The Financial Survival Guide for Family Caregivers: Programs, Tax Credits, and Strategies to Offset the Cost of Caring

Family caregivers spend an average of $7,200 out-of-pocket each year and lose $21,500 in income, yet most are unaware of the Medicaid, VA, paid leave, and tax credit programs designed to offset these costs. This guide uses a decision-tree approach to help adult children, sandwich-generation, and long-distance caregivers navigate the concrete financial pathways they may qualify for.

- Last Reviewed

- 2026-06-23

- working caregiver

- caregiver stress

- caregiver burnout

- Medicaid self-directed care

- VA caregiver compensation

The number is $28,700 a year — if you're an average family caregiver. But averages lie. They hide the caregiver earning $24,999 or less, which is nearly one in five. The real number for that person isn't an average; it's a crisis.

Let that land before we talk about solutions. The first problem isn't that programs don't exist — it's that the cost is so high and so invisible that most caregivers never get past the shock.

What $28,700 Actually Means

Start with the macro: AARP pegs the economic value of unpaid family caregiving at $1.01 trillion in 2024 — larger than most countries' GDP. Yet the 53 million family caregivers who produce that value are individually paying for the privilege. The National Council on Aging reports average out-of-pocket costs of $7,200 per year. A Place for Mom calculates $21,500 in average annual lost income. But those are means, not medians. A low-income caregiver faces a far worse financial picture than the averages suggest — and the averages already run deep red.

The middle-aged daughter caring for her mother can lose $80,000 to $100,000 per year in lifetime wages, benefits, and career advancement, according to Penn LDI. The sandwich-generation caregiver — 48% of all caregivers — balances this against raising kids under 18.

Why You Probably Missed the Money

Here's what's frustrating: programs exist that can offset those costs. Medicaid self-directed care, VA caregiver compensation, state paid family leave, tax credits. They exist. But most caregivers never use them because awareness is shockingly low and eligibility is a maze. Only 3% of adults over 50 have long-term care insurance. Private solutions are rare. Public programs are fragmented across state lines, income thresholds, and functional need requirements.

This article is a decision tree. It starts with your constraints — where you live, who you care for, their income, your job — and maps you to the programs you should actually investigate. Not a list of possibilities. A path.

