qualifying criteria — specifically, the 3-day inpatient hospital stay requirement?

What is the daily or hourly rate, and what services are included in that rate? Ask for a complete list of included services and any additional fees.

Are there any hidden fees — such as admission fees, assessment fees, or charges for laundry, transportation, or medication management?

What is the cancellation policy? Can you end the stay early without penalty? Is there a trial period?

If the senior has long-term care insurance, what is the elimination period, daily benefit maximum, and any exclusions that apply to short-term care?

Have you contacted your local Area Agency on Aging to ask about NFCSP grants or state-funded respite subsidies?

If the senior is a veteran, have you contacted the local VA medical center to inquire about respite care eligibility?

For a broader overview of all senior care funding options, including long-term care, see our comprehensive guide to paying for senior care in 2026. And if you are still deciding which type of short-term care is right for your situation, our crisis decision guide can help you evaluate your options under time pressure.

Comments

Join the discussion with an anonymous comment.