How to Pay for Senior Health Care Services: A Family Guide to Medicare, Medicaid, Private Pay, and Everything in Between

This comprehensive guide helps adult children and spousal caregivers navigate the complex landscape of paying for senior care. It covers the full continuum of services—from hospital stays and skilled nursing to assisted living and nursing homes—explaining what Medicare actually covers, how Medicaid works, and the full range of private pay, insurance, and government benefit options available.

By Editorial Team

Medicare

Medicaid

long-term care insurance

VA benefits

care coordination

📄

A printable version of this guide is available. Use your browser's print function (Ctrl+P / ⌘P) to save or print.

The single most common point of confusion in senior care is payment. Most families do not know that Medicare does not cover long-term care, that Medicaid is state-specific and asset-tested, and that mixing private pay, long-term care insurance, and public programs requires advance planning that most families lack. This guide spans the full continuum of senior health care services — from hospital stays and skilled nursing through assisted living and nursing homes — with detailed cost data, coverage rules, and actionable strategies for every payment source.

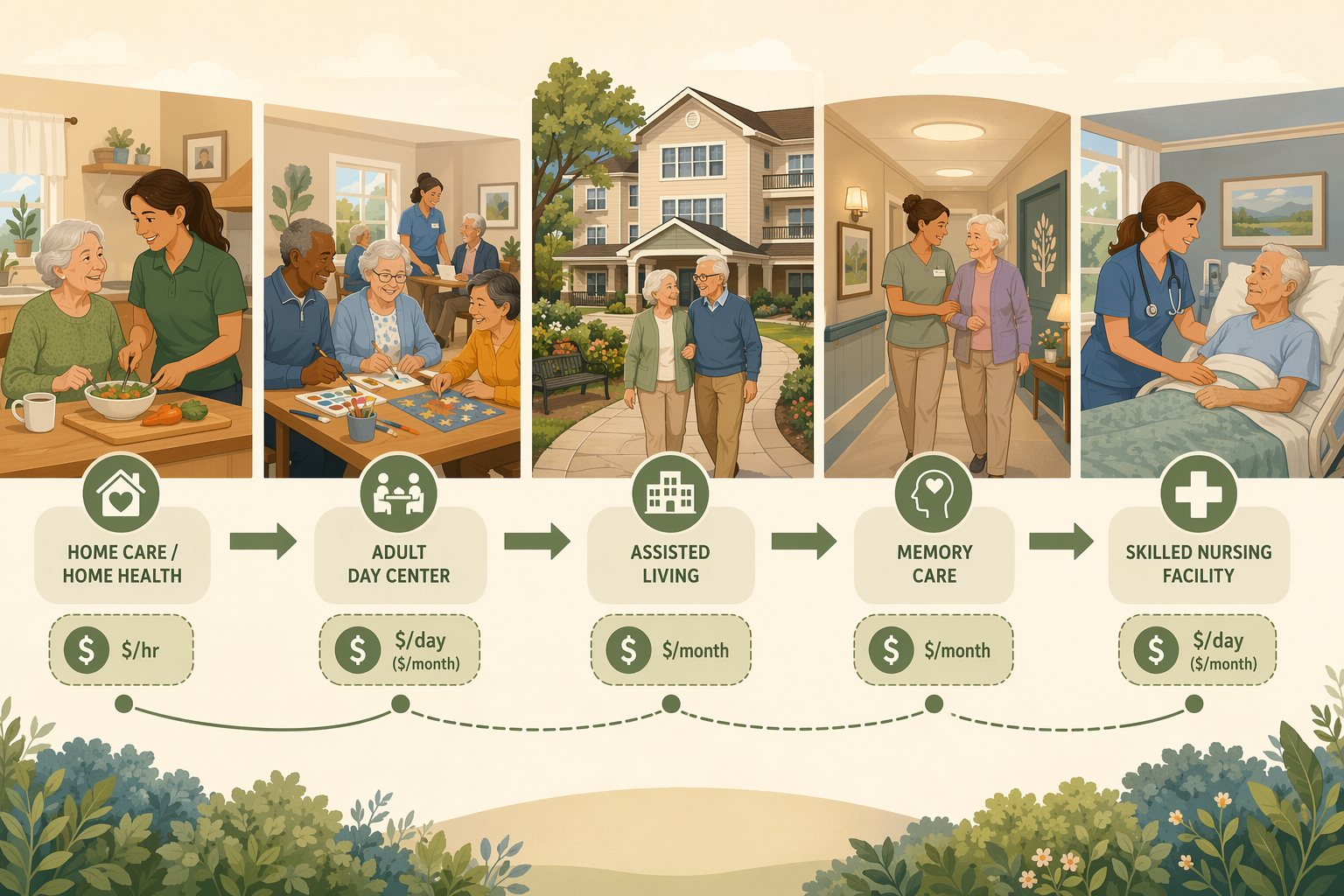

The Senior Health Care Services Continuum: from home care to skilled nursing facility, each level has distinct coverage rules and costs.

The Medicare Myth: What Part A and B Actually Cover (and What They Don't)

Medicare is the foundation of health coverage for Americans 65 and older, but it was never designed to pay for long-term care. The gap between what families expect Medicare to cover and what it actually covers is the single largest source of financial shock in senior care.

Medicare Part A: Hospital and Skilled Nursing Facility Coverage

Part A covers inpatient hospital stays, skilled nursing facility (SNF) care, hospice, and some home health care. For 2026, the Part A deductible is $1,736 per benefit period. After a qualifying hospital stay of at least three days, Medicare will cover up to 100 days in a skilled nursing facility — but with a critical catch:

Days 1–20: $0 copay (after the Part A deductible is met)

Days 21–100: $217 per day copay in 2026

After day 100: Coverage ends entirely. The patient or family is responsible for the full cost.

