Home Health vs. Home Care vs. Hospice vs. Respite: A Side-by-Side Comparison for Families After Hospital Discharge

clinicalIf your parent was just discharged from the hospital and you're confused by terms like 'home health,' 'home care,' 'hospice,' and 'respite,' this guide explains exactly what each service does, how Medicare pays, and which one fits your situation — so you can avoid costly mistakes and get the right care immediately.

Why the Terminology Matters: Ordering the Wrong Service Can Delay Care or Create Surprise Bills

Your father is sitting in a hospital bed, dressed in his own clothes, waiting for the discharge papers. The nurse says, "We'll set you up with home health." The social worker hands you a list of home care agencies. A friend mentions hospice. Another friend says you need respite. Each person uses a different term, and they all sound like they mean the same thing — someone coming to the house to help. They do not.

The difference between these services is not semantic. It determines whether Medicare pays the bill or you pay out of pocket. It determines whether a registered nurse or a personal care aide shows up at the door. It determines whether your parent receives skilled wound care or help with bathing — and whether that help is covered at all. Ordering the wrong service can delay critical care by days, trigger a denied Medicare claim, or leave you with a bill you did not expect.

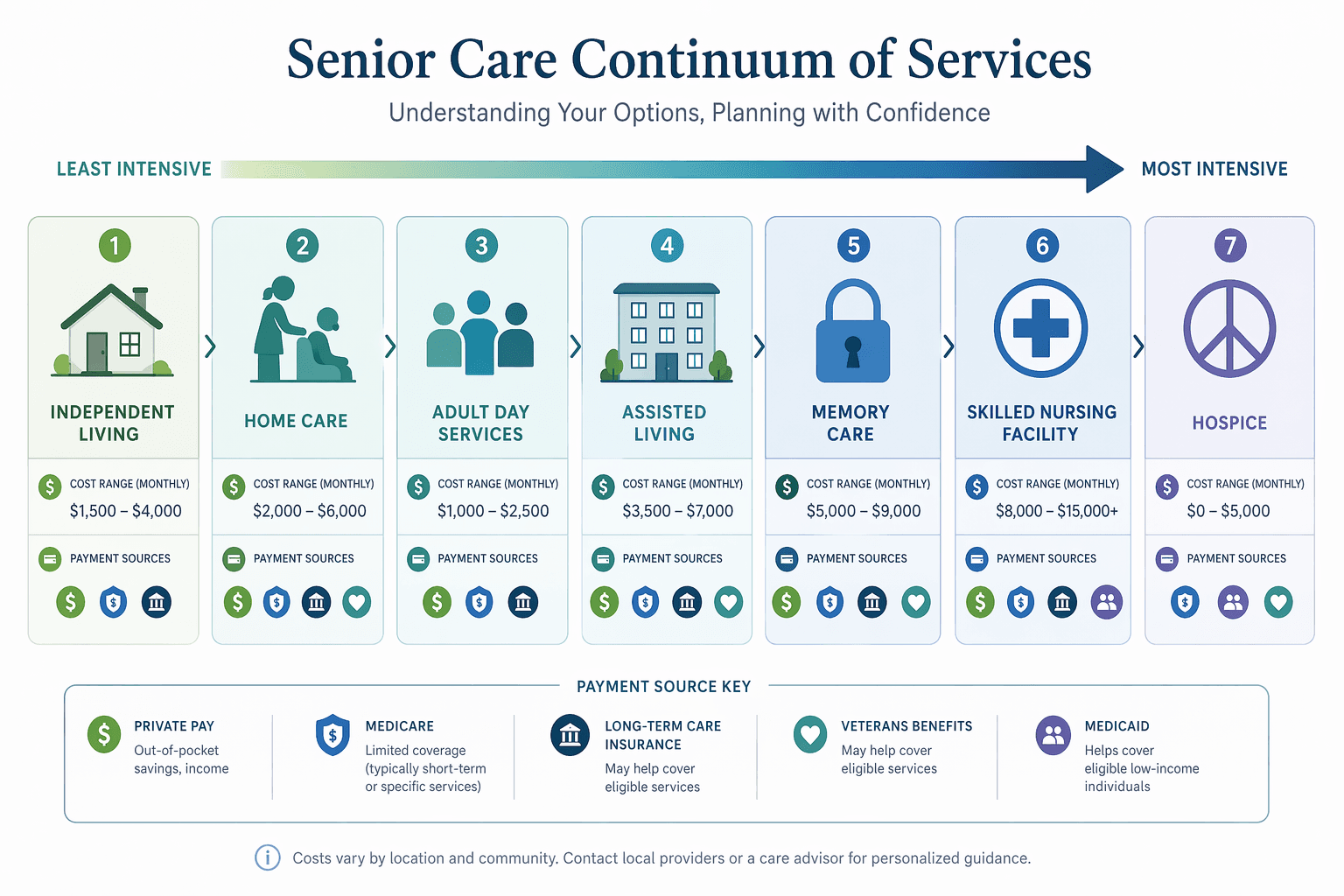

This guide covers the five service types you are most likely to encounter in a discharge conversation: home health (skilled, Medicare-covered), home care (non-medical, private pay), hospice (end-of-life comfort, Medicare-covered), respite (temporary caregiver relief, varied coverage), and palliative care (comfort alongside curative treatment). Each has a distinct purpose, a distinct provider type, and a distinct payment model. The comparison table below lays them side by side so you can match the right service to your parent's actual situation.

The Five Service Types at a Glance: What Each Does, Who Provides It, and How Medicare Pays

The table below is your primary reference tool. Print it, take it to the hospital, and use it during the discharge planning meeting. Each row answers the three questions that matter most: What does this service actually do? Who provides it? And who pays?

| Service Type | Purpose | Who Provides It | Typical Services | Medicare Coverage | Key Limitation |

|---|---|---|---|---|---|

| Home Health | Recover from illness, injury, or surgery at home with skilled medical care | Medicare-certified home health agency (RNs, PTs, OTs, social workers) | Skilled nursing, physical therapy, occupational therapy, speech therapy, medical social work, part-time home health aide (when combined with skilled care) | Covered at no cost for eligible patients (Part A and/or Part B); patient pays 20% of Medicare-approved amount for DME | Does NOT cover 24/7 care, custodial care alone, or homemaker services; patient must be homebound and need skilled care part-time/intermittently |

