Home Care vs. Assisted Living: The Cost Crossover Point Every Family Needs to Know in 2026

A data-driven guide for adult children deciding between in-home care and a facility for an aging parent. We analyze the 40–50 hour per week cost tipping point, provide a monthly cost calculator by hours of care, and offer a 7-factor decision matrix to help you make the right financial and personal choice.

By Editorial Team

home care costs

assisted living costs

cost comparison

decision guide

new caregiver

The $6,200 Question: Home Care or Assisted Living?

Every week, families across the country sit down at a kitchen table with a notebook and a knot in their stomach. The question is always the same: can we afford to keep Mom at home, or is it time to look at assisted living? The answer used to be simple — home care was cheaper, end of discussion. That is no longer true.

In 2026, the national median cost of assisted living is $6,200 per month (CareScout 2025 data). The national median for non-medical home care is $34–$35 per hour (A Place for Mom, CareScout, SeniorLiving.org). Do the math at 44 hours per week — roughly six hours of daily care — and monthly home care costs hit $6,478, essentially the same as assisted living. This is the crossover point, and it changes the entire decision framework.

This article is built around a single, actionable thesis: the cost tipping point between home care and facility care is approximately 40–50 hours per week of in-home care. Below that threshold, home care is often more affordable and more flexible. Above it, assisted living or memory care may be more cost-effective, especially when you factor in 24/7 supervision, meals, and social engagement. We will walk through the national numbers, build a monthly cost calculator you can use right now, examine the hidden costs on both sides, and give you a seven-factor decision matrix that goes far beyond the spreadsheet.

National 2026 Median Costs: The Baseline Numbers

Before you can calculate your family's crossover point, you need the national benchmarks. These are the numbers that every financial planner, social worker, and elder law attorney will reference. They are also the numbers that most online articles present in isolation — without showing you how they connect.

National median costs for senior care options in 2026. All figures are U.S. national medians; local rates vary.

Care Type

National Median Cost (2026)

Source & Year

Non-medical home care (hourly)

$34–$35 per hour

A Place for Mom ($34, 2026); CareScout ($35, 2025); SeniorLiving.org ($35, 2026)

Home care (44 hrs/week, monthly)

$6,478

A Place for Mom (2026)

Assisted living (monthly)

$6,200

CareScout (2025)

Memory care (monthly)

$6,000–$7,500

Senioridy (2026)

Nursing home, semi-private (monthly)

$9,581

CareScout (2025)

Nursing home, private room (monthly)

$10,798

CareScout (2025)

24/7 in-home care (168 hrs/week, monthly)

$25,479

U.S. News / CareScout (2025)

A few things jump out immediately. First, the gap between home care and assisted living has narrowed dramatically. In 2020, the difference was roughly $1,500–$2,000 per month in favor of home care. Today, at 44 hours per week, the difference is essentially zero at the national median. Second, the cost of a nursing home — even a semi-private room — is in a completely different tier. If your parent needs skilled nursing care, the home care vs. assisted living debate becomes secondary; the real question is whether home health care is a viable alternative to a facility.

Monthly Cost Calculator: How Much Home Care Will You Really Need?

The single most useful thing you can do right now is estimate how many hours of paid care your parent actually needs each week. Most families overestimate at first — they assume 24/7 coverage is required — but a honest assessment of activities of daily living (ADLs) often reveals a much lower number. The table below shows what each level of weekly care costs at the national median rate of $34 per hour.

Monthly home care costs at different weekly care levels, calculated at the national median rate of $34/hour (A Place for Mom, 2026). Actual costs vary by location and agency.

Morning and evening assistance with bathing, dressing, meals

30 hours

~4 hours/day

$4,416

Half-day coverage; help with multiple ADLs plus meal prep

44 hours

~6 hours/day

$6,478

Full daytime coverage; aligns with assisted living median cost

168 hours

24/7 (3 shifts)

$25,479

Round-the-clock care; typically requires live-in or multiple aides

Notice the progression. At 7 hours per week — a few hours of companionship and light help — home care is dramatically cheaper than any facility option. At 15 hours, it is still well below assisted living. At 30 hours, the monthly cost ($4,416) is approaching the assisted living median ($6,200) but still leaves room. At 44 hours, the two costs converge. This is why the 40–50 hour range is the critical decision zone.