This 100-day limit applies only to skilled nursing or rehabilitation services — not custodial care. If the patient stops making progress in therapy or no longer requires daily skilled nursing, Medicare may stop coverage well before day 100.

Medicare Part B: Medical Services and Limited Home Health

Part B covers doctor visits, outpatient care, preventive services, and durable medical equipment. It also covers home health services — but only if the patient is homebound, needs skilled care (nursing or therapy), and the care is provided by a Medicare-certified agency. Part B does not cover 24-hour-a-day care at home, personal care (bathing, dressing, toileting) if that is the only care needed, or meal delivery.

What Medicare Does Not Cover: The Full List

Understanding the boundaries of Medicare coverage is essential for financial planning. The table below summarizes what is covered and what is not across the care continuum.

Medicare coverage across the senior care continuum. The gaps are where families must turn to other payment sources.

Service Type

Medicare Coverage

Key Limitations

Hospital stay

Part A covers

Subject to benefit period and deductible ($1,736 in 2026)

Skilled nursing facility (short-term)

Part A covers up to 100 days

Days 21-100: $217/day copay; must follow 3-day hospital stay; must need skilled care

Home health (skilled)

Part A and B cover

Must be homebound, need skilled care, from a Medicare-certified agency; limited to part-time or intermittent care

Hospice care

Part A covers

For terminal illness with prognosis of 6 months or less

Custodial care (bathing, dressing, eating)

Not covered

This is the most common gap families face

Assisted living

Not covered

Room, board, and personal care services are entirely out-of-pocket

Long-term nursing home stay

Not covered

Medicare pays only for short-term skilled stays, not long-term custodial care

Adult day care

Not covered

Medicare does not pay for adult day services

Dental, vision, hearing

Not covered by original Medicare

Some Medicare Advantage plans may offer limited coverage

Medicare covers hospital stays, short-term skilled nursing, and limited home health — but not custodial care, assisted living, or long-term nursing home stays.

Medicare Savings Programs and Extra Help: Reducing Out-of-Pocket Costs for Low-Income Seniors

For seniors with limited income and assets, Medicare Savings Programs (MSPs) and Extra Help can significantly reduce out-of-pocket costs. These programs are administered by state Medicaid agencies and help with Medicare premiums, deductibles, coinsurance, and prescription drug costs.