| Home Care (Non-Medical) | Help with activities of daily living (bathing, dressing, meal prep, light housekeeping) | Private home care agencies or independent caregivers (personal care aides, homemakers) | Bathing, dressing, grooming, toileting, meal preparation, medication reminders, companionship, transportation | Medicare does NOT cover; almost always private pay (some Medicaid HCBS waivers may cover in certain states) | No Medicare coverage; costs can exceed $80,000/year at 44 hours/week; no skilled medical care provided |

| Hospice | Comfort-focused end-of-life care for patients with a prognosis of 6 months or less | Medicare-certified hospice agency (RNs, social workers, chaplains, volunteers, aides) | Pain and symptom management, nursing care, medical equipment, medications, short-term inpatient care, grief counseling, caregiver support | Fully covered by Medicare Part A (hospice benefit) with little to no out-of-pocket costs | Patient must have a terminal prognosis of 6 months or less and choose comfort care over curative treatment |

| Respite | Temporary relief for family caregivers | Home care agencies, adult day centers, skilled nursing facilities, hospice agencies | Short-term care at home, in an adult day center, or in a facility (hospital or SNF) for a few hours to several days | Medicare covers up to 5 consecutive days of inpatient respite under the hospice benefit; otherwise, typically private pay | Medicare-covered respite is only available to patients enrolled in hospice; non-hospice respite is almost always out-of-pocket |

| Palliative Care | Symptom relief and improved quality of life alongside curative treatment | Specialized palliative care teams (doctors, nurses, social workers) — often hospital-based or clinic-based | Pain management, symptom control, care coordination, advance care planning, emotional and spiritual support | Covered by Medicare Part B (outpatient) or Part A (inpatient) depending on setting; patient may have copays | Not a home-based service in most cases; often requires a hospital or clinic visit; does not replace home health or home care |

The most common mistake families make is assuming that home health and home care are the same thing. They are not. Home health is a skilled medical service ordered by a physician, provided by a Medicare-certified agency, and covered by Medicare for eligible patients. Home care is a non-medical service — help with bathing, dressing, meals — that is almost always paid entirely out of pocket. If your parent needs help with daily activities but does not need skilled nursing or therapy, Medicare will not pay for that help unless it is part of a prescribed home health plan that also includes skilled care.

