Senior Care Options in 2026: The Real Costs Families Pay and the Hidden Expenses That Catch Them Off Guard

A comprehensive guide for family caregivers facing the financial shock of senior care. We break down 2026 benchmark pricing across all major options and reveal the five hidden costs — home modifications, tiered care pricing, LTC insurance elimination periods, caregiver career impact, and inflation — that can double the true expense. Includes a funding source matrix and a budget-planning worksheet to help families plan realistically.

By Editorial Team

senior care options

cost of care

hidden costs

family caregiver

financial planning

📄

A printable version of this guide is available. Use your browser's print function (Ctrl+P / ⌘P) to save or print.

Your Parent Needs Care. Here’s What It Actually Costs — and What No One Tells You Until After You’ve Committed.

The phone call comes on a Tuesday. Your mother fell. She’s safe, but she can’t go home alone. Within hours, you’re searching for “senior care options” and discovering a world where monthly rates rival a mortgage and the fine print contains expenses you never anticipated. This is the financial shock that millions of families face every year, and it almost always arrives without warning.

The core problem is a dangerous gap between perception and reality. According to the National Institute on Aging, Medicare does not cover custodial long-term care — the kind of daily assistance with bathing, dressing, eating, and mobility that most older adults eventually need. Yet a majority of Americans believe their health insurance will cover them if they need help. It won’t. And the sticker price you see on a facility’s brochure is only the beginning.

This guide exists to close that gap. We’ve assembled the 2026 benchmark pricing for every major senior care option, then peeled back the surface to reveal the five hidden costs that can double your true expense. You’ll find a funding source matrix that shows exactly what each payer covers and where it falls short, plus a budget-planning worksheet to help you estimate your family’s real total cost of care. The goal is not to overwhelm you — it’s to make sure you enter this decision with your eyes open.

