The Overlooked Middle: Affordable Senior Housing Options for Seniors Who Don't Qualify for Medicaid but Can't Afford Private Assisted Living

Over 11 million middle-income seniors will be unable to afford senior housing by 2033. This guide helps adult children navigate the affordability gap for parents who earn too much for Medicaid but too little for private-pay assisted living, covering alternative pathways like shared housing, PACE programs, and state-specific waivers.

By Editorial Team

new caregiver

care coordination

first steps

Medicare

Medicaid

📄

A printable version of this guide is available. Use your browser's print function (Ctrl+P / ⌘P) to save or print.

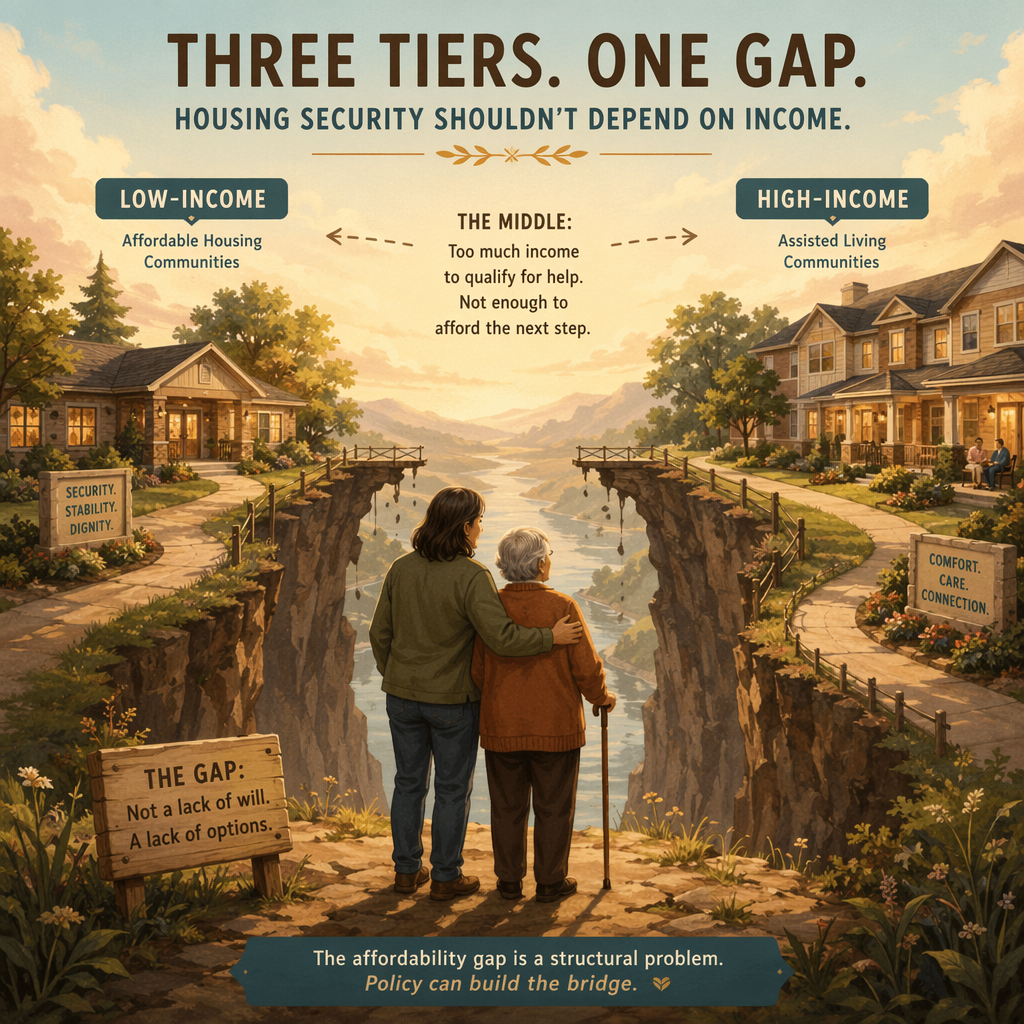

The 'forgotten middle' faces a structural gap in the senior housing market — too much income for Medicaid, too little for private-pay assisted living.

Who Is the 'Forgotten Middle'? Defining the Affordability Gap

The term 'forgotten middle' describes a rapidly growing cohort of older Americans who fall into a financial no-man's-land: they earn too much to qualify for Medicaid but have far too little saved to afford private-pay assisted living. For the purposes of this guide, we define this group as seniors with annual individual incomes roughly between $25,000 and $60,000. They are not poor enough for public assistance, and they are not wealthy enough to write a check for $70,000 a year in care.

