Home Health Care vs. Home Care vs. Assisted Living vs. Nursing Home: How to Choose the Right Senior Health Care Service

Home Health Care vs. Home Care vs. Assisted Living vs. Nursing Home: How to Choose the Right Senior Health Care Service

A crisis-mode comparison guide for adult children who need to quickly distinguish between the four most commonly confused senior care types — home health care, non-medical home care, assisted living, and nursing homes — using three clear decision dimensions: medical need, living safety, and who pays.

By Editorial Team

The Four Most Confusing Senior Care Options — At a Glance

If a doctor, social worker, or sibling just mentioned a care option you have never heard of, you are not alone. The four terms — home health care, home care, assisted living, and nursing home — are used interchangeably in casual conversation, but they describe fundamentally different services with different costs, different payment sources, and different purposes.

The fastest way to sort them is to ask three questions about your loved one:

Medical need: Does she need a nurse, physical therapist, or wound care ordered by a doctor, or does she need help with bathing, dressing, and meals?

Living safety: Can she remain safely at home with support, or does she need a supervised residential setting?

Payer: Will Medicare, Medicaid, private insurance, or the family's own savings cover the bill?

The table below maps each service type against those three dimensions using the most current national data available as of mid-2026.

Quick-reference comparison of the four most commonly confused senior care types. Cost figures are national medians; actual costs vary significantly by state and level of care needed.

Service Type

Who It Serves

Typical Cost (2026 National Median)

Primary Payer

Home Health Care

Homebound patients needing short-term skilled nursing, PT, or OT ordered by a doctor

Covered by Medicare (no cost to patient for qualifying services); private pay rates vary

Medicare Part A/B (short-term); Medicaid (varies by state); private insurance

Non-Medical Home Care

Seniors needing help with ADLs (bathing, dressing, meals) but not skilled medical care

$34–$35/hr (A Place for Mom 2026; CareScout 2025)

Private pay (almost always); long-term care insurance; some state Medicaid waiver programs

Assisted Living

Seniors who need daily personal care but not 24/7 skilled nursing

The senior care spectrum is a continuum, not a single decision. Each stage has a distinct purpose, cost structure, and payment source.

Home Health Care: Skilled Medical Care at Home (Short-Term)

What it is: Home health care is skilled medical care provided in the home. It is ordered by a physician and delivered by licensed professionals — registered nurses, physical therapists, occupational therapists, speech-language pathologists, and home health aides working under a nurse's supervision. The National Institute on Aging defines it as services such as medication management, wound care, and rehabilitation therapy.

Who needs it: A patient recovering from a hip replacement, a stroke, or a heart failure exacerbation who is homebound and needs short-term nursing or therapy. The key word is short-term. Medicare covers home health only for patients who are homebound and need part-time or intermittent skilled care. It does not cover 24-hour care, meal delivery, or help with bathing if that is the only need.

What Medicare covers: Medicare Part A and Part B cover home health services at no cost to the patient if all of the following conditions are met: a doctor certifies the need for skilled care; the patient is homebound; the care is provided by a Medicare-certified home health agency; and the care is part-time or intermittent (typically fewer than 28 hours per week). Medicare does not cover custodial care — the kind of help with daily activities that most families actually need long-term. This is the single most common and costly misunderstanding families encounter.

Costs: For qualifying patients, Medicare covers the full cost of skilled nursing and therapy visits. For patients who do not qualify, or who need more care than Medicare allows, private-pay home health rates vary widely. The 2026 Medicare changes include a Part B premium of $202.90/mo and a Part A inpatient deductible of $1,736, but these do not affect home health coverage for qualifying patients.

Non-Medical Home Care: Help with Daily Life (Long-Term)

What it is: Non-medical home care — often called "home care" or "personal care" — provides assistance with activities of daily living (ADLs): bathing, dressing, toileting, eating, transferring, and mobility. It also includes homemaking services like meal preparation, light housekeeping, laundry, and companionship. The caregiver is typically a home health aide or a companion, not a nurse or therapist.

