The True Cost of Assisted Care: A Financial Roadmap for Families Comparing Home Care, Assisted Living, and Nursing Homes in 2026

A comprehensive financial roadmap comparing all major assisted care options — home care, adult day, assisted living, board and care, memory care, and nursing homes — with national median costs, state-by-state variation, payment pathways, hidden fees, and contingency planning for families managing a parent's care finances.

- Device / Aid Type

- assistive devices and mobility aids

- Functional Need Addressed

- comprehensive cost comparison and financial planning for assisted care options

- Professional Assessment

- An occupational therapist or physical therapist is recommended for individual device selection and fitting.

- Last Reviewed

- 2026-06-20

- assisted living cost

- home care cost

- nursing home cost

- Medicaid

- VA Aid and Attendance

- long-term care insurance

- senior care financial planning

The Cost Confusion: Why 'Staying Home' Can Be the Most Expensive Option

When a parent begins to struggle with daily tasks, the first instinct for many adult children is to bring in help at home. It feels safer, more familiar, and intuitively less expensive than moving them into a facility. That intuition, however, is often wrong.

According to 2026 data from CareScout and the American Health Care Association / National Center for Assisted Living (AHCA/NCAL), full-time home care — defined as 44 hours per week of non-medical caregiver support — carries a national median cost of $80,080 per year. That figure exceeds the national median for assisted living, which sits at $74,000 per year ($6,200/month). The gap widens further when you factor in the mortgage, utilities, property taxes, home maintenance, and grocery costs that continue regardless of whether a senior lives at home or in a residential setting.

The confusion is understandable. The senior care market is fragmented, pricing is opaque, and most families have no prior experience navigating it. A 2025 U.S. News survey found that 94% of older adults prefer to age in place, yet the same survey revealed that families systematically underestimate the cost of the care required to make that possible. The result is a financial blind spot that can exhaust savings years earlier than expected.

This article provides a comprehensive, multi-option cost comparison across every major assisted care level — home care, adult day services, assisted living, board and care homes, memory care, and nursing homes — along with state-by-state variation, payment pathways, hidden fees, and contingency planning for the scenario every family dreads: running out of money.