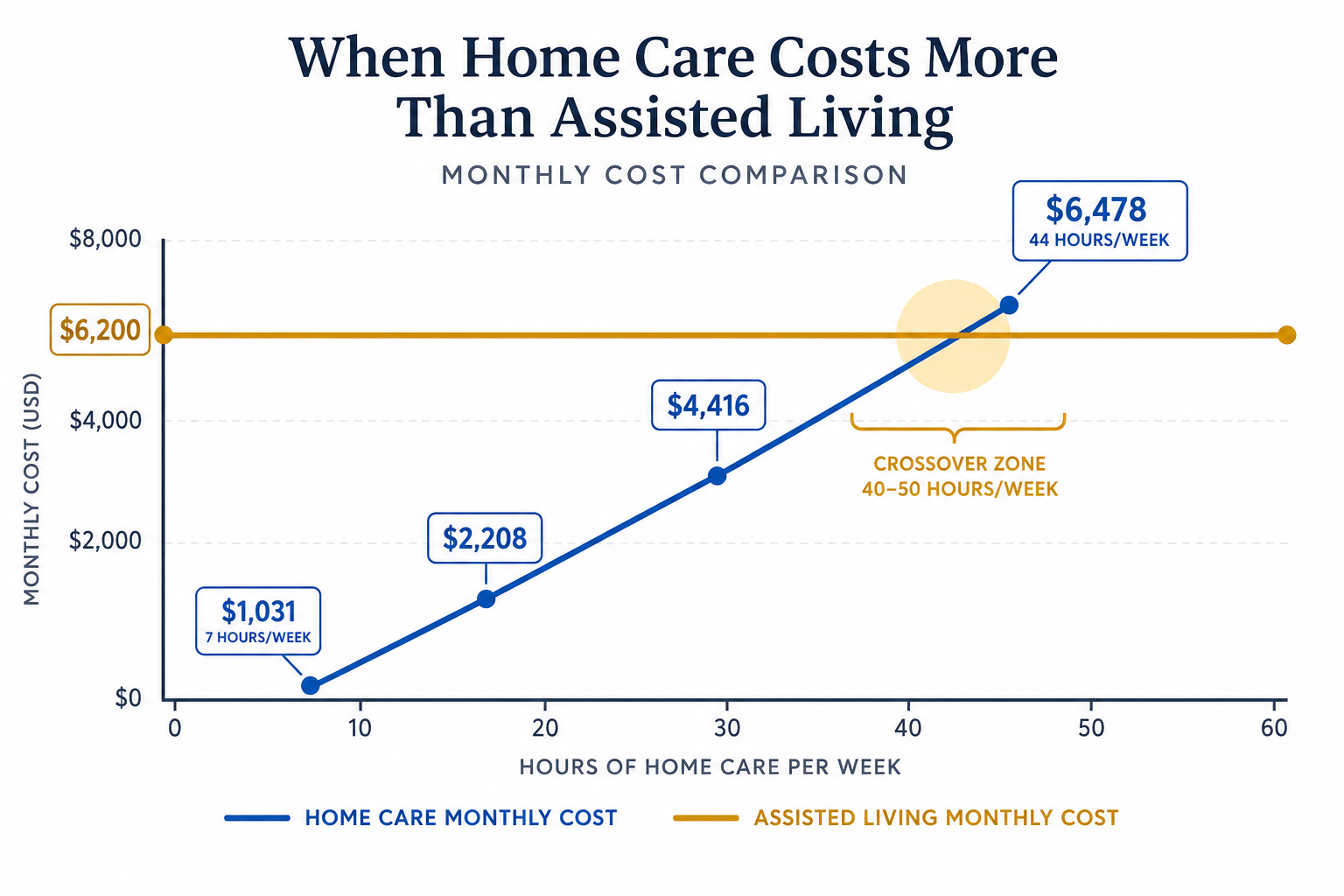

The Crossover Point: When Home Care Costs More Than Assisted Living

The crossover point is not a fixed number — it is a range between 40 and 50 hours per week of paid in-home care. Below this range, home care is almost always the more affordable option. Above it, the financial equation flips, and facility care often becomes the lower-cost choice, especially when you account for what is included in the monthly fee.