Who needs it: A senior who is generally stable from a medical standpoint but can no longer safely bathe, dress, or prepare meals alone. She may have mild cognitive impairment, arthritis, or general frailty. She does not need a nurse, but she needs someone to be present for several hours a day — or around the clock — to prevent accidents and ensure basic needs are met.

What Medicare covers:Nothing. Medicare does not cover non-medical home care. This is the most important financial fact to understand: if your parent needs help with bathing and meals but does not need skilled nursing, Medicare will not pay for it. The same is true for most private health insurance plans. Long-term care insurance may cover some or all of the cost, but only if the policy was purchased before the need arose.

Costs: The national median rate for non-medical home care in 2026 is $34 per hour (A Place for Mom 2026), up from $35/hr in 2025 (CareScout). State medians range from $25/hr in Mississippi to $44/hr in South Dakota. At 44 hours per week — roughly the point where a senior needs care most of the day — the monthly cost reaches approximately $6,478, which is more than the national median for assisted living.

Assisted Living: Residential Care with Personal Support

What it is: Assisted living is a residential option for seniors who need help with daily activities but do not require 24/7 skilled nursing. Residents typically live in private apartments or rooms and receive personal care services (bathing, dressing, medication reminders), meals, housekeeping, transportation, and social activities. The National Institute on Aging notes that assisted living facilities provide 24-hour supervision but not the level of medical care found in a nursing home.

Who needs it: A senior who can no longer live safely alone — perhaps because of fall risk, medication mismanagement, or early-stage dementia — but who does not need a nurse on site around the clock. The typical assisted living resident needs help with two to three ADLs and has some degree of cognitive impairment, but is not bedbound or medically unstable.

What Medicare covers:Nothing. Medicare does not pay for assisted living. The vast majority of residents pay entirely out of pocket. Some states offer Medicaid waiver programs that can cover assisted living costs for low-income seniors, but eligibility and availability vary dramatically by state. Long-term care insurance may cover assisted living if the policy includes that benefit.

Costs: The national median cost for assisted living in 2025–2026 is approximately $6,200 per month (CareScout 2025), with SeniorLiving.org reporting $6,313/mo in May 2026. Pricing is typically tiered: a base rent covers housing and meals, and additional "care levels" are added as the resident's needs increase. A 2026 survey by SingleCare found that 56% of families mistakenly believe assisted living costs less than $4,000 per month — a misconception that can lead to serious financial surprises.

Nursing Homes (Skilled Nursing Facilities): 24/7 Medical Care

What it is: A nursing home — also called a skilled nursing facility (SNF) — provides round-the-clock skilled nursing care, rehabilitation services, and supervision for seniors who cannot be cared for safely at home or in an assisted living setting. The NIA explains that nursing homes provide 24-hour supervision, three meals daily, assistance with ADLs, and on-site nursing and medical care.

Who needs it: A senior who requires 24/7 nursing care — for example, someone with advanced dementia who is bedbound, has a feeding tube, needs frequent wound care, or has unstable medical conditions that require monitoring. Nursing homes also serve as short-term rehabilitation centers for patients recovering from a hospital stay (hip fracture, stroke, pneumonia) who need daily physical therapy but are not yet ready to go home.

What Medicare covers: Medicare covers short-term skilled nursing facility stays only after a qualifying hospital stay of at least three days. For 2026, the rules are: days 1–20 are fully covered after the Part A deductible ($1,736); days 21–100 require a copay of $217 per day (SeniorLiving.org 2026); after day 100, Medicare pays nothing. Medicare does not cover long-term custodial stays in a nursing home.

Costs and payment: The national median cost for a semi-private room in a nursing home is $9,842 per month ($118,104/year) as of May 2026; a private room costs $11,294/mo ($135,528/year). Costs rose 7% (semi-private) and 9% (private) year over year. Most families start by paying privately, then transition to Medicaid once the senior's assets are spent down. SingleCare reports that 6 in 10 nursing home residents rely on Medicaid, making it the largest payer for long-term care nationally (46% of all LTC spending in 2023).