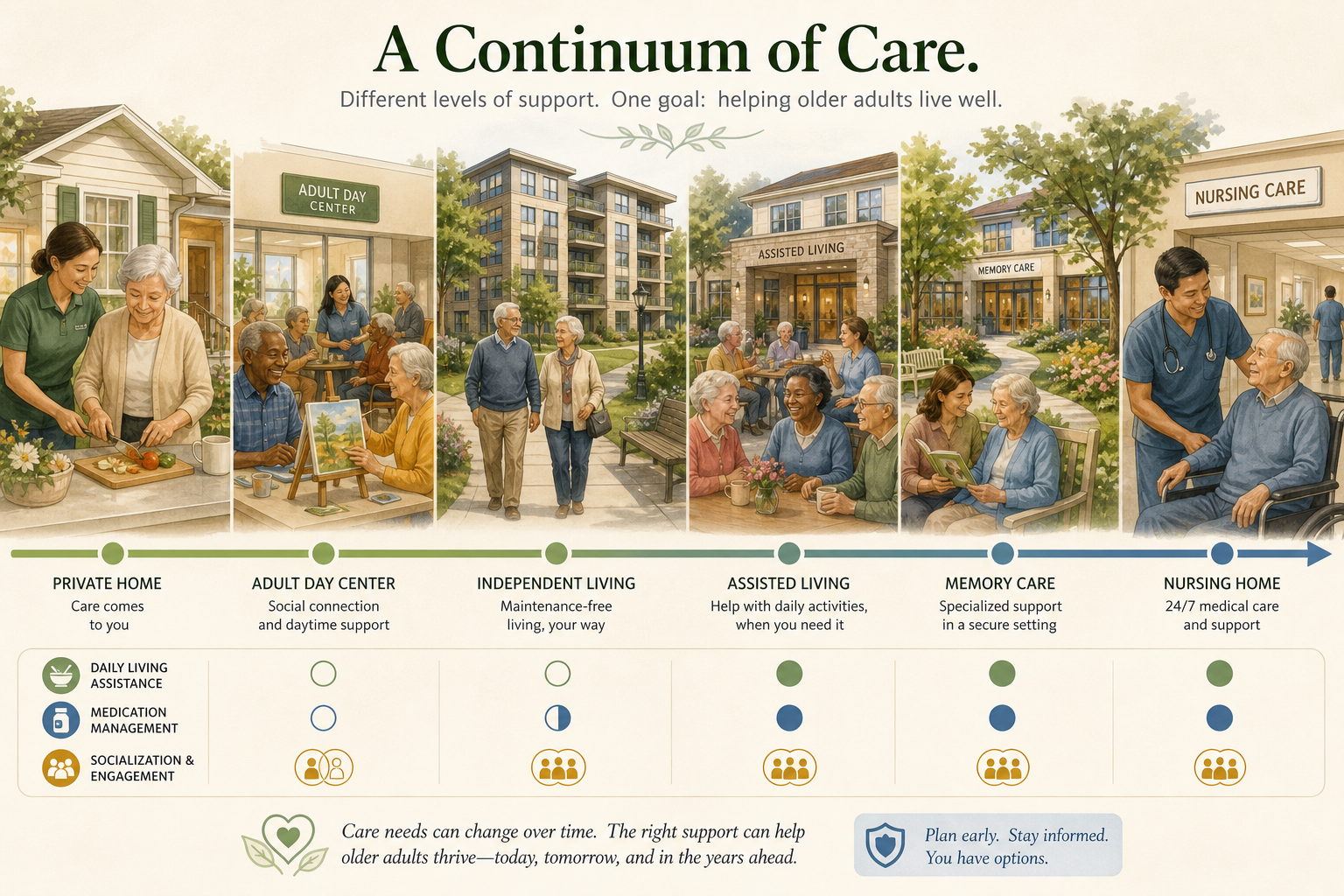

National Median Cost Comparison: Every Assisted Care Option in One Table

The table below consolidates 2026 national median cost data from AHCA/NCAL and CareScout (via U.S. News) for every major assisted care category. These figures represent the national midpoint — actual costs in your area may be significantly higher or lower, a topic we address in the next section.

| Care Option | Monthly Cost (Median) | Annual Cost (Median) | Key Details |

|---|---|---|---|

| Adult Day Health Care | $2,058 | $24,700 | Typically 5–8 hours/day; no overnight care |

| Independent Living | $3,523 | $42,276 | Minimal or no assistance with ADLs; social focus |

| Assisted Living | $6,200 | $74,000 | Help with ADLs, meals, medication oversight; 24-hr supervision |

| Board and Care Home (Shared) | $6,000 | $72,000 | Small residential home; ≤20 residents; shared room |

| Board and Care Home (Private) | $7,300 | $87,600 | Same setting; private room |

| Memory Care | $7,645 | $91,740 | Secured unit; dementia-specific programming; higher staff ratio |

| Home Care (44 hrs/week) | $6,673 | $80,080 | Non-medical; hourly rate ~$35/hr; no housing costs included |

| Nursing Home (Semi-Private) | $9,581 | $114,975 | Skilled nursing; 24/7 medical oversight; shared room |

| Nursing Home (Private) | $10,798 | $129,575 | Same level of care; private room |

Several patterns jump out from this data. First, the assumption that home care is cheaper than residential care only holds if the senior needs fewer than roughly 35 hours of paid help per week. At 44 hours — a common threshold for someone who cannot be left alone safely — home care becomes more expensive than assisted living. Second, the jump from assisted living to nursing home care is dramatic: a private nursing home room costs nearly 75% more than assisted living. Third, memory care, while expensive, sits well below nursing home costs, reflecting its position as a specialized assisted living product rather than a skilled nursing service.

For a deeper dive into the home care versus assisted living decision, see our guide Home Care vs. Assisted Living: The 40-Hour Rule, which walks through the math and trade-offs in detail.

State-by-State Variation: Why Location Changes Everything

National medians are useful for ballpark planning, but they can be dangerously misleading for families in high-cost or low-cost states. Assisted living costs vary by a factor of two or more depending on where you live. A facility that costs $3,500/month in rural Missouri may command $8,500/month in downtown San Francisco or Manhattan.

The same geographic spread applies to home care. Hourly rates for non-medical caregivers range from roughly $20/hour in parts of the South and Midwest to over $40/hour in major coastal cities. For a family needing 44 hours per week, that difference alone can shift the annual cost by more than $45,000.

- High-cost states (CA, NY, MA, CT, DC, HI): Assisted living often exceeds $7,500–$9,000/month. Home care rates typically $35–$45/hour. Nursing home private rooms can surpass $15,000/month.

- Mid-cost states (FL, TX, IL, PA, VA, CO): Assisted living generally falls in the $4,500–$6,500/month range. Home care rates $25–$35/hour. Nursing homes $8,000–$11,000/month.

- Low-cost states (MO, AR, MS, AL, OK, WV): Assisted living can be as low as $3,000–$4,000/month. Home care rates $18–$25/hour. Nursing homes $6,000–$8,000/month.

State-level variation also affects Medicaid coverage for assisted living. Some states offer generous home- and community-based services (HCBS) waivers that cover assisted living costs for eligible seniors; others have limited or no such programs. This is a critical factor in long-term financial planning, as we discuss in the payment pathways section below.