Medicare Savings Programs (MSPs)

There are three main types of MSPs, each with different income and asset limits:

Qualified Medicare Beneficiary (QMB) Program: Helps pay for Part A and Part B premiums, deductibles, coinsurance, and copays. This is the most comprehensive MSP.

Specified Low-Income Medicare Beneficiary (SLMB) Program: Helps pay for Part B premiums only.

Qualifying Individual (QI) Program: Helps pay for Part B premiums for individuals who do not qualify for QMB or SLMB. Funding is limited and awarded on a first-come, first-served basis.

Extra Help (Part D Low-Income Subsidy)

Extra Help is a federal program that helps pay for Medicare Part D prescription drug plan costs, including premiums, deductibles, and copays. Eligibility is based on income and resources. For 2026, individuals with income up to 150% of the federal poverty level and resources below a certain threshold may qualify. The program can save beneficiaries hundreds or even thousands of dollars per year on prescription drugs.

Medicaid: The Payer of Last Resort for Long-Term Care

Medicaid is a joint federal and state program that provides health coverage for low-income individuals, including seniors. It is the primary payer for long-term nursing home care in the United States, covering an average of 82 cents per dollar spent on nursing home care nationally. Approximately 7.2 million low-income seniors rely on Medicaid alongside Medicare.

State-Specific Eligibility and Asset Limits

Medicaid eligibility varies significantly by state. In general, to qualify for long-term care Medicaid, an individual must have limited income and assets. Asset limits typically range from $2,000 to $10,000 for an individual, though some states have higher limits. The home is often exempt up to a certain equity value, and a vehicle is usually exempt. Income limits also vary, but many states use a "medically needy" pathway that allows individuals with higher incomes to qualify by spending down excess income on medical expenses.

Home and Community-Based Services (HCBS) Waivers

Many states offer HCBS waivers that allow Medicaid funds to be used for home and community-based services rather than institutional care. These waivers can cover personal care, homemaker services, respite care, adult day care, home modifications, and assistive technology. The goal is to help seniors remain in their homes and communities rather than entering a nursing home. However, HCBS waivers often have waiting lists, and availability varies by state.

Spend-Down Strategies

For individuals whose income or assets exceed Medicaid limits, spend-down strategies can help them qualify. Common strategies include:

Paying for medical expenses out-of-pocket to reduce countable assets

Paying for home modifications or assistive devices

Prepaying funeral and burial expenses

Purchasing an annuity that meets Medicaid requirements (shielded from asset calculations)

Transferring assets to a spouse (the community spouse is allowed to retain a certain amount of assets and income)

Private Pay: Understanding the True Cost of Care Across the Continuum

For families who do not qualify for Medicaid or who need care before Medicaid eligibility is established, private pay is the default option. Understanding the true cost of care across the continuum is essential for financial planning. The following data is based on 2026 reports from A Place for Mom and SeniorLiving.org, which are referral-fee-based platforms — not government surveys. Cross-verification with Genworth/CareScout data is recommended for the most accurate national medians.

National Median Costs by Care Type (2026)

2026 national median costs for senior care services. Actual costs vary significantly by state and level of care needed.

Care Type

National Median Cost

Typical Range

Home care (nonmedical, hourly)

$34/hour

$25–$44/hour by state

Home care (44 hours/week)

~$6,478/month

Varies by state and hours needed

Assisted living (monthly)

$6,313/month

$3,000–$10,000+ depending on location and amenities

Nursing home (semiprivate room)

$9,842/month ($328/day)

$5,808–$32,220/month by state

Nursing home (private room)

$11,294/month ($376/day)

$7,519–$32,220/month by state

State-by-State Variation

Costs vary dramatically by state. For home care, the most expensive states in 2026 include South Dakota ($44/hour), Vermont ($43/hour), Minnesota ($42/hour), Montana ($42/hour), and Washington ($42/hour). The least expensive states include Mississippi ($25/hour), Alabama ($26/hour), Louisiana ($26/hour), and West Virginia ($28.50/hour). For nursing homes, the range is even wider: semiprivate rooms range from $5,808/month in Texas to $32,220/month in Alaska.