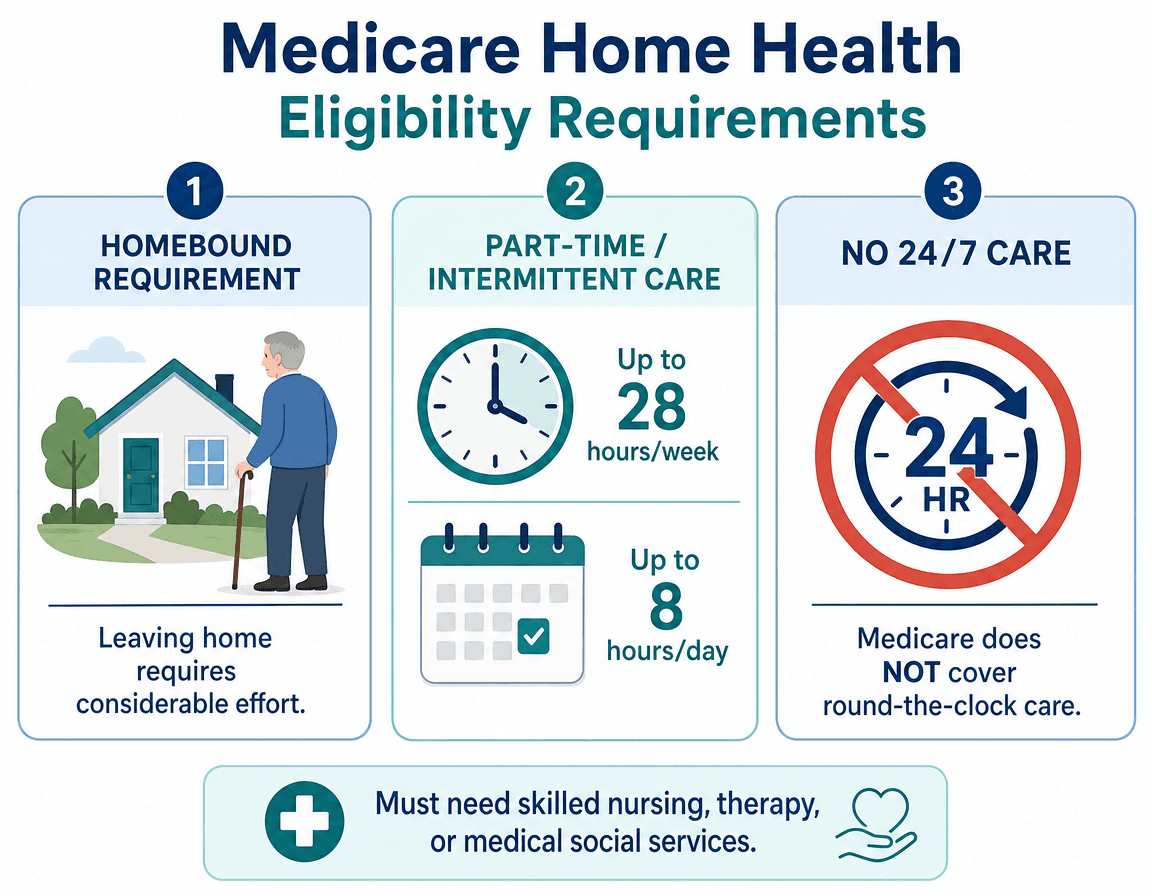

Medicare Home Health Eligibility: The Homebound Requirement, Part-Time Rule, and the 24/7 Care Gap

Medicare home health is a generous benefit — but only if you meet its specific eligibility criteria. Three rules cause the most confusion and the most denied claims.