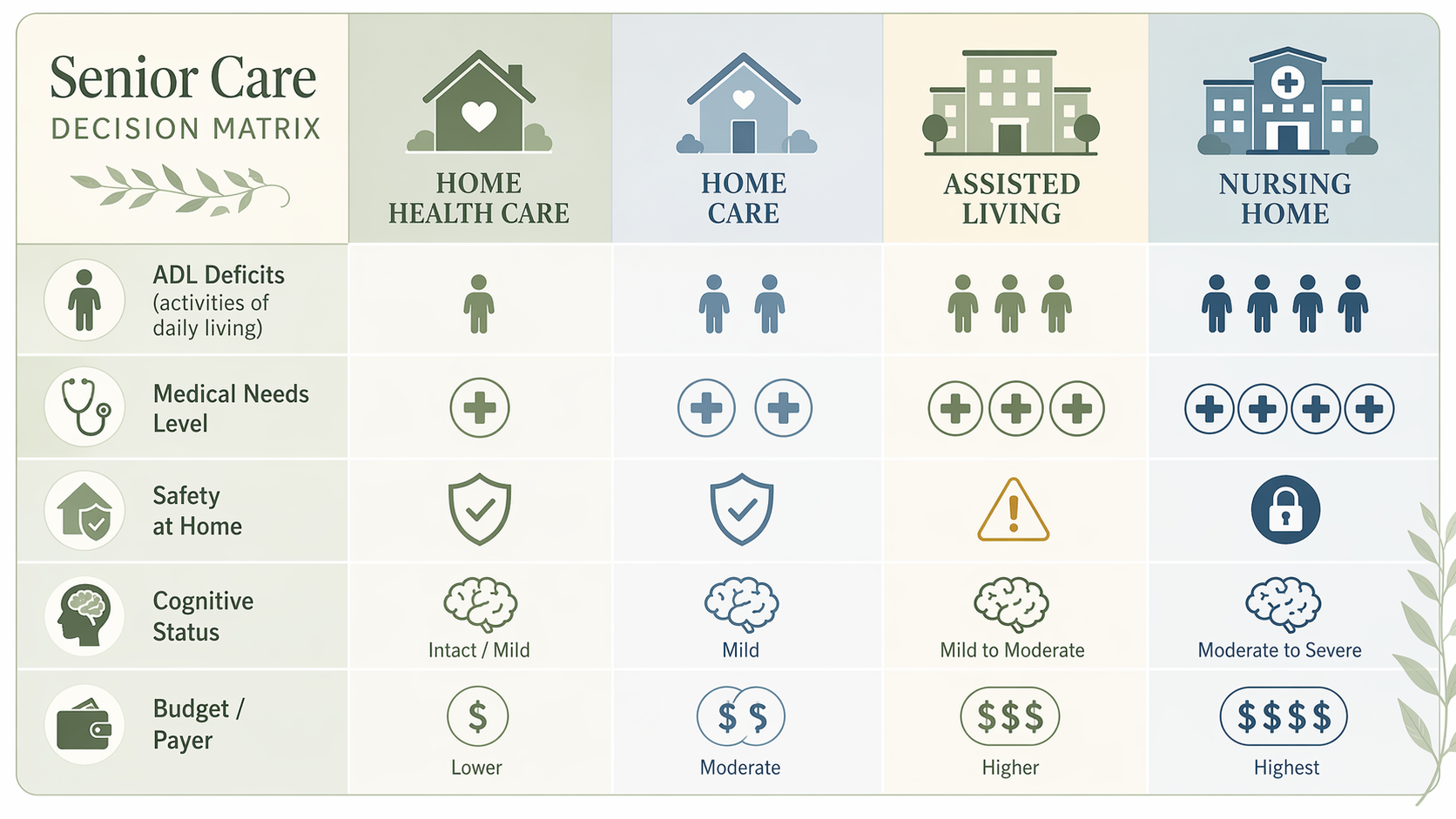

Decision Matrix: Which Service Fits Your Situation?

The following matrix maps the key decision factors — ADL deficits, medical complexity, cognitive status, caregiver availability, and budget — to the appropriate service type. Use it as a starting point for discussion with your loved one's doctor, a geriatric care manager, or a geriatric care manager (a licensed nurse or social worker who can assess needs and coordinate services, typically charging $75–$200/hour).

Use this decision matrix to match your loved one's needs to the right care category. No single factor determines the choice — it is the combination of medical need, living safety, and payer that points to the right option.