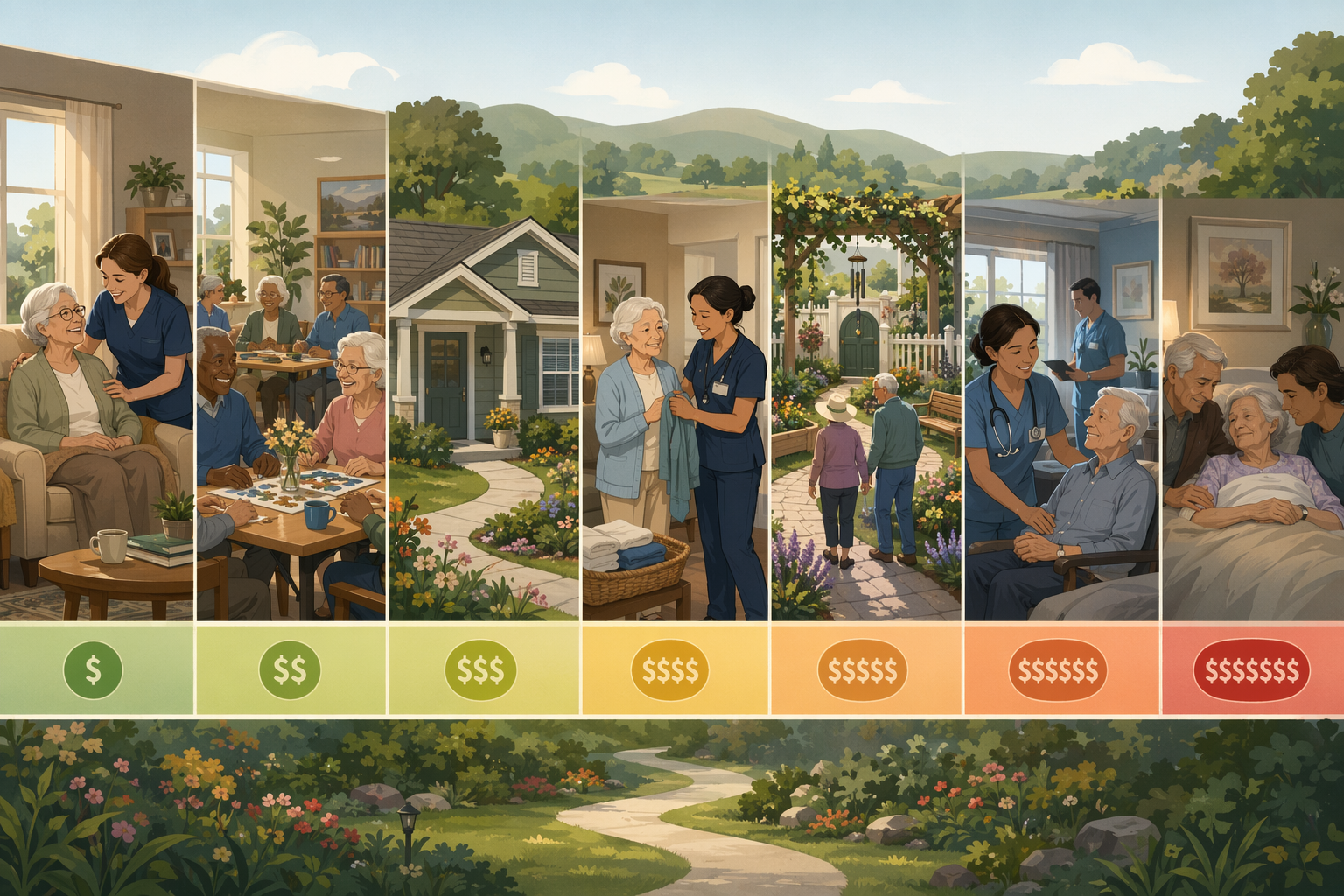

The senior care spectrum: care options range from in-home support to skilled nursing, with costs rising significantly as medical and supervision needs increase.

2026 Benchmark Pricing: What Nine Major Senior Care Options Actually Cost

Before we examine the hidden costs, we need a clear picture of the baseline. The table below draws on the CareScout 2025 Cost of Care Survey (fielded July–November 2025) and U.S. News 2026 reporting to present national median costs for the nine most common senior care arrangements. These are planning benchmarks, not quotes. Actual costs vary significantly by state, metro area, and level of care required.

2026 national median costs for senior care options. Sources: CareScout 2025 Cost of Care Survey, U.S. News 2026 senior living reporting, and A Place for Mom 2026 Cost of Care Report.

Care Option

National Median Cost (2026)

Typical Payment Model

Key Note

Home Care (non-medical)

$35/hour; ~$6,062/month at 44 hrs/week

Hourly or daily rate

Costs rise with hours; 24/7 care is far more expensive than assisted living

Adult Day Services

$95 per eight-hour day

Daily rate

Affordable option for daytime supervision; does not cover nights or weekends

Independent Living

$3,523/month

Monthly rent + optional services

No personal care or medical support included

Assisted Living

$6,200/month

Base rate + tiered care fees

Base rate covers only low-level assistance; costs rise as needs increase

Board and Care Home (Private)

$7,300/month

Monthly all-inclusive rate

Smaller settings (20 or fewer residents); less regulation than larger facilities

Memory Care

$7,645/month

Base rate + tiered care fees

20–30% more expensive than standard assisted living (U.S. News)

Nursing Home (Semi-Private)

$9,581/month

Daily or monthly rate

Medicare covers short-term stays only; Medicaid is primary payer for long-term

Nursing Home (Private)

$10,798/month

Daily or monthly rate

Private rooms command a premium; availability varies by region

CCRC (Continuing Care Retirement Community)

Entrance fee $100k–$2M + $3k–$8k/month

Lump-sum entrance fee + monthly fee

Covers independent living through skilled nursing on one campus; contracts vary widely

Hidden Cost #1: Home Modifications for Aging in Place

Families who choose home care often assume the $35/hour rate covers everything. It doesn’t. The home itself must be made safe, and that work carries a price tag that can rival several months of facility care.

According to U.S. News, home modifications such as grab bars, walk-in showers, ramps, and stair lifts represent a significant hidden cost of aging in place. These are structural changes, not optional upgrades. A bathroom without grab bars is a fall waiting to happen. A home with stairs and no ramp is inaccessible to a wheelchair user. The costs add up quickly.