1. The Homebound Requirement

To qualify for Medicare-covered home health, your parent must be homebound. This does not mean they cannot leave the house at all. Medicare defines homebound as: leaving home requires considerable and taxing effort, and the patient cannot leave without help (from another person or a device like a walker or wheelchair). Occasional absences for medical treatment or infrequent, short trips (like a religious service or a haircut) do not disqualify someone. But the expectation is that the patient's condition makes leaving home a significant challenge.

2. The Part-Time / Intermittent Rule

Medicare home health is designed for short-term, part-time care, not ongoing daily assistance. The rules are specific: Medicare covers up to 8 hours per day (combining skilled nursing and home health aide time) and a maximum of 28 hours per week. In certain cases where more care is medically necessary for a short period, Medicare may cover up to 35 hours per week. Once the patient no longer needs skilled care (nursing or therapy), the home health benefit ends — even if they still need help with bathing or dressing.

This is the rule that catches most families off guard. Your parent may receive a home health aide for bathing assistance — but only as long as they are also receiving skilled nursing or therapy. The moment the skilled care ends, the aide visits stop, even if your parent still cannot bathe safely alone.

3. The 24/7 Care Gap

Medicare home health does not cover 24-hour-a-day care. If your parent needs round-the-clock supervision or assistance — because of dementia, fall risk, or general frailty — Medicare will not pay for that level of support through the home health benefit. This is the single most important limitation to understand before you leave the hospital. If your parent needs 24/7 care, you will need to combine Medicare home health (for the skilled portion) with private-pay home care (for the custodial portion), or consider a facility setting.

For a deeper dive into 2026-specific Medicare changes affecting home health, including the new Part B premium of $202.90/month and the Part A inpatient deductible of $1,736, see our dedicated guide: Medicare Home Health Care in 2026: What Changed, What Stayed the Same, and What Families Need to Know. For a complete breakdown of eligibility criteria, costs, and coverage gaps, see Does Medicare Cover Home Health Care? A Caregiver's Guide to Eligibility, Costs, and Coverage Gaps in 2026.