The cost crossover point: home care vs. assisted living at the national median. The yellow zone (40–50 hrs/week) is where the decision becomes financially neutral.

Why does this happen? Home care is priced by the hour, and every additional hour adds to the monthly total. Assisted living is a fixed monthly fee that covers rent, meals, housekeeping, activities, and 24/7 staff availability. Once your parent needs more than about six hours of daily paid care, the fixed-price model of assisted living becomes competitive — and often cheaper — than the hourly model of home care.

There is an important nuance here. The crossover analysis assumes that the family is paying for all care hours out of pocket. If a spouse or adult child is providing a significant portion of the care — say, 20 hours per week — then the paid care hours may be much lower, and home care remains the clear financial winner. The crossover point applies to paid care hours only.

For families exploring the live-in caregiver model — where a single aide lives in the home and provides up to 16 hours of daily care — the cost structure is different. A live-in caregiver typically costs $20,000–$24,000 per month (Senioridy, 2026), which is significantly more than assisted living but less than a nursing home. If you are considering this option, our companion guide on live-in caregiver vs. assisted living costs provides a detailed comparison.

Hidden Costs and Hidden Benefits of Each Option

The hourly rate and the monthly fee are only the beginning. Both home care and assisted living come with costs and benefits that do not show up on a rate sheet. Ignoring them can lead to a decision that looks right on paper but fails in practice.

Hidden Costs of Home Care

Home modifications: Grab bars, ramps, stair lifts, walk-in tubs, and widened doorways can cost $500–$15,000 depending on the scope. Our aging-in-place remodel cost guide breaks down the numbers.

Medical equipment: Hospital beds, lift systems, oxygen concentrators, and mobility aids are often not fully covered by Medicare.

Increased utility and household costs: More laundry, more cooking, higher heating and cooling bills when someone is home all day.

Family caregiver unpaid labor: The National Alliance for Caregiving estimates that family caregivers provide an average of 20+ hours per week of unpaid care. At $34/hour, that is an implicit cost of nearly $35,000 per year — money that shows up as lost wages, reduced retirement savings, and increased stress.

Agency markup: Home care agencies typically charge 20–30% more than independent caregivers (SeniorLiving.org, Senioridy). The markup covers bonding, insurance, background checks, and backup coverage.

Hidden Benefits of Home Care

One-on-one attention: Your parent gets a caregiver's undivided focus, not a staff member responsible for 10–15 residents.

Familiar environment: 93% of adults aged 55+ want to age in place (U.S. News survey). Staying home reduces confusion, anxiety, and disorientation, especially for individuals with dementia.

Flexible scheduling: You can increase or decrease hours as needs change, without a contract or move.

Lower infection risk: No exposure to communal living spaces where respiratory illnesses and other infections spread quickly.

Hidden Costs of Assisted Living

Level-of-care fees: Most facilities charge extra for assistance with bathing, dressing, medication management, and incontinence care. These fees can add $500–$2,000 per month to the base rate.

Community or entrance fees: Some facilities charge a one-time fee of $1,000–$5,000 upon move-in.

Annual rate increases: Assisted living costs rose 5% year over year in 2025 (CareScout). A $6,200/month facility today could cost $6,500 next year and $6,800 the year after.

Moving and transition costs: Packing, moving, setting up a new apartment, and the emotional toll of leaving a home of 30+ years.

Hidden Benefits of Assisted Living

Built-in socialization: Group meals, activities, outings, and common areas reduce isolation — a major risk factor for depression and cognitive decline in older adults.

24/7 staff availability: No need to worry about a caregiver calling in sick or arriving late. Staff are always on site.