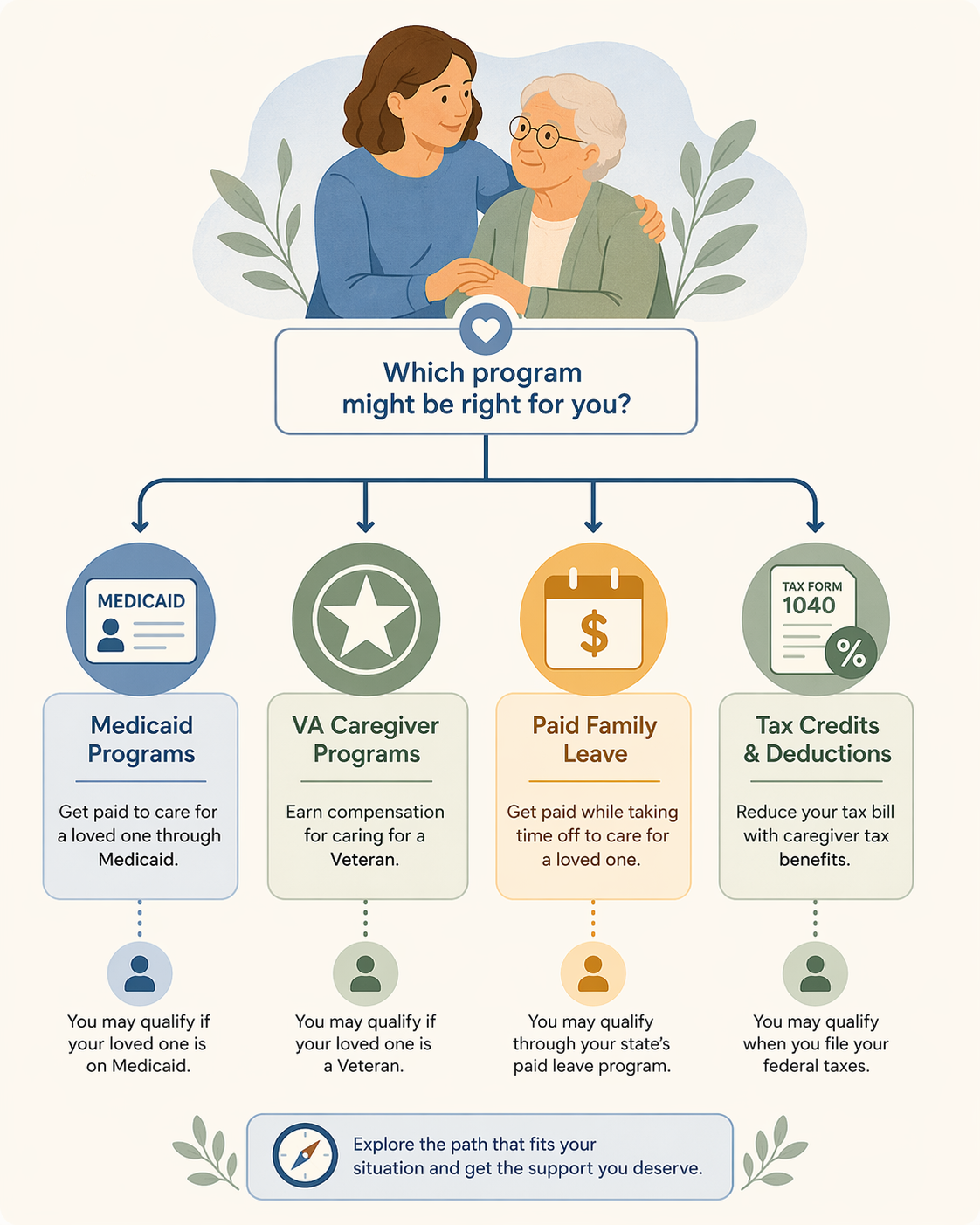

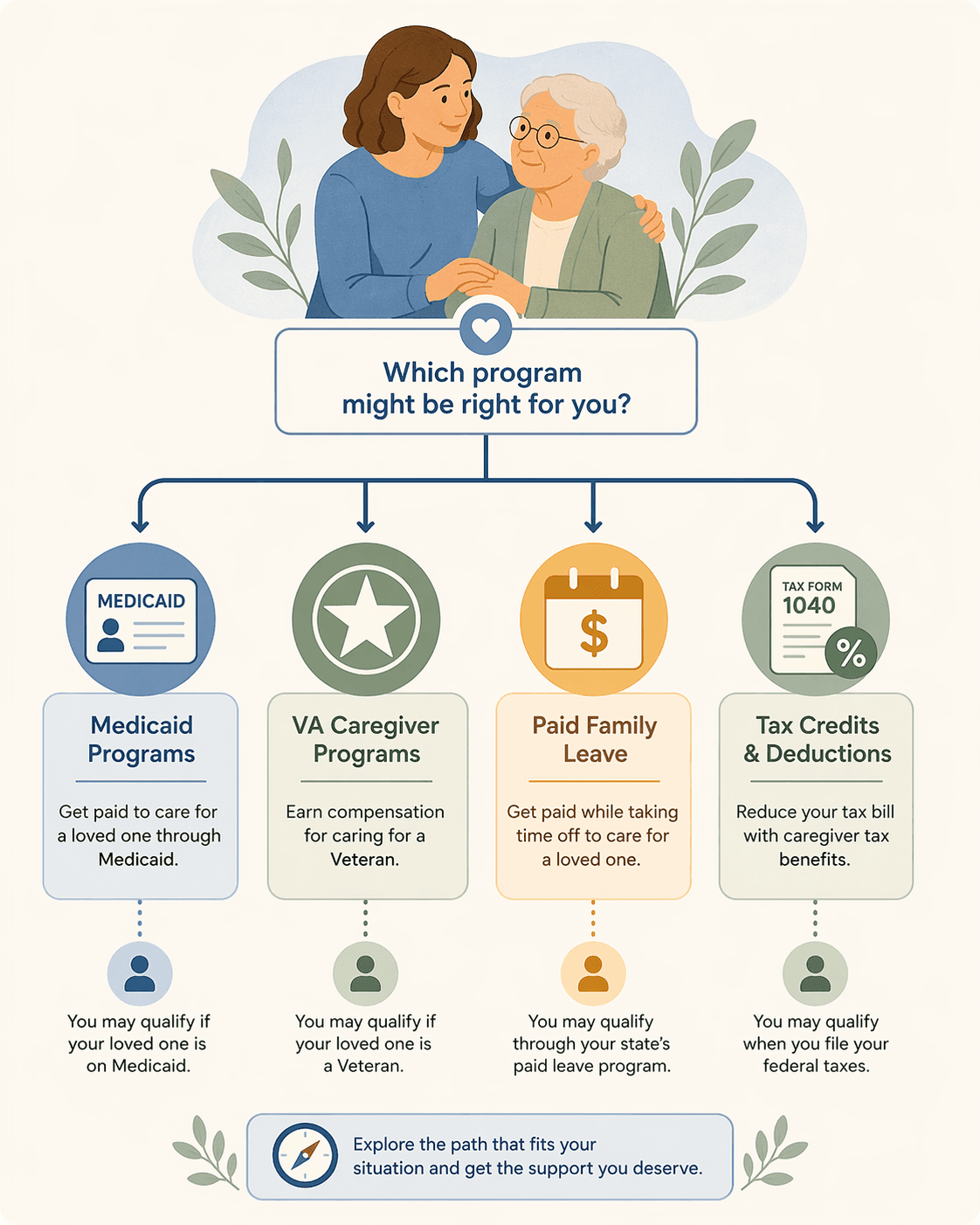

Medicaid Self-Directed Care: Can You Get Paid $13–$18 an Hour?

Medicaid isn't just for nursing homes. In most states, self-directed programs let the care recipient hire family members as paid caregivers. The national average rate is $13 to $18 per hour — but that's an average. Your state may pay half that, or more. The actual rate depends on the care recipient's functional need level (how many activities of daily living they need help with) and the state's Medicaid waiver structure. The eligibility filter: the care recipient's income must be low enough to qualify for Medicaid long-term care services in their state — usually around $2,829/month in most states (2025 limits). If your parent exceeds that, they may qualify through a "spend-down" or a waiver, but it's not automatic.

About 37 million Americans provide unpaid care each month. If your parent qualifies, you could be part of the subset that actually gets paid. But you apply through your state's Medicaid agency and get approved as a provider — it's not automatic.

VA Caregiver Compensation: If Your Loved One Is a Veteran

The VA's Program of Comprehensive Assistance for Family Caregivers (PCAFC) provides monthly cash stipends, training, counseling, and up to 30 days of respite care annually. That "up to" is a maximum, not a guarantee. Eligibility requires the veteran to have a serious service-connected injury and need in-person supervision or assistance with activities of daily living. The Aid and Attendance (A&A) and Housebound benefits are separate pension enhancements for veterans who need daily help — different rules, including a requirement of at least 90 days active duty with one day during a war period.

If your loved one is a veteran, this is the highest-value pathway available. But it's also the most restrictive. Start with the VA's eligibility checklist before spending time on the application.

State Paid Family Leave: Are You in One of the 15 States?

Paid family leave is not a national right. As of 2026, 11 states plus Washington, D.C. have enacted laws: California, Colorado, Connecticut, Massachusetts, New Hampshire, New Jersey, New York, Oregon, Rhode Island, Vermont, Washington. Four more — Delaware, Maine, Maryland, Minnesota — join in 2025–2026.

- Wage replacement rates range from 60% to 90% of your regular wages, depending on the state and your income level.

- Most states have a waiting period (typically 7 days) before benefits begin.

- The leave is job-protected in most states, so you can return to the same position.

- Washington's WA Cares Fund, starting benefits in July 2026, provides up to $36,500 per lifetime to pay for care, including care given by family members.

If you live in one of these states, paid leave can replace a significant portion of the income you lose when you take time off for caregiving. If you're in the other 35 states, this path is closed — for now.