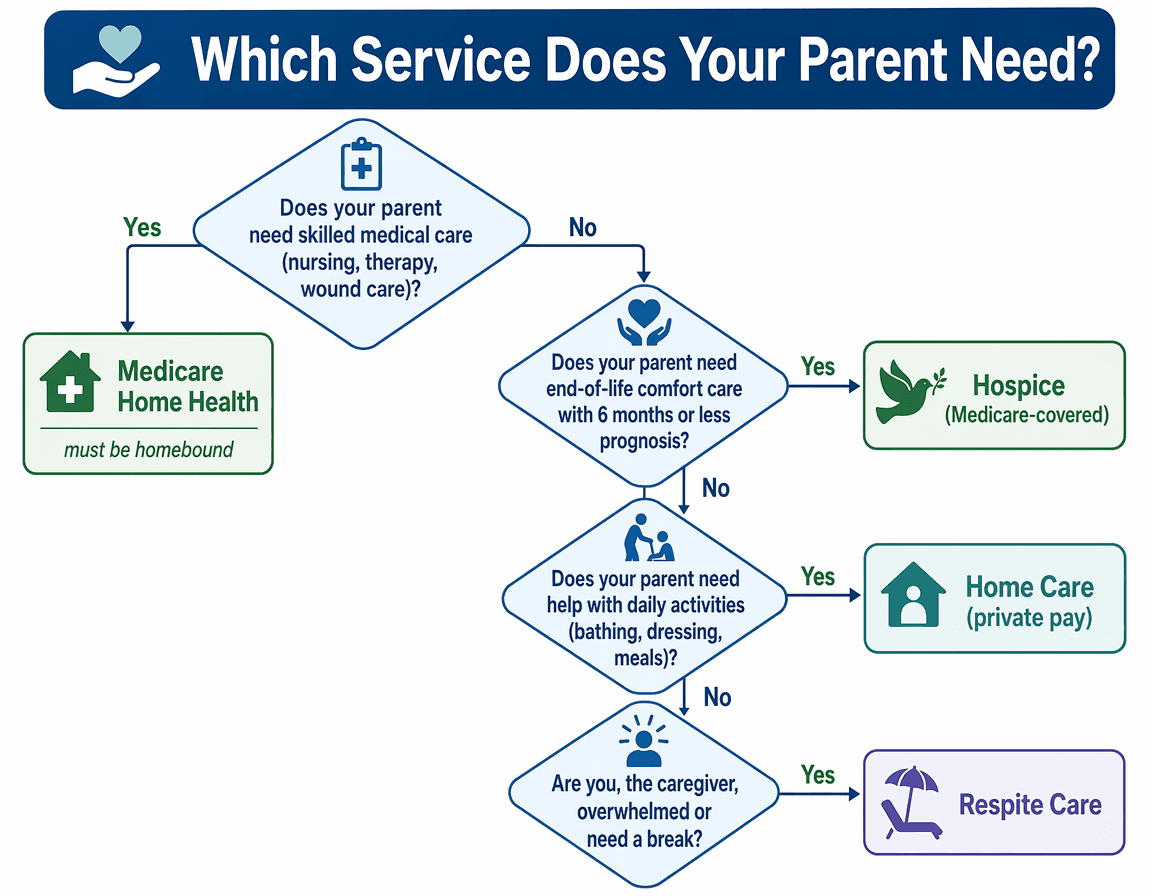

When to Call Each Service: Decision Trees Based on Your Parent's Situation

Use the following decision framework at the hospital bedside. Start at the top and answer each question honestly. The path that emerges will tell you which service to request from the discharge planner.

Does your parent need skilled nursing or therapy?

Skilled care includes: wound care, injections, IV medications, physical therapy after a hip replacement, occupational therapy after a stroke, speech therapy after a neurological event. If the answer is yes, and your parent is homebound, request Medicare home health. The hospital discharge planner should arrange a referral to a Medicare-certified home health agency. If your parent does not meet the homebound requirement, home health is not an option — you will need to arrange outpatient therapy or private-duty skilled nursing.

Is your parent's prognosis 6 months or less?

If a physician has determined that your parent has a terminal illness with a life expectancy of 6 months or less, and your parent chooses comfort-focused care over curative treatment, request hospice. Hospice is fully covered by Medicare Part A and includes nursing care, medical equipment, medications related to the terminal diagnosis, and — critically — caregiver support and respite. Many families wait too long to enroll in hospice, missing months of covered support.

Does your parent need help with bathing, dressing, meals, or other daily activities — but not skilled care?

If your parent is medically stable and does not need nursing or therapy, but cannot safely bathe, dress, prepare meals, or manage medications alone, you need home care (non-medical). This is almost always private pay. Medicare will not cover it unless it is part of a home health plan that also includes skilled care. If your parent qualifies for Medicaid, a Home and Community-Based Services (HCBS) waiver may cover some in-home care costs — but eligibility and coverage vary significantly by state.

Do you, as the caregiver, need a break?

If you are the primary caregiver and you are exhausted, overwhelmed, or need to attend to your own health or family obligations, request respite care. If your parent is enrolled in hospice, Medicare covers up to 5 consecutive days of inpatient respite in a hospital or skilled nursing facility. If your parent is not in hospice, respite is typically private pay — you can hire a home care agency for a few hours or days, or use an adult day center (average $95 per 8-hour day).

2026 Cost Ranges: What You'll Actually Pay for Each Service

Cost is often the deciding factor. The table below shows what you can expect to pay in 2026 for each service type. The most important takeaway: staying at home with paid care is often the most expensive option — not the cheapest, as many families assume.

| Service Type | 2026 Cost Range | Primary Payment Source | Key Insight |

|---|---|---|---|

| Home Health (Skilled) | $0 for covered services (patient pays 20% of Medicare-approved amount for DME) | Medicare Part A and/or Part B | No cost for eligible patients, but limited to skilled care and part-time hours (max 28–35 hrs/week); does not cover custodial care alone |

| Home Care (Non-Medical) | National median $34–$35/hour (CareScout 2025 survey: $35/hr; A Place for Mom June 2026: $34/hr); $80,080/year at 44 hours/week | Almost always private pay (some Medicaid HCBS waivers may cover in certain states) | Staying home with paid care is the most expensive option — $80,080/year exceeds assisted living at $74,400/year and approaches nursing home costs |