The Cross-Over Point: When Full-Time Home Care Becomes Comparable to Assisted Living

One of the most important financial calculations families need to make is the cross-over point where full-time home care becomes comparable in cost to assisted living. At the national median of $34/hour, 44 hours per week of home care costs approximately $6,478/month — nearly identical to the $6,313/month median cost of assisted living. In states with higher home care rates, assisted living may actually be the more affordable option.

Long-Term Care Insurance: What It Covers and When It Makes Sense

Long-term care (LTC) insurance is designed to cover the costs of custodial care that Medicare does not pay for. Policies can cover home care, assisted living, adult day care, and nursing home care. However, LTC insurance is not right for everyone, and the decision to purchase it depends on age, health, and financial circumstances.

What LTC Insurance Typically Covers

Home care: Personal care assistance with ADLs, homemaker services, and respite care

Assisted living: Room, board, and personal care services in an assisted living facility

Nursing home care: Both skilled and custodial care in a nursing home

Adult day care: Structured daytime programs for seniors who need supervision

Hospice care: End-of-life care, often with a daily or monthly benefit

When LTC Insurance Makes Sense

LTC insurance is most appropriate for individuals who:

Are in their 50s or early 60s (premiums increase significantly with age)

Have sufficient assets to protect (typically $150,000 or more, excluding a home)

Can afford the premiums without financial strain (premiums can be $2,000–$5,000+ per year depending on age and benefit level)

Are in good health (policies are medically underwritten; pre-existing conditions may result in denial or higher premiums)

Want to avoid spending down assets to qualify for Medicaid

Key Considerations and Trade-Offs

Premiums can increase over time: Many policies have rate increase provisions, and premiums have been rising faster than inflation in recent years.

Exclusions and waiting periods: Most policies have a 90-day elimination period (waiting period) before benefits begin, and pre-existing condition exclusions may apply.

Benefit limits: Policies typically have a daily or monthly maximum benefit and a total lifetime benefit cap (e.g., $200,000 total).

Inflation protection: Adding inflation protection increases premiums but helps ensure benefits keep pace with rising care costs.

Not everyone qualifies: Individuals with significant health conditions may be denied coverage or offered policies with limited benefits.

VA Benefits: Support for Veterans and Surviving Spouses

The Department of Veterans Affairs (VA) offers a range of benefits for eligible veterans and surviving spouses that can significantly offset the cost of senior care. These benefits include health care, long-term care, pensions, and disability compensation.

VA Health Care and Long-Term Care

The VA provides comprehensive health care services to enrolled veterans, including primary care, specialty care, mental health services, and prescription drugs. For long-term care, the VA offers:

VA nursing homes (Community Living Centers): The VA operates its own nursing homes for eligible veterans.

State Veterans Homes: State-run facilities that partner with the VA to provide nursing home and domiciliary care.

Community Nursing Home Program: The VA contracts with community nursing homes to provide care for eligible veterans.

Home and Community-Based Services: The VA offers home health aide services, respite care, adult day health care, and homemaker services through programs like the Veterans Directed Care program.

VA Pensions and Disability Compensation

The VA offers a pension for low-income veterans who are 65 or older or who are permanently and totally disabled. The pension can be supplemented by the Aid and Attendance benefit, which provides additional funds for veterans who need help with ADLs, are housebound, or are in a nursing home. Surviving spouses may also be eligible for a pension and Aid and Attendance.

How to Apply

To apply for VA benefits, start by gathering the veteran's DD Form 214 (Certificate of Release or Discharge from Active Duty). Then:

Apply for VA health care online through the VA website, by phone at 877-222-8387, or in person at a VA medical center.

Apply for a VA pension and Aid and Attendance by submitting VA Form 21P-527EZ (for veterans) or VA Form 21P-534EZ (for surviving spouses).

Contact your local VA regional office or a Veterans Service Officer (VSO) for assistance with the application process.

Bridge Strategies: Reverse Mortgages, Annuities, and Life Insurance Conversion

For families who need to bridge the gap between savings and care costs, several financial strategies can help generate additional funds. These strategies come with risks and should be carefully evaluated with the help of a financial advisor or elder law attorney.