Decision matrix mapping key factors to the four service types. Use the column that matches most of your loved one's characteristics.

Decision Factor

Home Health Care

Non-Medical Home Care

Assisted Living

Nursing Home

ADL deficits

Minimal (skilled care is primary need)

Moderate (needs help with 2–4 ADLs)

Moderate (needs help with 2–3 ADLs)

High (needs help with most or all ADLs)

Medical complexity

High (requires skilled nursing, PT, OT)

Low (medically stable)

Low to moderate (may need medication management)

High (requires 24/7 skilled nursing)

Cognitive status

Any (care is medical, not cognitive)

Mild impairment acceptable

Mild to moderate impairment (some facilities have memory care wings)

Moderate to severe impairment (dementia, Alzheimer's)

Caregiver availability

Family caregiver can manage non-skilled needs

Family caregiver needs relief or cannot provide full-time care

No family caregiver available or caregiver burnout

No family caregiver available; 24/7 supervision required

Budget/payer

Medicare covers short-term; private pay for longer

Private pay ($34–$35/hr); LTC insurance; some Medicaid waivers

Private pay ($6,200/mo); some Medicaid waivers; LTC insurance

Private pay then Medicaid spend-down; Medicare for short-term rehab only

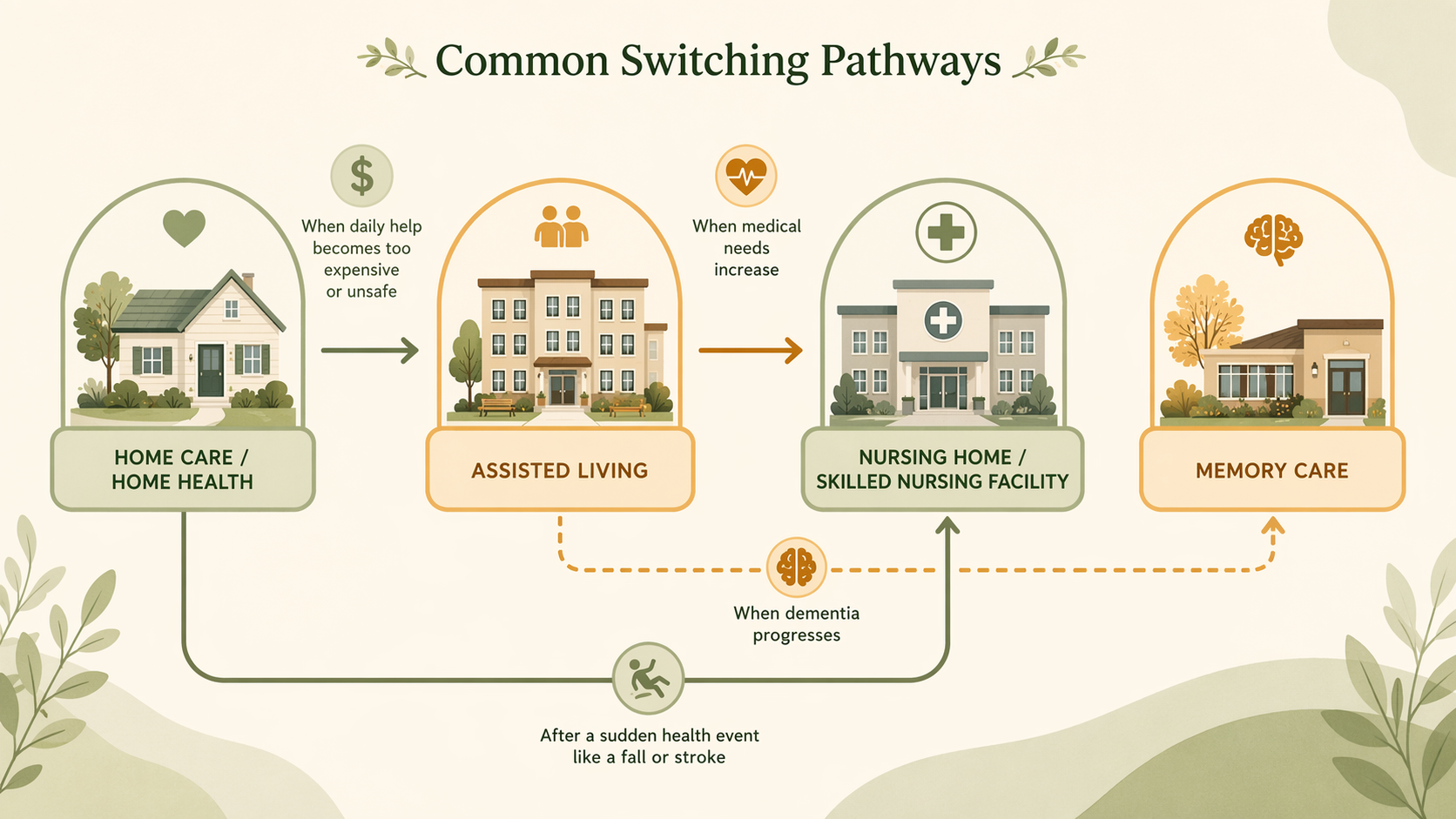

Common Switching Pathways: How Needs Escalate Over Time

Senior care is rarely a single decision. Most families move through two or more care levels as needs change. Understanding the common escalation pathways can help you anticipate what comes next and plan financially before a crisis forces a rushed move.

Common care escalation pathways. Most families follow one of these routes as needs progress. Planning ahead for the next step can save thousands of dollars and reduce stress.

Most common pathways:

Home care → Assisted living: This is the most common transition. The senior starts with a few hours of home care per week, but as needs increase, the cost of home care rises. When 44+ hours per week are needed, assisted living often becomes both cheaper and safer.

Home health → Home care: A patient receives Medicare-covered home health after a hospital stay. When the skilled care ends (typically after a few weeks), the family realizes the senior still needs help with daily activities — but now must pay privately for non-medical home care.

Assisted living → Memory care: A senior with dementia living in assisted living begins to wander, becomes agitated, or requires a secure environment. Many assisted living facilities have a dedicated memory care wing, or the resident may need to move to a stand-alone memory care community. See When to Move From Assisted Living to Memory Care for the specific warning signs.