| Hospice | Fully covered by Medicare Part A with little to no out-of-pocket costs | Medicare Part A (hospice benefit) | Includes nursing, equipment, medications, and up to 5 days of inpatient respite — a comprehensive benefit families often underuse |

| Respite (Inpatient Facility) | $150–$425/day (facility-based); Medicare covers up to 5 consecutive days under hospice benefit | Medicare (hospice patients only) or private pay | Non-hospice respite is almost always out-of-pocket; adult day centers offer a lower-cost alternative at $95/day for 8 hours |

| Palliative Care | Covered by Medicare Part B (outpatient) or Part A (inpatient) depending on setting; patient may have copays | Medicare Part B or Part A | Not a home-based service in most cases; often requires clinic or hospital visits; does not replace home health or home care |

For a broader guide on all payment sources beyond Medicare — including Medicaid, VA benefits, and long-term care insurance — see How to Pay for Senior Care in 2026: A Guide to Medicare, Medicaid, and Other Funding Sources.

Questions to Ask the Hospital Discharge Planner and Home Health Agency Before Signing Anything

Before you leave the hospital, you need answers to specific questions. Use this checklist during the discharge planning meeting. Write down the answers and the name of the person who gave them.

- "Is this agency Medicare-certified?" — Only Medicare-certified agencies can bill Medicare for home health services. If the agency is not certified, Medicare will not pay.

- "Does my parent meet the homebound requirement as Medicare defines it?" — Ask the discharge planner to document this in the medical record. If the answer is no, home health is not an option.

- "What specific skilled services will be provided, and by whom?" — You need to know whether a registered nurse, a physical therapist, or a home health aide will visit, and how often.

- "How many hours per week of home health aide time is included?" — Remember: aide time is only covered when combined with skilled care. If the plan includes 2 hours of aide time per week, that may not be enough for your parent's needs.

- "Who pays for what?" — Get a written breakdown of what Medicare covers, what you will pay out of pocket, and what the agency will bill you for directly.

- "What happens when the skilled care ends?" — The home health benefit ends when skilled nursing or therapy is no longer needed. Ask what the transition plan is — will the agency help you arrange private-pay home care?

- "Is my parent eligible for hospice or palliative care?" — If the prognosis is serious, ask this question directly. Many families are not offered hospice because the physician assumes they want curative treatment.

- "What respite options are available if I need a break?" — If your parent is not in hospice, ask about adult day centers or short-term home care as a private-pay respite option.

Once you have chosen a service and need practical steps for arranging in-home nursing care, see our step-by-step guide: How to Set Up In-Home Nursing Care for an Elderly Parent: A Step-by-Step Decision Guide.

See This Term in Context

- POA, CAPS, and PERS: A Caregiver's Cheat Sheet for the Three Acronyms That Determine Where Your Parent Lives, Who Makes Medical Decisions, and How They Stay Safe

After a parent's fall or hospital discharge, three acronyms — POA (legal authority), CAPS (home modification expertise), and PERS (emergency monitoring) — represent the sequential decisions caregivers must make. This guide frames them as an integrated decision pathway, not a flat glossary.

- Hospice vs. Palliative Care: A Family Caregiver’s Decision Framework

Understand the critical difference between hospice and palliative care — when each starts, what changes for your family, and how to recognize the right time to transition. This guide helps adult children caring for a seriously ill parent make informed, timely decisions.

- Senior Health Services vs. Home Care vs. Home Health vs. Hospice: What's the Difference and How to Choose

This guide helps family caregivers distinguish between commonly confused senior care terms — home care, home health, palliative care, hospice, assisted living, and skilled nursing — and provides a decision framework for choosing the right service at the right time.

Also related: Medicare Home Health Care in 2026: What Changed, What Stayed the Same, and What Families Need to Know, Does Medicare Cover Home Health Care? A Caregiver's Guide to Eligibility, Costs, and Coverage Gaps in 2026, How to Set Up In-Home Nursing Care for an Elderly Parent: A Step-by-Step Decision Guide, How to Pay for Senior Care in 2026: A Guide to Medicare, Medicaid, and Other Funding Sources

Comments

Join the discussion with an anonymous comment.