For help matching your parent's specific care needs to the appropriate level of support, see our decision guide: Independent Living vs. Assisted Living vs. Nursing Home: How to Match Your Parent's Needs to the Right Level of Care.

Payment Pathways: How Families Actually Pay for Assisted Care

Very few families pay for long-term care entirely out of pocket from start to finish. Most rely on a combination of public benefits, insurance, and personal savings. Understanding which pathways are available — and in what order to pursue them — can mean the difference between exhausting assets in two years and sustaining care for a decade.

Medicaid

Medicaid is the single largest payer for long-term care in the United States. According to AHCA/NCAL, 17% of assisted living residents currently rely on Medicaid to cover their costs. More broadly, the Centers for Medicare & Medicaid Services (CMS) reported that in fiscal year 2023, 63.8% of all Medicaid long-term services and supports (LTSS) spending — $145.9 billion — went to home- and community-based services, reflecting a decades-long policy shift away from institutional care.

Medicaid eligibility is based on both income and assets, and rules vary significantly by state. Some states offer HCBS waivers that cover assisted living, adult day care, and in-home support; others do not. For families planning ahead, consulting with a Medicaid planner or elder law attorney is often a worthwhile investment.

VA Aid and Attendance

For veterans and surviving spouses, the VA Aid and Attendance pension benefit can provide substantial monthly payments to help cover the cost of assisted living, home care, or nursing home care. As of 2026, the maximum monthly benefit amounts are:

- Single veteran: up to $2,424/month

- Married veteran: up to $2,874/month

- Surviving spouse: up to $1,558/month

These benefits are not automatic — they require an application and documentation of both wartime service and medical need. The VA also provides long-term care services directly through VA nursing homes and community living centers, though there may be waiting lists.

Long-Term Care Insurance

Long-term care insurance (LTCI) policies cover services in the home, assisted living, or nursing home settings, depending on the policy. However, the market has contracted significantly in recent years as insurers raised premiums and tightened underwriting. For families who already have a policy, it is essential to understand the daily benefit amount, the elimination period (waiting period before benefits begin), and whether the policy covers the specific type of care needed.

Reverse Mortgages and Life Insurance Conversions

For seniors aged 62 and older who own their home, a reverse mortgage can provide tax-free funds to pay for care without requiring monthly repayments. The loan is repaid when the homeowner sells the home, moves out permanently, or passes away. There are no income or medical requirements to qualify.

Some life insurance policies offer accelerated death benefits or viatical settlements that allow the policyholder to access a portion of the death benefit while still alive if they need long-term care. This can be a valuable bridge for families who are asset-rich but cash-poor.

Private Pay

Private pay — paying out of personal savings, retirement accounts, or family contributions — remains the most common initial payment method for assisted living and home care. The challenge is sustainability. At $74,000/year for assisted living or $80,000/year for home care, a couple's retirement savings can be depleted rapidly. This is why understanding the full cost landscape and planning for a potential transition to Medicaid or VA benefits is critical.

For a comprehensive walkthrough of eligibility, application steps, and strategies for each payment pathway, see our family guide: How to Pay for Senior Health Care Services: A Family Guide to Medicare, Medicaid, Private Pay, and Everything in Between. For a full list of funding sources including state and local programs, see How to Pay for Elderly Care: 7 Funding Sources to Cover the $34/HR Cost in 2026.

What Medicare Does and Does Not Cover

Medicare is a health insurance program, not a long-term care program. It covers medically necessary services: doctor visits, hospital stays, prescription drugs, and — under limited circumstances — skilled nursing facility (SNF) care and home health care. Specifically:

- Skilled nursing facility (SNF) care: Medicare Part A covers up to 100 days of SNF care per benefit period, but only after a qualifying hospital stay of at least three days. Days 1–20 are fully covered; days 21–100 require a daily coinsurance payment ($204/day in 2026). After day 100, Medicare pays nothing.

- Home health care: Medicare covers part-time or intermittent skilled nursing care and physical/occupational therapy at home, but only if the person is homebound and under a physician's plan of care. It does not cover 24/7 care, meal delivery, or personal care assistance (bathing, dressing) unless skilled care is also being provided.

- Assisted living, board and care, memory care: Not covered. Medicare does not pay for room and board, custodial care, or supervision in any residential setting.

Medicare Advantage (Part C) plans may offer some additional benefits like adult day care or transportation, but they do not cover custodial care or assisted living. Families should never assume Medicare will cover a parent's long-term care needs — verify every benefit against the specific plan.

For a deeper exploration of this topic and the most common financial blind spots, see The Real Cost of Long-Term Senior Care: Why Most Families Get It Wrong and How to Plan.

Hidden Costs to Ask About on Every Tour

The monthly base rate quoted by an assisted living facility or board and care home is rarely the full monthly cost. Most facilities use a tiered pricing model where the base rate covers a minimum level of care, and additional services incur extra charges. These hidden costs can add $1,000–$3,000 or more to the monthly bill.