Assisted living → Nursing home: A resident's medical condition deteriorates — a stroke, a fall with fracture, or progression of a chronic disease — to the point where 24/7 skilled nursing is required.

Home care → Nursing home (direct): Some seniors skip assisted living entirely and move directly from home to a nursing home when a sudden medical event (stroke, severe fall) creates an immediate need for round-the-clock nursing care.

The continuum of care model (CCRC): Some families choose a Continuing Care Retirement Community (CCRC), which offers independent living, assisted living, and skilled nursing on one campus. As myLifeSite explains, CCRCs typically charge a one-time entrance fee ($100,000–$2 million) plus monthly fees, but they allow residents to move between care levels without leaving the community. This can reduce the disruption of multiple moves, but the high entrance fee and complex contracts require careful financial and legal review.

Red Flags That the Current Care Level Is Wrong

No care plan is permanent. The following warning signs suggest that your loved one's needs have outgrown their current setting and that it is time to reassess.

Frequent falls or near-falls: If a senior is falling at home despite home care, or in assisted living despite supervision, the environment or level of support is insufficient.

Unexplained weight loss or dehydration: This often indicates that meal preparation, feeding assistance, or medical management is inadequate.

Medication errors or missed doses: If a senior cannot manage their own medications and the current care setting does not provide medication management, the risk of hospitalization rises sharply.

Caregiver burnout: If the family caregiver is exhausted, missing work, or experiencing health problems of their own, the current arrangement is not sustainable. 37 million family caregivers provide unpaid eldercare in the U.S., and caregiver burnout is a leading cause of premature nursing home placement.

Social isolation or depression: A senior who is alone at home for long hours, or who has stopped engaging in activities they once enjoyed, may need the social structure of a residential setting.

Hospital readmissions: If a senior is being readmitted to the hospital within 30 days of discharge, the post-acute care plan is failing. This may indicate that home health or home care is insufficient and that a skilled nursing facility is needed for rehabilitation.

Comments

Join the discussion with an anonymous comment.