This is not a fringe problem. According to a landmark study by NORC at the University of Chicago, more than 11 million middle-income seniors aged 75 and older may not be able to pay for assisted living by 2033. The same study projects that the middle-income senior population will grow by 89 percent — an additional 7.5 million people — between 2018 and 2033. By 2029, 54 percent of these seniors will lack the financial resources to meet yearly costs of $60,000 for assisted living, even if they committed 100 percent of their annual income.

The health profile of this group makes the situation even more urgent. Among middle-income seniors, more than half have three or more chronic conditions, 56 percent have mobility limitations, and one in three faces cognitive impairments. These are not hypothetical future needs — they are current, daily challenges that require some form of paid care or housing support.

The 2026 Numbers: Why the Math Doesn't Work

The financial mismatch at the heart of this crisis is stark. The median individual income for older adults (age 65+) in 2024 was just $33,310 per year, according to the Pension Rights Center. For older adults without earnings — which describes four-fifths of those over 65 — the median income drops to $26,770. Meanwhile, the median annual cost of assisted living in 2024 was $70,800, or $5,900 per month, according to the Genworth/CareScout Cost of Care Survey.

The core financial mismatch: median older adult income is less than half the median assisted living cost.

Metric

Amount

Source

Median individual income (age 65+)

$33,310/year

Pension Rights Center, 2024

Median household income (age 65+)

$56,680/year

Pension Rights Center, 2024

Median assisted living cost

$70,800/year ($5,900/month)

Genworth/CareScout, 2024

Middle-income seniors unable to afford care by 2029

54%

NORC / Health Affairs

Middle-income seniors unable to afford care by 2033

11+ million

NORC at UChicago

Even home equity — often cited as a safety net — does not close the gap for most families. The NORC study found that even if middle-income seniors sold their homes, 39 percent (6.1 million people) would still have insufficient resources to pay the annual costs of assisted living and medical care. In 2029, only 19 percent of middle-market seniors are projected to have the financial resources to afford housing and care without selling their homes.

The cost trajectory is also accelerating. Between 2021 and 2023, assisted living costs rose 18.9 percent. In 2024 alone, the median cost jumped another 10 percent year-over-year. Asking rent growth in senior housing has stabilized above 4 percent annually, and average operating margins for senior housing operators surpassed 25 percent in mid-2025 — the highest since 2018. The market is not building its way out of this problem either: new construction is at historic lows, with fewer than 1,500 new units added to primary markets in Q3 2025, representing just 0.7 percent year-over-year growth, the lowest on record since NIC MAP began tracking supply data in 2006.

Why Traditional Options Fail This Cohort

The 'forgotten middle' falls through the cracks because the two dominant models — private-pay assisted living and Medicaid — were not designed for them. Understanding why each option fails is the first step toward finding workable alternatives.

Private-pay assisted living is structurally out of reach. At $70,800 per year, assisted living consumes more than double the median individual income of an older adult. Even households with two incomes struggle: the median older household income is $56,680, still $14,000 short of the annual assisted living cost. A KFF public opinion survey found that 83 percent of adults said it would be impossible or very difficult to pay $60,000 a year for an assisted living facility.

Medicaid coverage for assisted living is extremely limited. Only 18 percent of residential care facilities agree to accept Medicaid payments, according to a federal survey. Even in facilities that do accept Medicaid, it is often limited to a minority of beds. This means that even if a senior eventually spends down to Medicaid eligibility, they may not be able to stay in their chosen facility or find a Medicaid-accepting bed in their area.

Asset tests disqualify many middle-income seniors. Medicaid is designed for those with very low income and assets. A senior with $50,000 in savings, a paid-off home, and a $35,000 annual Social Security income may be too 'asset-rich' to qualify for Medicaid in many states, yet too income-poor to afford private-pay assisted living.

Hidden fees and tiered pricing erode affordability. A KFF Health News investigation found that the median annual price of assisted living increased 31 percent faster than inflation from 2004 to 2021, nearly doubling to $54,000. By 2024, it had reached $70,800. Half of operators earn returns of 20 percent or more above operating costs. A class-action lawsuit against Aegis Living, settled for $16 million, highlighted a point system that charged residents 64 cents per point per day for additional services — costs that quickly add up beyond the base rent.

