Glossary entry

The Medicare DME Prevention Paradox: What Won't Medicare Pay For and How to Plan for the Gap

The Prevention Paradox: Medicare Pays for Falls, Not Prevention

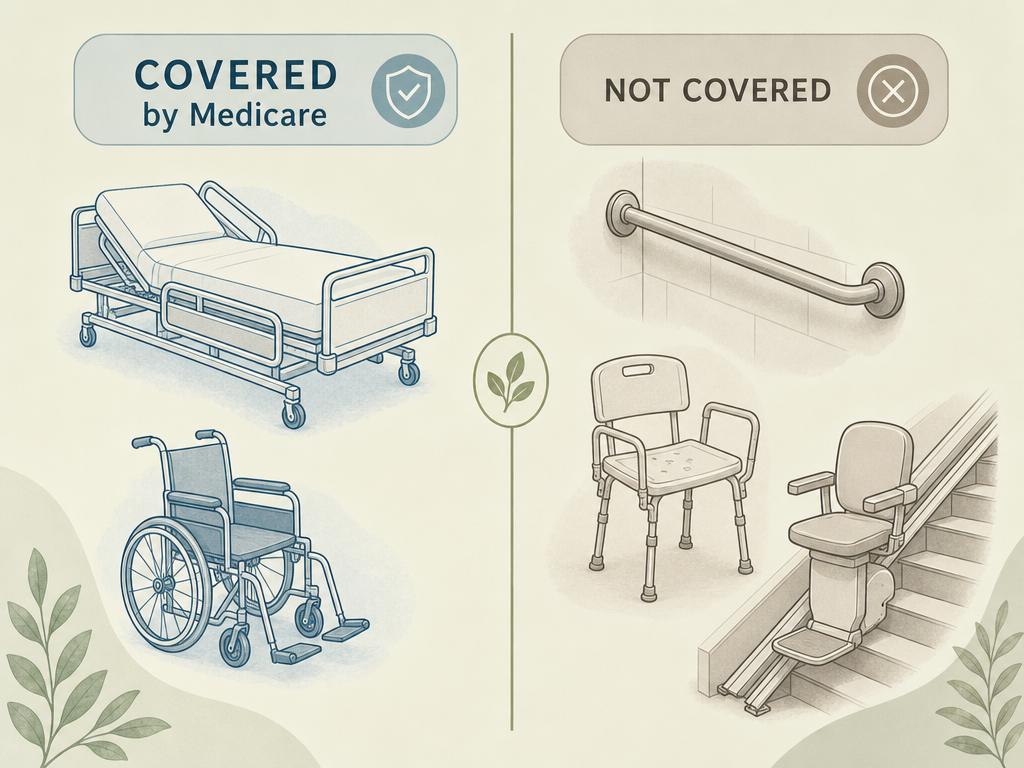

If you are planning a home for an aging parent, you have likely encountered a frustrating reality: Medicare will pay thousands of dollars for a hospital bed or a wheelchair after a fall, but it will not pay the $50 for a grab bar that might have prevented the fall in the first place. This is the prevention paradox, and it is one of the most common — and costly — surprises family caregivers face.

Under Original Medicare Part B, durable medical equipment (DME) is defined as equipment that is durable, used for a medical reason, useful only to someone who is sick or injured, used in the home, and expected to last at least three years. Items that meet these criteria — such as walkers, wheelchairs, hospital beds, and oxygen equipment — are covered at 80% after you meet the annual deductible. But items designed primarily for safety, convenience, or home modification do not qualify, even when they are far more likely to keep your parent out of the emergency room.

Nearly 19% of older adults in the United States use mobility devices such as walkers, canes, or crutches, according to a 2020 study cited by the American Academy of Physical Medicine and Rehabilitation. Yet a 2007 study found that fewer than half of chronically disabled Medicare beneficiaries — and less than one-quarter of the newly disabled — received any DME through Medicare at all. The gap between what seniors need and what Medicare covers is not small, and it falls squarely on family caregivers to fill.

This article focuses exclusively on what Medicare does not cover — the safety and mobility equipment that prevents falls, supports daily independence, and keeps seniors at home. If you need a refresher on the general DME definition or the standard process for getting covered equipment, see our comprehensive DME overview article for that foundation.