Here are the most common hidden fees families should ask about during every tour and phone call:

- Care tier pricing: Most facilities charge a base rate for a low level of care (e.g., 30 minutes of assistance per day). If your parent needs help with two or more activities of daily living (ADLs) — bathing, dressing, toileting, transferring, eating — the monthly cost can jump by $500–$2,000 or more. Always ask for the full care tier schedule.

- Medication management fees: Some facilities charge a flat monthly fee for medication oversight; others charge per medication. For a parent on 8–12 medications, this can add $200–$600/month.

- Community or entrance fees: Many assisted living communities charge a one-time community fee ($1,000–$5,000) upon move-in. This is often non-refundable.

- Transportation fees: Some facilities include scheduled transportation in the base rate; others charge per trip or require a monthly transportation fee ($50–$200/month).

- Amenity and activity fees: Cable TV, telephone, internet, and some social activities may be billed separately. These typically add $100–$300/month.

- Respite or trial stay fees: Short-term stays are often priced at a premium daily rate that is higher than the monthly rate divided by 30.

The same principle applies to home care agencies. Many charge a higher rate for weekends, holidays, and overnight shifts. Some require a minimum number of hours per visit (e.g., 4 hours), which can inflate costs if you only need 2 hours of help. Always request a complete fee schedule in writing before signing any agreement.

For an expanded analysis of costs that are often overlooked when keeping a parent at home, see The Hidden Costs of Aging in Place in 2026: Why Families Underestimate the True Price Tag. For a detailed breakdown of 24/7 home care costs and hidden expenses, see How Much Does 24/7 Home Care Cost in 2026?.

Running Out of Money: Contingency Planning for Families

The hardest conversation in senior care financial planning is the one no one wants to have: what happens when the money runs out. For families paying privately, the average assisted living stay of 22–28 months can deplete a $200,000 nest egg in under three years. Nursing home costs can exhaust it even faster.

Contingency planning is not defeatist — it is responsible stewardship of a family's resources. Here are the key strategies to consider:

- State Medicaid spend-down rules: Most states allow seniors to "spend down" their assets to the Medicaid eligibility threshold by paying for medical and long-term care expenses. Once assets fall below the threshold (typically $2,000–$10,000 depending on the state), Medicaid can begin covering care costs. The key is understanding the rules before the crisis hits — improper transfers of assets can trigger a penalty period of Medicaid ineligibility.

- Transitioning from private pay to Medicaid within a facility: Not all assisted living facilities accept Medicaid. Those that do may have a limited number of Medicaid beds. Families should ask during the initial tour whether the facility accepts Medicaid and what the process is for transitioning from private pay to Medicaid if assets are depleted.

- Family contribution pooling: Siblings can pool resources to cover the gap between a parent's income (Social Security, pension) and the cost of care. A written agreement clarifying each person's contribution and whether it is a gift or a loan can prevent conflict later.

- Downsizing and asset liquidation: Selling the family home is often the single largest source of funds for long-term care. The proceeds can be used for private pay, or the home can be sold and the proceeds spent down to qualify for Medicaid. A reverse mortgage can also provide ongoing income without requiring a sale.

- Life insurance conversion: As noted above, some life insurance policies allow the policyholder to access the death benefit early to pay for long-term care. This can provide a critical bridge for families who have exhausted other resources.

For additional money-saving strategies and a comprehensive overview of assistance programs, see The Complete 2026 Guide to Affordable Senior Care: Costs, Assistance Programs, and Money-Saving Strategies. This guide covers state-specific programs, nonprofit grants, and practical steps families can take to stretch their care dollars further.

Related Guides

- Transfer Aids and Techniques for Senior Caregivers: Matching Equipment to Mobility Level

A practical guide for family caregivers on selecting the right transfer aid for a senior's actual weight-bearing capacity and applying safe, step-by-step techniques for the most common home transfer scenarios — from bed to wheelchair to car — including special considerations for seniors with dementia.

- The 9 in 10 Problem: Why Most Homes Aren't Ready for Aging in Place — and a Practical Room-by-Room Upgrade Plan for Families

Only 10% of U.S. homes are equipped for safe aging, yet over 90% of older adults want to stay home. This guide helps adult children and caregivers create a prioritized, budget-aware modification plan — starting with low-cost, high-impact changes and progressing to larger projects — so a parent can live independently and safely.

- When a Senior Refuses to Bathe: Understanding the Why and What to Do About It

Bathing refusal in older adults is rarely about stubbornness. This guide helps family caregivers identify the root cause — from fear of falling and sensory changes to dementia-related distortions and loss of dignity — and provides targeted, non-coercive strategies to make bathing safer, more comfortable, and more manageable.

Comments

Join the discussion with an anonymous comment.