Meals, housekeeping, and maintenance included: These are not trivial expenses. Three meals a day, laundry, cleaning, and home maintenance can easily add $800–$1,500 per month to the cost of living at home.

Safety and security: Emergency call systems, handrails, non-slip flooring, and staff trained in fall response are standard.

State-by-State Cost Variability: Why Location Is a Primary Cost Driver

Home care costs vary by nearly 2x across the United States. This variability directly shifts the crossover point. In a low-cost state, home care remains cheaper than assisted living even at 50+ hours per week. In a high-cost state, the crossover happens much sooner.

Selected state-level median home care rates. Data sources and dates are noted because state-level figures vary between surveys.

State

Median Home Care Rate (per hour)

Source

Mississippi

$25

A Place for Mom (2026)

Louisiana

$23

SeniorLiving.org (2026)

Arkansas

$25–$28

Senioridy (2026)

West Virginia

$25–$28

Senioridy (2026)

Maine

$40–$45

Senioridy (2026)

Washington

$42

SeniorLiving.org (2026)

Minnesota

$38–$42

Senioridy (2026)

South Dakota

$44

A Place for Mom (2026)

North Dakota

$38–$40

Senioridy (2026)

What does this mean for the crossover point? In Mississippi, 44 hours per week of home care costs approximately $4,767 per month ($25 × 44 × 4.33) — well below the national assisted living median of $6,200. In South Dakota, the same 44 hours costs approximately $8,380 per month ($44 × 44 × 4.33) — significantly more than assisted living. The crossover point in South Dakota may occur at 30 hours per week, while in Mississippi it may not occur at all.

To make an informed decision, you need local pricing for both home care and assisted living in your specific area. Our companion guide to assisted living costs by state provides the facility-side data you need to complete the comparison.

How Medicare, Medicaid, and Long-Term Care Insurance Factor In

One of the most common — and costly — misconceptions families bring to this decision is that Medicare will pay for home care. It will not, at least not in the way most people assume.

Medicaid is a different story, but it is state-specific. Through Home and Community-Based Services (HCBS) waivers, many states provide coverage for non-medical in-home care for seniors who meet financial and functional eligibility criteria. The availability, scope, and waiting lists for these waivers vary dramatically by state. Some states also offer Consumer-Directed Attendant Support Services (CDASS), which allow seniors to hire family members as paid caregivers (CareLink).

VA benefits — specifically the Aid and Attendance and Housebound allowances — can provide monthly payments to eligible veterans and their surviving spouses to help cover the cost of home care or assisted living. These are not automatic; they require an application and medical evidence of need.

Long-term care insurance policies vary widely. Some cover home care, some cover only facility care, and some have elimination periods (waiting periods) of 30–90 days before benefits begin. If your parent has a policy, the first step is to read the benefit summary carefully and call the insurer to confirm coverage for non-medical home care.

Medicare: Covers short-term skilled home health only. Does not cover non-medical personal care.

Medicaid (HCBS waivers): Covers in-home care for eligible individuals. State-specific. May have waiting lists.

VA Aid & Attendance: Monthly payment for eligible veterans and surviving spouses. Can be used for home care or assisted living.

Long-term care insurance: Coverage varies by policy. Verify home care coverage, elimination periods, and daily benefit limits.

Out-of-pocket / private pay: The most common funding source for non-medical home care. Some expenses may be tax-deductible if they exceed 7.5% of adjusted gross income (A Place for Mom).

Beyond the Spreadsheet: A 7-Factor Decision Matrix

Cost is the first filter, but it should never be the only filter. The decision between home care and assisted living is deeply personal, and the right choice depends on factors that no spreadsheet can capture. The following matrix covers seven non-cost factors that should weigh heavily in your decision.

A 7-factor decision matrix comparing home care and assisted living on non-cost dimensions. Use this alongside the cost analysis to make a balanced decision.

Seven non-cost factors to consider when choosing between home care and assisted living. Most families will find that some factors favor one option and others favor the other — the goal is to identify which factors matter most.