What Medicare Does NOT Cover: The Complete List of Excluded Safety Equipment

The following items are explicitly excluded from Medicare DME coverage. Some are classified as "home modifications," others as "convenience items," and a few fall outside the definition because they are designed for outdoor use or are disposable. Regardless of the classification, the result is the same: you pay the full cost.

| Item | Typical Use | Why Medicare Excludes It |

|---|---|---|

| Grab bars | Bathroom and shower safety | Classified as a home modification |

| Shower chairs / bath benches | Safe bathing for those with balance issues | Considered a convenience item |

| Stair lifts | Navigating stairs with mobility limitations | Classified as a home modification |

| Wheelchair ramps | Home access for wheelchair users | Classified as a home modification |

| Lift chairs (seat lift mechanisms) | Standing up from a seated position | Considered a convenience item |

| Motorized scooters for outdoor use | Mobility outside the home | Not for use in the home |

| Air conditioners, humidifiers, dehumidifiers | Home air quality adjustment | Not medical equipment |

| Most disposable items (gloves, incontinence pads) | Daily care and hygiene | Single-use or disposable |

| Exercise bicycles or fitness equipment | Prevention and fitness | Designed to prevent injuries, not treat them |

| Customized accessories for hospital beds or wheelchairs | Comfort or positioning | Not standard DME |

This list is not exhaustive, but it covers the items that most frequently surprise family caregivers. For example, a shower chair may be the single most important piece of equipment for preventing bathroom falls, yet Medicare treats it as a convenience item. Similarly, grab bars are among the most effective fall prevention tools available, but they fall under home modifications, not DME.

Why Medicare Excludes These Items: The 'Home Modification' and 'Convenience' Classification

Understanding why Medicare excludes these items will not change the coverage rules, but it will help you plan more effectively. Medicare's DME definition is narrow by design: equipment must be "primarily and customarily used to serve a medical purpose" and "generally not useful to a person in the absence of illness or injury." A grab bar, by contrast, is useful to anyone who wants to avoid slipping in the shower — not just someone who is sick or injured. A stair lift is a permanent home modification, not a piece of medical equipment you can take with you to the hospital.

This classification logic creates a perverse incentive. Medicare will pay for the hospital stay, surgery, and rehabilitation after a fall — costs that can easily reach tens of thousands of dollars — but it will not pay for the $50 grab bar or the $200 shower chair that might have prevented the fall entirely. The system is designed to treat illness and injury, not to prevent them, and family caregivers bear the financial burden of that gap.

It is important to note that this is not a flaw in Medicare's administration; it is a feature of the statutory definition of DME. The Centers for Medicare & Medicaid Services (CMS) follows the law as written. Caregivers who understand this distinction can stop wasting energy fighting the system and start focusing on the strategies that actually work to bridge the gap.

The Financial Impact: What These Items Actually Cost Out of Pocket

The out-of-pocket costs for non-covered equipment vary dramatically, from a few dollars for a basic grab bar to several thousand for a stair lift or ramp. The following table provides typical price ranges so you can budget realistically.

| Item | Typical Price Range | Notes |

|---|---|---|

| Grab bars | $15 – $50 | Installation may add $100–$300 if professionally installed |

| Shower chairs / bath benches | $30 – $200 | Basic models under $50; bariatric or padded models cost more |

| Raised toilet seats | $25 – $80 | Some models include armrests for additional support |

| Stair lifts | $3,000 – $10,000 | Straight staircases cost less; curved tracks cost significantly more |

| Wheelchair ramps | $1,000 – $5,000 | Portable ramps start around $200; permanent modular ramps cost more |

| Lift chairs (seat lift) | $500 – $3,000 | Basic models start around $500; premium models with heat and massage cost more |

| Transfer aids (transfer boards, transfer poles) | $30 – $200 | Simple transfer boards are inexpensive; poles require ceiling or floor mounting |

For context, the 2026 Medicare Part B deductible is $283, and you pay 20% coinsurance on covered items. But for the items above, you pay 100%. A family equipping a single bathroom with grab bars, a shower chair, and a raised toilet seat might spend $200–$400 out of pocket — a fraction of the cost of a single fall-related emergency room visit, which averages well over $1,000.