Reverse Mortgages

A reverse mortgage allows homeowners aged 62 or older to convert a portion of their home equity into cash without selling the home or making monthly mortgage payments. The loan is repaid when the homeowner sells the home, moves out permanently, or passes away. Proceeds can be used for any purpose, including paying for senior care.

How it works: The lender makes payments to the homeowner (as a lump sum, monthly payments, or a line of credit). Interest accrues on the loan balance.

Pros: Provides tax-free cash without selling the home; no monthly mortgage payments; can be used to pay for home care, assisted living, or other expenses.

Cons: Reduces home equity; fees and interest can be high; the loan must be repaid when the homeowner leaves the home; can affect Medicaid eligibility if not structured properly.

Annuities

An annuity is a financial product that provides a guaranteed stream of income for a specified period or for life. Certain types of annuities can be structured to be shielded from Medicaid asset considerations, making them a useful tool for Medicaid planning. However, annuities are complex products with fees, surrender charges, and tax implications.

Medicaid-compliant annuities: These are structured to meet state Medicaid requirements, allowing the income to be used for care costs while the principal is shielded from asset calculations.

Immediate annuities: Convert a lump sum into a guaranteed income stream that starts immediately. Can be used to pay for ongoing care costs.

Deferred annuities: Accumulate value over time and begin paying out at a future date. Less useful for immediate care needs.

Life Insurance Conversion

Life insurance policies can be converted into cash to pay for senior care through several mechanisms:

Surrender: Cash in the policy for its cash surrender value. This is the simplest option but may result in losing the death benefit.

Life settlement: Sell the policy to a third party for a lump sum payment, typically 50–75% of the policy's face value. The buyer takes over premium payments and receives the death benefit when the insured passes away.

Conversion to life assurance: Some policies can be converted into a long-term care benefit plan, allowing the death benefit to be used for care costs while the insured is still alive.

Tax Deductions for Medical Expenses: Reducing the Financial Burden

Out-of-pocket medical expenses that exceed 7.5% of your Adjusted Gross Income (AGI) can be deducted as itemized medical expenses on your federal income tax return. This can provide significant tax savings for families paying for senior care.

What Qualifies as a Deductible Medical Expense

The IRS allows deductions for a wide range of medical expenses, including many senior care costs:

Nursing home costs: The full cost of a nursing home (including room and board) is deductible if the primary reason for being there is medical care.

Home care costs: Payments for home health aides, personal care attendants, and homemaker services are deductible if the care is medically necessary.

Assisted living costs: A portion of assisted living costs may be deductible if the facility provides medical or nursing care. The deductible portion typically includes the cost of care services but not room and board.

Medically necessary ADL help: Help with activities of daily living (bathing, dressing, eating, toileting, transferring) is deductible if it is prescribed by a doctor as medically necessary.

Long-term care insurance premiums: Premiums for qualified long-term care insurance policies are deductible as medical expenses, subject to age-based limits.

Other deductible expenses: Prescription drugs, doctor visits, hospital stays, dental care, vision care, hearing aids, transportation for medical care, and home modifications (if medically necessary).

How to Document Expenses

To claim the medical expense deduction, you must itemize your deductions on Schedule A of Form 1040. You will need to keep detailed records of all medical expenses, including:

Receipts and invoices from care providers

A doctor's prescription or letter of medical necessity for home care or ADL help

A log of mileage for medical-related travel

Statements from insurance companies showing what was paid and what was not

A breakdown of assisted living or nursing home costs showing the portion attributable to medical care vs. room and board

Four payment source categories for senior care. Most families will need to combine multiple sources to cover the full cost of care.

Putting It All Together: Building a Payment Plan

Paying for senior care rarely relies on a single source. Most families combine private pay, Medicare, Medicaid, LTC insurance, VA benefits, and bridge strategies to cover the full cost. The key is to start planning early, understand the rules of each payment source, and seek professional guidance from elder law attorneys, financial advisors, and geriatric care managers.

For additional help navigating the payment landscape, contact the Eldercare Locator at 800-677-1116, visit LongTermCare.gov, or use the BenefitsCheckUp.org tool from the National Council on Aging (NCOA) to identify benefits your family member may qualify for.

Comments

Join the discussion with an anonymous comment.