Factor

Home Care Typically Better When...

Assisted Living Typically Better When...

Safety

The home can be modified affordably; fall risk is low to moderate; 24/7 supervision is not required.

The home has stairs, narrow doorways, or other hazards that are expensive to fix; fall risk is high; wandering is a concern.

Socialization

The senior has a strong local social network (family, friends, church, clubs) and is not isolated.

The senior is lonely at home; family visits are infrequent; structured group activities would improve quality of life.

Medical Complexity

Care needs are stable and can be managed with part-time non-medical care and periodic doctor visits.

Care needs are complex or changing rapidly; multiple chronic conditions require coordinated monitoring; skilled nursing is needed regularly.

Home Suitability

The home is already accessible or can be modified at reasonable cost; the neighborhood is safe and walkable.

The home requires major structural renovations; the neighborhood is isolated or unsafe; the home is too large or too small.

Family Support

Family caregivers live nearby and can provide 10–20+ hours of weekly support; the family is able to coordinate care.

Family caregivers are long-distance, have health issues of their own, or are already experiencing burnout.

Geography

The senior lives in a low-cost state or area where home care rates are below the national median.

The senior lives in a high-cost state where home care rates are $40+/hour; assisted living may be more cost-effective.

Personal Preference

The senior strongly wants to stay home and is willing to accept help from strangers in the home.

The senior is open to moving and may even welcome the social opportunities and reduced burden on family.

For families who are evaluating multiple facility types — independent living, assisted living, memory care, or nursing home — our comprehensive guide to independent living vs. assisted living vs. nursing home provides a detailed comparison of each option's care level, cost structure, and typical resident profile.

Your Next Steps: A Practical Action Plan for Each Scenario

Where you go from here depends on where your family falls on the care spectrum. Below are three common scenarios with specific next steps.

Scenario 1: Your parent needs fewer than 30 hours of paid care per week

Home care is almost certainly the more affordable and appropriate option. Start here:

Get a professional assessment of your parent's ADL and IADL needs from their primary care provider or a geriatric care manager.

Request in-home quotes from three local home care agencies. Ask about their hourly rate, minimum hours per visit, and whether they provide backup coverage.

Check whether your parent qualifies for Medicaid HCBS waivers, VA Aid & Attendance, or any state-specific programs that could offset costs.

Conduct a home safety audit using our room-by-room fall prevention checklists to identify modifications that may be needed.

Scenario 2: Your parent needs 40+ hours of paid care per week

You are in the crossover zone. Both options are financially viable, and the decision should be driven by the non-cost factors in the matrix above.

Get local pricing for both home care and assisted living in your specific area. Use the state-by-state guides linked above as a starting point, then call local providers.

Tour at least three assisted living facilities. Ask about level-of-care fees, annual rate increases, and what is included in the base monthly fee.

Interview home care agencies about their ability to provide consistent, reliable coverage at the hours you need. Ask about caregiver turnover rates and training requirements.

Consult with a financial planner or elder law attorney who specializes in long-term care. They can help you model the 3–5 year cost trajectory of each option, including inflation and potential Medicaid spend-down.

Scenario 3: Your parent needs 24/7 care or has complex medical needs

At this level of need, the home care vs. assisted living comparison expands to include memory care, nursing home care, and live-in caregiver arrangements.

If your parent has a dementia diagnosis, evaluate memory care facilities alongside home care with dementia-trained aides. Memory care costs $6,000–$7,500 per month nationally (Senioridy, 2026).

If your parent needs skilled nursing care, compare the cost of a nursing home ($9,581/month semi-private) with the cost of 24/7 home health care, which can exceed $25,000/month (U.S. News / CareScout).

If you are considering a live-in caregiver, read our detailed comparison of live-in caregiver vs. assisted living costs to understand the trade-offs.

Regardless of the path you choose, get a professional assessment from a geriatric care manager or your parent's primary care provider. The wrong level of care — whether too little or too much — can be costly, unsafe, and emotionally draining for everyone involved.

Comments

Join the discussion with an anonymous comment.