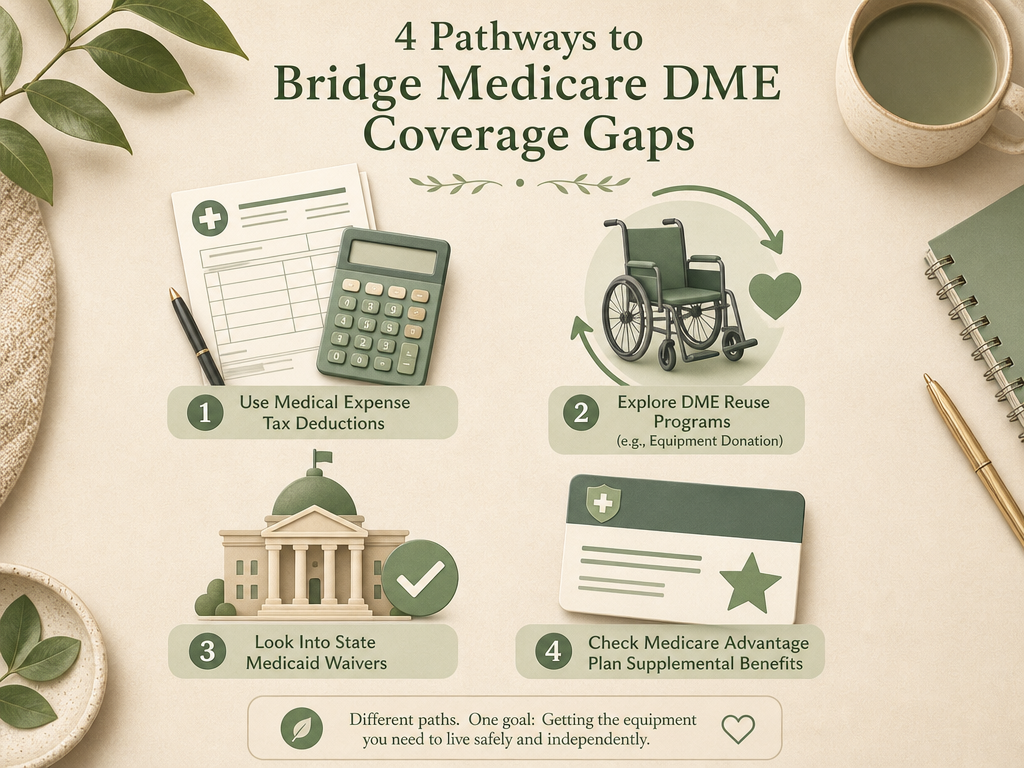

5 Strategies to Bridge the Coverage Gap

Since Medicare will not pay for most safety and prevention equipment, you need alternative strategies. The following five approaches can significantly reduce your out-of-pocket costs.

1. Medical Expense Tax Deduction

The IRS allows you to deduct unreimbursed medical expenses that exceed 7.5% of your adjusted gross income (AGI). This includes the cost of many non-covered DME items, such as grab bars, shower chairs, stair lifts, and ramps, as long as they are prescribed by a physician to treat a specific medical condition. Keep the prescription, receipts, and any documentation of medical necessity. If your parent's total medical expenses for the year — including premiums, prescriptions, and equipment — exceed 7.5% of their AGI, the excess is deductible.

2. DME Reuse Programs (Project MEND, RSVP, and Local Nonprofits)

Community-based DME reuse programs collect, sanitize, repair, and redistribute gently used equipment to uninsured and underinsured individuals. Two well-established programs are Project MEND in San Antonio and the Rehabilitation Services Volunteer Project (RSVP) in the Greater Houston area. RSVP also offers free physical and occupational therapy evaluations through a volunteer clinician network. Many local Area Agencies on Aging and faith-based organizations run similar equipment loan closets. A quick call to your local Area Agency on Aging can often connect you to a program in your area.