Tax Credits: What You Can Claim Now — and What's Still Pending

Federal tax credits exist but are modest and come with strings. The Child and Dependent Care Credit can reimburse up to $3,000 for care expenses while you work — a credit, not a deduction, and nonrefundable (you can't get back more than you owe). The Credit for Other Dependents gives up to $500 per qualifying dependent. Both require earned income.

At the state level, six states — Georgia, Missouri, Montana, New Jersey, North Dakota, South Carolina — offer caregiver tax credits. Oklahoma and Nebraska enacted the first in 2023 and 2024. In 2026, 12 more states have considered similar legislation.

| Credit | Amount | Eligibility |

|---|---|---|

| Child and Dependent Care Credit | Up to $3,000 (one dependent) or $6,000 (two or more) | Must have earned income, care expenses while working |

| Credit for Other Dependents | Up to $500 per dependent | Dependent must meet IRS definition, caregiver must have earned income |

| State caregiver tax credits (6 states) | Varies by state (typically $500–$2,000) | Must be a resident of that state, meet state-specific criteria |

| Proposed Credit for Caring Act | $5,000 | Not yet enacted; would require caregiver to have earned income |

Long-term care insurance is rare — only 3% of adults over 50 have it. If your loved one does, check whether payments to informal caregivers are allowed; some newer policies do. A personal care agreement — a legal contract between care recipient and caregiver — can formalize payment and avoid gift tax issues, but it doesn't create a new source of money.

How to Decide Which Program to Pursue

The four pathways above — Medicaid self-directed care, VA compensation, state paid family leave, tax credits — form the map. But the map is useless without knowing which roads are open to you. Start with these questions:

- Where does the care recipient live? If it's a state with paid family leave, that's your first look. If not, move to Medicaid.

- Is the care recipient a veteran? If yes, check PCAFC eligibility first — it's the highest-value single program.

- Is the care recipient's income low enough for Medicaid? If yes, apply for self-directed care. If no, look at personal care agreements and tax credits.

- Are you employed? If yes, the Child and Dependent Care Credit and state paid leave (if available) are options. If no, focus on credits that don't require earned income (Credit for Other Dependents).

Concrete example: If you're a sandwich-generation caregiver in California, caring for a low-income mother who is not a veteran, your best path is California's In-Home Supportive Services (IHSS) — a self-directed Medicaid program that pays family caregivers. You can also use California's paid family leave for up to 8 weeks at 60–70% of your wages while you take time off. And you can claim the Child and Dependent Care Credit if you pay for care while you work.

The decision tree isn't about listing every program. It's about finding the one or two that actually apply to you — and then having the eligibility details to know whether it's worth your time. That's the difference between a fantasy list and a survival guide.

We didn't cover negotiating flexible schedules with your employer, or the emotional toll of asking for help. Those are real, but they belong in other guides. Here, the goal was to show you the money that exists and how to get it. If you found a path that fits your situation, start with one application. Just one. The hardest part is the first step, and the government forms are never easy, but the $28,700 question doesn't answer itself.

Continue Your Caregiving Journey

When you are ready, these resources can help with specific caregiving tasks.

- Private Companion vs. Agency Companion: A Decision Framework for Family Caregivers

A practical guide for adult children deciding whether to hire a companion for an aging parent privately or through an agency. Covers cost comparisons, a pros-and-cons decision table, step-by-step hiring instructions, legal responsibilities, and when the agency premium is worth it.

- The Emotional Toll No One Warns You About: Why Caring for an Aging Parent Affects Women and Men Differently — and How to Protect Your Mental Health

New Pew Research reveals a striking gender gap in caregiving's emotional toll: 47% of women vs. 30% of men report negative impacts on their well-being. This article explores the unequal task distribution driving this disparity and provides evidence-based strategies to protect your mental health.

- The Hidden Health Toll of Family Caregiving: What Every New Caregiver Needs to Know About Their Own Risks

Most new family caregivers focus entirely on their loved one and don't realize they face serious, documented health risks — from a 40-70% rate of clinically significant depression symptoms to immune system compromise that can last years. This article presents the data every new caregiver needs to know and offers a practical self-care framework for early intervention.

Comments

Join the discussion with an anonymous comment.