Alternative Pathway 1: Subsidized and Income-Restricted Senior Housing

For seniors who fall into the 'forgotten middle,' federally subsidized housing programs can provide a critical foundation. These programs are not a perfect solution — waitlists are long, and availability varies dramatically by region — but they are one of the few options designed specifically for older adults with limited income.

HUD Section 202 Supportive Housing for the Elderly: This program provides rental assistance and supportive services for very low-income seniors aged 62 and older. Residents pay 30 percent of their adjusted income toward rent, with the federal subsidy covering the remainder. The program is specifically designed for seniors who need some supportive services but not the full medical model of a nursing home. However, funding is limited, and waitlists in many cities stretch for years.

Low-Income Housing Tax Credit (LIHTC) Properties: These are privately owned apartment buildings that receive tax credits in exchange for renting to households earning below a certain percentage of the area median income. Many LIHTC properties set aside units for seniors. Income limits vary by location but typically target households earning 50-60 percent of area median income — which often aligns with the 'forgotten middle' range in lower-cost areas.

Public Housing for Seniors: Local public housing authorities operate apartment buildings specifically for seniors. Rent is typically set at 30 percent of adjusted income. These units are often the most affordable option available, but availability is extremely limited in many markets.

Housing Choice Vouchers (Section 8): Seniors can use a voucher to rent a private apartment and pay approximately 30 percent of their income toward rent. However, waitlists for vouchers are often closed for years at a time in high-demand areas.

A key limitation of these programs is that they provide housing but not necessarily care. A senior who needs help with bathing, medication management, or meals may need to layer in home care services — which brings its own cost challenges. However, for seniors who are still relatively independent, subsidized housing can dramatically reduce monthly expenses, freeing up income for other needs.

Alternative Pathway 2: PACE Programs and Home-Based Care Models

The Program of All-Inclusive Care for the Elderly (PACE) is one of the most promising — and most underutilized — options for the 'forgotten middle.' PACE provides comprehensive medical care, adult day services, and some in-home support to seniors who are eligible for nursing home care but can live safely in the community with coordinated support.

PACE is funded through a combination of Medicare and Medicaid, but it serves a broader population than traditional Medicaid. In many states, seniors who do not qualify for full Medicaid can still enroll in PACE by paying a monthly premium for the Medicaid portion of the benefit. This makes PACE accessible to some middle-income seniors who would otherwise be locked out of both private-pay and Medicaid-covered care.

PACE covers: primary care, specialist visits, hospital care, prescription drugs, adult day center services, physical and occupational therapy, meals, transportation to the PACE center, and some in-home personal care.

PACE does not cover: 24-hour in-home care, assisted living facility costs, or nursing home care (though it can coordinate with these settings).

Eligibility: The senior must be 55 or older, live in a PACE service area, and be certified by their state as needing a nursing home level of care. They must be able to live safely in the community with PACE support.

For seniors who do not have a PACE program nearby, home-based care models offer another bridge. Programs like 'Money Follows the Person' allow Medicaid funds to be used for home and community-based services rather than institutional care. Some states also offer home health aide services through Medicaid waivers that have higher income thresholds than traditional nursing home Medicaid.

Alternative Pathway 3: Shared Housing, Adult Family Homes, and State Waivers

Beyond the well-known options, a range of smaller-scale, less formal arrangements can serve the 'forgotten middle' — often at a fraction of the cost of traditional assisted living. These options require more legwork to find and evaluate, but they can be the difference between a parent receiving care and going without.

Lesser-known housing and care options for the 'forgotten middle' with typical cost ranges and limitations.

Option

Typical Cost Range

Best For

Key Limitation

Adult family home (2-6 residents)

$2,500 - $5,000/month

Seniors who need moderate assistance but want a home-like setting

Limited availability; state licensing varies widely

Shared housing / home-sharing

$800 - $2,000/month (per person)

Relatively independent seniors who need companionship and light support

No built-in care services; must arrange separately

HCBS Medicaid waiver (assisted living)

Varies by state; often covers room, board, and care

Seniors whose state offers a waiver with higher income thresholds

Only available in certain states; waitlists common

Money Follows the Person program

Covers home and community-based services

Seniors transitioning from nursing home to community setting

Requires a qualifying nursing home stay first

Adult family homes — also called residential care homes or board-and-care homes — are private residences that house 2 to 6 residents and provide meals, personal care, and supervision. They are typically much less expensive than large assisted living communities, with costs ranging from $2,500 to $5,000 per month depending on location and level of care. However, they are not regulated in all states, and quality varies dramatically. A thorough in-person visit and background check are essential.