3. State Medicaid Waivers

While Original Medicare does not cover home modifications, some state Medicaid waivers — particularly Home and Community-Based Services (HCBS) waivers — may cover grab bars, ramps, and other safety modifications for dual-eligible beneficiaries (those who qualify for both Medicare and Medicaid). Coverage varies significantly by state and by waiver program. Contact your state Medicaid office or a local SHIP counselor to find out what is available in your state. For a deeper dive into funding sources, see our complete guide to funding sources for home modifications.

4. Veterans Aid and Attendance Benefits

If your parent is a veteran or surviving spouse, the VA Aid and Attendance benefit may provide funds to help cover the cost of home modifications and safety equipment. This is a monthly pension supplement for veterans who need assistance with activities of daily living. The funds can be used for a wide range of home safety improvements, including grab bars, ramps, and stair lifts. Contact your local VA regional office or a VA-accredited claims agent to determine eligibility.

5. Local Nonprofit Equipment Loan Closets

Many communities have equipment loan closets run by churches, senior centers, or service organizations like the Lions Club or Kiwanis. These programs lend walkers, wheelchairs, shower chairs, and other equipment at no cost, often for as long as needed. Search online for "medical equipment loan closet" plus your city or county name, or call your local senior center. These programs are often under-publicized but can be a lifeline for families facing immediate needs.

Medicare Advantage vs. Original Medicare: How Plans Differ on Non-Covered Items

Medicare Advantage (Part C) plans are required to cover the same DME items as Original Medicare, but they may offer additional supplemental benefits that Original Medicare does not. Some Medicare Advantage plans include allowances for home modifications, such as grab bars or bathroom safety equipment, as part of their supplemental benefits package. Others may offer a flexible spending card that can be used for over-the-counter items, including some safety equipment.

However, these benefits vary widely by plan and by year. A plan that covered grab bars in 2025 may not cover them in 2026, and a plan offered in one county may have different benefits than the same plan in another county. The only way to know for sure is to review the plan's Evidence of Coverage (EOC) document, which lists all covered benefits and any exclusions. If you are considering a Medicare Advantage plan for a parent, look specifically for plans that advertise "home modification allowances" or "supplemental benefits for safety equipment."

When to Push Back: Documenting Medical Necessity and Filing an Appeal

For most of the items on the non-covered list, an appeal under Original Medicare will not succeed because the items are excluded by statute, not by a coverage determination. However, there are borderline cases where a well-documented appeal may work. For example, a lift chair (a recliner with a powered seat lift mechanism) may be covered if a physician documents that the patient needs it for positional relief of a specific medical condition, such as severe orthostatic hypotension or congestive heart failure. Similarly, a specialized alternating pressure pad for a hospital bed may be covered with proper documentation, even though standard mattress overlays are not.

If you believe an item should be covered and has been wrongly denied, here is the appeals process for Original Medicare:

- File a redetermination with the DME Medicare Administrative Contractor (MAC) within 120 days of the date on your Medicare Summary Notice (MSN).

- If the redetermination is denied, file a reconsideration request with Maximus (the DME Qualified Independent Contractor) within 60 days. You can submit this online at qicappeals.cms.gov, by mail to 3750 Monroe Avenue, Suite 777, Pittsford, NY 14534, or by fax to 585-869-3314.

- If you miss a deadline, you can request a "good-cause extension" — Medicare may grant additional time if you had a medical emergency or other valid reason for the delay.

According to a 2023 KFF analysis cited by the National Council on Aging, only 11% of Medicare Advantage prior authorization denials were appealed by enrollees, but 82% of those appeals resulted in full or partial overturn of the initial denial. While this statistic applies to Medicare Advantage rather than Original Medicare DME appeals, it underscores a critical point: most people do not appeal, and those who do often succeed.

The prevention paradox is frustrating, but it is not insurmountable. By understanding exactly what Medicare does not cover, budgeting for the out-of-pocket costs, and using the strategies outlined above, you can equip your parent's home with the safety equipment they need — without relying on a system that was never designed to pay for prevention.

For a room-by-room assessment of fall risks and the specific equipment that can help, see our bathroom safety checklist for seniors and our complete guide to bathroom remodeling for aging in place.

Browse more in the Glossary.