Grab bars and bathroom safety rails: $50–$200 per bar, plus professional installation ($150–$500)

Walk-in shower or tub conversion: $2,500–$10,000

Ramp installation (modular or custom): $800–$5,000

Stair lift (straight or curved): $3,000–$15,000

Widening doorways for wheelchair access: $500–$3,000 per doorway

Full bathroom remodel for accessibility: $10,000–$25,000+

A comprehensive home safety retrofit can run from $5,000 for basic modifications to $50,000 or more for a full renovation. Medicare and standard health insurance do not cover these costs. Some Medicaid waivers and VA grants may help, but eligibility is narrow and application processes are slow.

An accessible bathroom remodel is one of the most common and costly home modifications families face when choosing to age in place.

Hidden Cost #2: Tiered Care Pricing in Assisted Living

The $6,200/month figure for assisted living is a median base rate. It almost never covers the full cost of care for a resident with moderate or high needs. Most assisted living facilities use a tiered pricing model: the base rate covers a low level of assistance (Level 1), and monthly costs increase by $500–$2,000 as a resident’s needs progress to Level 2, Level 3, or beyond.

Here’s how it typically works in practice. A family tours a facility and is quoted $6,200/month. They budget for that number. But within six to twelve months, their parent’s needs increase — more help with bathing, medication management, or mobility assistance — and the monthly cost jumps to $7,200, then $8,200. The family is now paying 30% more than they planned, and they have no easy way to move their parent to a cheaper option without causing disruption.

U.S. News explicitly warns that assisted living uses tiered pricing and that monthly costs rise as care needs increase. The Alzheimer’s Association notes that memory care, which is already 20–30% more expensive than standard assisted living, uses the same tiered structure. A family budgeting for Level 1 memory care at $7,645/month could find themselves at Level 3 within a year, paying $9,500–$10,000/month.

Hidden Cost #3: The Long-Term Care Insurance Elimination Period

If your parent has a long-term care insurance policy, you might assume it will cover costs from day one. That assumption can be expensive. Most LTC insurance policies include an elimination period — a waiting period of 30 to 90 days during which the policyholder must pay 100% of care costs out-of-pocket before benefits begin.

U.S. News identifies the LTC elimination period as a significant hidden cost of senior care. Consider the math: if your parent enters assisted living at $6,200/month and has a 90-day elimination period, the family must cover $18,600 out-of-pocket before the insurance company pays a single dollar. For a nursing home at $10,798/month, a 90-day elimination period means $32,394 in upfront costs.

This timing is particularly cruel because the elimination period coincides with the most financially stressful period of caregiving — the first few months, when families are also paying for home modifications, medical equipment, transportation, and lost income from reduced work hours.

Hidden Cost #4: Unpaid Caregiver Wages and Career Impact

The most invisible cost of senior care is the one that doesn’t appear on any invoice: the financial toll on the family caregiver. In the United States, 53 million people provide unpaid care to an adult family member. These caregivers absorb costs that never show up in a facility’s pricing brochure, yet they are very real.

The economic impact includes:

Lost wages from reduced work hours or leaving the workforce entirely

Reduced retirement savings contributions during caregiving years

Missed promotions and career advancement opportunities

Increased healthcare costs from caregiver stress and burnout

Out-of-pocket spending on care supplies, transportation, and medical equipment not covered by insurance

There’s also a critical financial break-even point that families rarely consider. According to U.S. News, home care at $35/hour for 44 hours per week costs approximately $6,062/month — roughly equal to the median cost of assisted living. The break-even point is around 40 hours per week. If a family caregiver is providing more than 40 hours of unpaid care per week, the economic value of that care exceeds the cost of assisted living. In other words, choosing to provide care at home may actually be the more expensive option when you account for the caregiver’s lost income.

Hidden Cost #5: Inflation — The Silent Budget Killer

Inflation is the hidden cost that compounds silently over years, and it hits senior care harder than most household expenses. In 2024 alone, the median cost of assisted living surged by 10% (New LifeStyles). That’s more than double the general inflation rate and far above the Social Security Cost-of-Living Adjustment (COLA) for the same year.

U.S. News projects the long-term impact of even modest inflation on senior care costs. At a 3.8% annual inflation rate:

Projected annual costs at 3.8% inflation. These are estimates based on current national medians and do not account for regional variation or above-average inflation in healthcare services.