Shared housing arrangements — where a senior rents a room in a private home or shares a larger apartment with another older adult — can reduce housing costs to $800 to $2,000 per month. Organizations like HomeShare and local Area Agencies on Aging sometimes facilitate these matches. The trade-off is that no formal care services are included; the arrangement is purely housing, and any care needs must be met separately through home care aides or family support.

State-specific Home and Community-Based Services (HCBS) Medicaid waivers are perhaps the most important tool for the 'forgotten middle,' but they are also the most complex. These waivers allow states to use Medicaid funds to pay for assisted living, adult day care, and in-home support for seniors who would otherwise need nursing home care. Crucially, some states set higher income thresholds for these waivers than for traditional nursing home Medicaid, making them accessible to middle-income seniors.

State-by-State Variation: Where the Options Are Better

The availability of affordable senior housing and care for the 'forgotten middle' depends heavily on where your parent lives. Some states have invested in broader waiver programs, higher income thresholds, and more robust PACE networks. Others have done very little.

Examples of states with more favorable programs for middle-income seniors. This is not an exhaustive list — always verify current eligibility rules with your state's Medicaid office.

State

Notable Programs

Key Feature for 'Forgotten Middle'

California

PACE programs, Medi-Cal HCBS waivers, Adult Day Health Care

Multiple PACE sites; some waivers have higher income thresholds for assisted living

New York

PACE, Managed Long-Term Care (MLTC), Adult Family Homes

MLTC plans coordinate care for dual-eligible seniors; strong adult family home network

Texas

STAR+PLUS waiver, PACE programs

STAR+PLUS waiver covers home and community-based services; expanding PACE availability

Pennsylvania

Community HealthChoices, PACE

Managed care program for seniors; PACE programs in Philadelphia and Pittsburgh

Oregon

K Plan (Medicaid waiver), Adult Foster Homes

Strong adult foster home network; K Plan covers home and community-based services

Florida

Statewide Medicaid Managed Care (SMMC), PACE

SMMC Long-Term Care program covers assisted living and home care; PACE in major cities

A few general patterns emerge. States that have expanded Medicaid under the Affordable Care Act tend to have more generous HCBS waiver programs. States with strong managed long-term care programs (like New York and Pennsylvania) often provide better coordination of services. And states with a high density of PACE programs (California, Texas, New York) offer more options for seniors who want to remain in the community.

Action Checklist: What to Do If Your Parent Is in the 'Forgotten Middle'

If you suspect your parent falls into the 'forgotten middle' — too much income for Medicaid, too little for private-pay assisted living — here is a step-by-step action plan. This is not a quick fix, but it is a systematic way to identify every possible pathway.

Determine your parent's exact income and asset position. Gather all income sources (Social Security, pensions, retirement accounts, part-time work) and all assets (savings, investments, home equity, vehicles). Compare this to your state's Medicaid income and asset limits for both nursing home Medicaid and HCBS waivers. Do not assume — the limits vary by state and program type.

Research state-specific HCBS waiver programs. Contact your state's Medicaid office or your local Area Agency on Aging and ask specifically about Home and Community-Based Services waivers that cover assisted living or in-home care. Ask about income thresholds, waitlists, and whether the waiver covers the type of care your parent needs.

Explore HUD Section 202 and LIHTC properties in your area. Use HUD's online resource locator to find subsidized senior housing. Call each property directly to ask about current waitlist status and income limits. Be prepared for waitlists of one to three years in most markets.

Evaluate PACE program availability. Use the National PACE Association's directory to check if a PACE program serves your parent's zip code. If one exists, schedule an informational meeting to understand eligibility, costs, and what services are covered.

Consider shared housing or adult family homes. Search for adult family homes through your state's Department of Social Services or licensing agency. For shared housing, contact local home-sharing organizations or your Area Agency on Aging. Visit any potential home in person and check licensing and complaint records.

Build a layered funding strategy. Most 'forgotten middle' families will need to combine multiple programs and resources: a subsidized apartment (HUD Section 202) plus a PACE program for medical care, or an adult family home plus a state HCBS waiver for care costs. Do not expect any single program to cover everything.

Six alternative pathways for the 'forgotten middle' — no single option works for everyone, but a layered strategy combining multiple programs can close the affordability gap.

Comments

Join the discussion with an anonymous comment.