Care Option

2026 Annual Cost

Cost in 10 Years (2036)

Cost in 20 Years (2046)

Assisted Living

$74,400

~$108,000

~$157,000

Nursing Home (Private)

$129,575

~$188,000

~$273,000

Home Care (44 hrs/week)

$80,080

~$116,000

~$169,000

Memory Care

$91,740

~$133,000

~$193,000

This is not a hypothetical concern. Assisted living costs rose 5% from 2024 to 2025 alone (A Place for Mom 2026 Cost of Care Report). For families planning five, ten, or twenty years ahead — especially those considering a CCRC with escalating monthly fees — inflation can turn an affordable plan into an unsustainable one.

Funding Source Matrix: What Each Option Covers and Its Key Limitation

Understanding which funding sources cover which types of care is essential to realistic planning. The matrix below summarizes the six major payers, what they cover, and the most important limitation families need to know.

Major funding sources for senior care. Source: National Institute on Aging, U.S. News, SeniorLiving.org, and New LifeStyles 2026 reporting.

Funding Source

What It Covers

What It Does NOT Cover

Key Limitation

Medicare

Short-term skilled nursing (days 1–20 fully covered after Part A deductible; days 21–100 have $217/day copay in 2026); some home health care; hospice

Custodial long-term care (assistance with ADLs); assisted living; most home care beyond skilled needs

Medicare does not cover the type of daily care that most older adults eventually need (NIA)

Medicaid

Long-term nursing home care; some home and community-based services (waivers vary by state)

Most assisted living (coverage varies by state); care in facilities that don’t accept Medicaid

Requires strict financial eligibility (spend-down) and a five-year look-back period for asset transfers

Long-Term Care Insurance

Care in home, assisted living, or nursing home up to policy limits

Care beyond policy maximums; pre-existing conditions during waiting periods

Elimination period (30–90 days) requires out-of-pocket payment before benefits begin; policies vary widely

VA Benefits (Aid and Attendance)

Up to $2,424/month for single veterans; $2,874/month for married veterans; $1,558/month for surviving spouse

Care at facilities that don’t meet VA standards; some home care costs

Requires proof of medical need and financial eligibility; application process can take months

Private Pay (Out-of-Pocket)

Any care option the family can afford

Nothing — but it depletes savings rapidly

No safety net; a year of assisted living at $74,400 can exhaust a $200,000 nest egg in under three years

PACE (Program of All-Inclusive Care for the Elderly)

Comprehensive medical and long-term care services for frail older adults living in the community

Care outside the PACE network; 24/7 in-home care

Available only in certain states and service areas; requires Medicare/Medicaid eligibility

Budget-Planning Worksheet: Estimating Your True Total Cost of Care

Use the worksheet below to estimate your family’s real monthly and annual cost of care. This goes beyond the base rate to include the hidden costs we’ve covered. Fill in the line items that apply to your situation.

Budget-planning worksheet for estimating the true total cost of senior care. Fill in each line item that applies to your situation.

Cost Category

Your Estimate (Monthly)

Notes

Base care cost (from pricing table above)

$______

Use the national median for your care type, then adjust for your metro area

Tiered care increase (assisted living or memory care)

$______

Add $500–$2,000/month for each level above Level 1

Home modifications (one-time, amortized over 12 months)

$______

Divide total modification cost by 12 for monthly budget impact

LTC insurance elimination period out-of-pocket (amortized)

$______

Divide total elimination period cost by 12 if you’re in the first year

Caregiver lost income (if providing unpaid care)

$______

Estimate reduced work hours × hourly wage; or use $35/hr for care value

Medical equipment and supplies not covered by insurance

$______

Include walkers, hospital beds, incontinence supplies, etc.

Transportation (medical appointments, errands)

$______

Include mileage, parking, and any specialized transport services

Food and utilities (if care is at home)

$______

Add the cost of additional groceries and increased utility usage

Inflation adjustment (for multi-year planning)

$______

Multiply total by 1.038 for each year beyond the first

Total Estimated Monthly Cost

$______

Sum all line items above

Once you have your total estimate, compare it against your family’s available income and savings. If the gap is larger than expected, you’re not alone — and there are strategies to close it.

The decision about senior care is never just a financial one. It involves emotion, family dynamics, and the deeply personal question of what “good care” looks like for someone you love. But the financial reality is the foundation on which every other decision rests. By understanding the full cost — the sticker price and the five hidden costs that so often catch families off guard — you can make a plan that is both compassionate and sustainable.

Comments

Join the discussion with an anonymous comment.