This guide helps adult children plan home care for an aging parent by explaining the critical difference between home care and home health, breaking down real 2026 costs, navigating Medicare's coverage gaps, and showing how to combine paid services, family help, and home modifications into one workable plan.

By Editorial Team

new caregiver

experienced caregiver

long-distance caregiving

spousal caregiver

working caregiver

daily routines

medication management

personal hygiene

care coordination

first steps

ADLs

IADLs

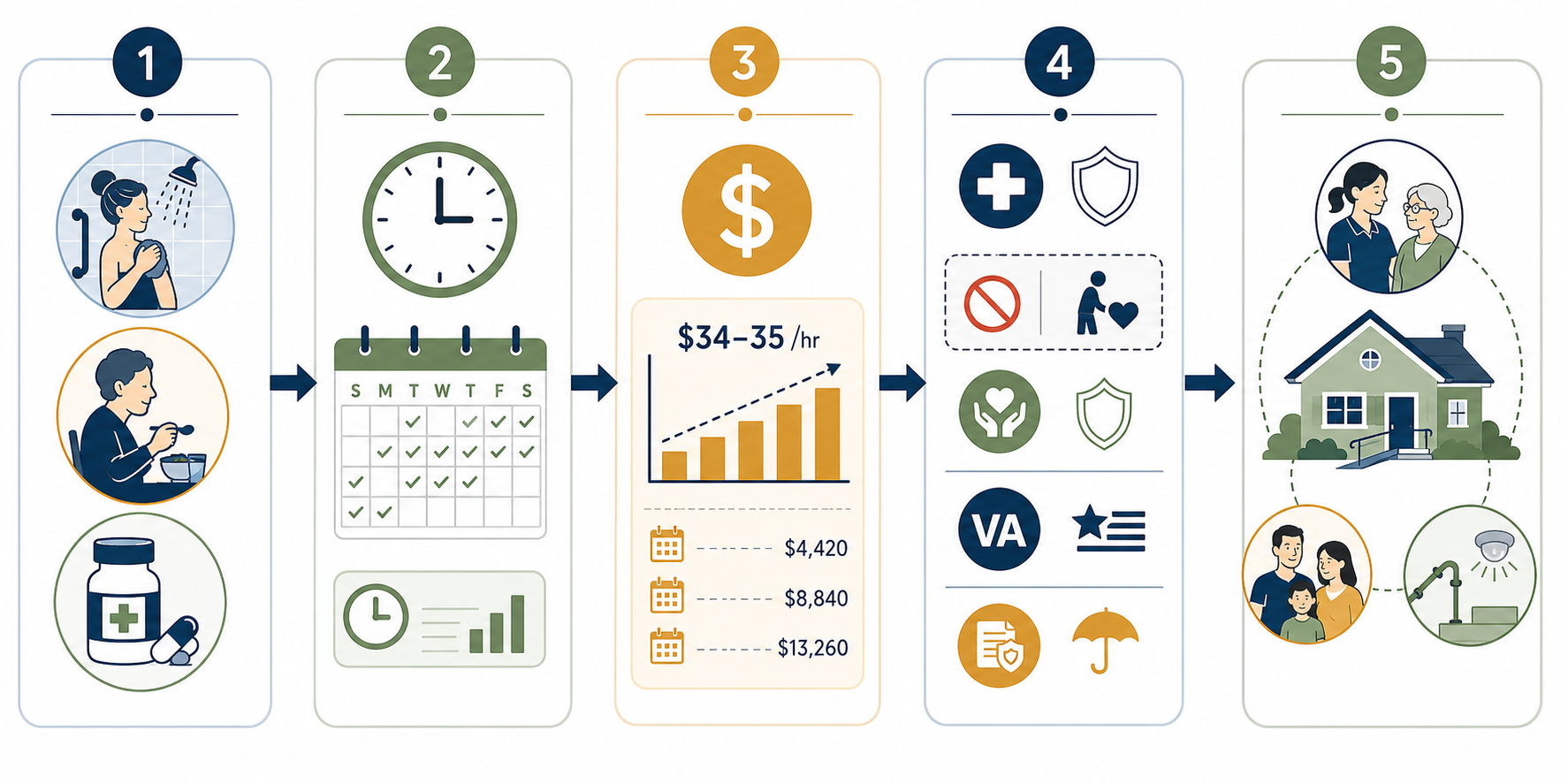

The first expensive mistake in an aging in place home care plan is using “home care” and “home health” as if they mean the same thing. They do not. Non-medical home care is the daily help many families are picturing: bathing, dressing, meal preparation, light housekeeping, transportation, companionship, supervision, and reminders. Skilled home health is clinical care ordered by a doctor, such as skilled nursing or therapy, usually after an illness, injury, surgery, or hospital stay.

That distinction controls the rest of the plan. If your parent needs help showering every morning and someone nearby while they make lunch, you are probably arranging non-medical home care. If your parent is homebound, under a physician’s plan of care, and needs intermittent skilled nursing, physical therapy, occupational therapy, speech therapy, or a qualifying home health aide visit, you may be looking at Medicare-covered home health services. Medicare’s home health benefit can cover skilled services when the rules are met, but it does not cover long-term personal care or 24-hour supervision as an ongoing custodial arrangement.[1]

This is why a family can call an agency, ask about “home health,” hear warm and helpful answers, and still be surprised later when the bill is private pay. The agency may provide excellent help. The question is whether the help is medical, intermittent, doctor-ordered, and covered under a benefit, or whether it is daily living support that someone has to pay for another way.

Why the home plan has to be specific

Most older adults are already living in the setting their families are trying to preserve. Pew Research Center reported in February 2026 that 93% of adults age 65 and older live in their own homes, and 60% would prefer to stay home with care rather than move if they needed help. The uneasy part is the confidence gap: among those who prefer that arrangement, only 37% think it is extremely or very likely to happen, and only 21% have long-term care insurance.[2]

That gap shows up at the kitchen table. A parent may say, “I’m fine,” while the adult children are quietly counting skipped meals, missed medications, laundry that has not been touched, and the new fear of the bathtub. Wanting to remain at home is not the problem. The problem is trying to protect that wish with vague promises instead of matching needs, hours, funding, people, and home conditions.

Sort the need before calling providers

Start with what your parent actually needs help doing, not with the name of a service. A practical assessment usually separates activities of daily living, often called ADLs, from instrumental activities of daily living, or IADLs. ADLs are the personal care tasks that affect basic safety and dignity. IADLs are the household and life-management tasks that let someone function at home.

Companion care, homemaker services, family task-sharing, transportation support, or care management

Clinical needs

Wound care, injections, therapy after hospitalization, monitoring after an acute change

Doctor-ordered skilled home health if eligibility rules are met

Supervision needs

Wandering risk, unsafe cooking, repeated falls, overnight confusion, inability to be alone safely

Longer home care shifts, family coverage, respite, home safety changes, or a broader senior services review

Write the list in plain language. “Needs help bathing” is more useful than “needs support.” “Forgets evening pills three times a week” is more useful than “medication issues.” If your family needs a structured way to have that conversation without turning it into an argument, an ADL checklist for an elderly parent can make the discussion less personal and more observable.

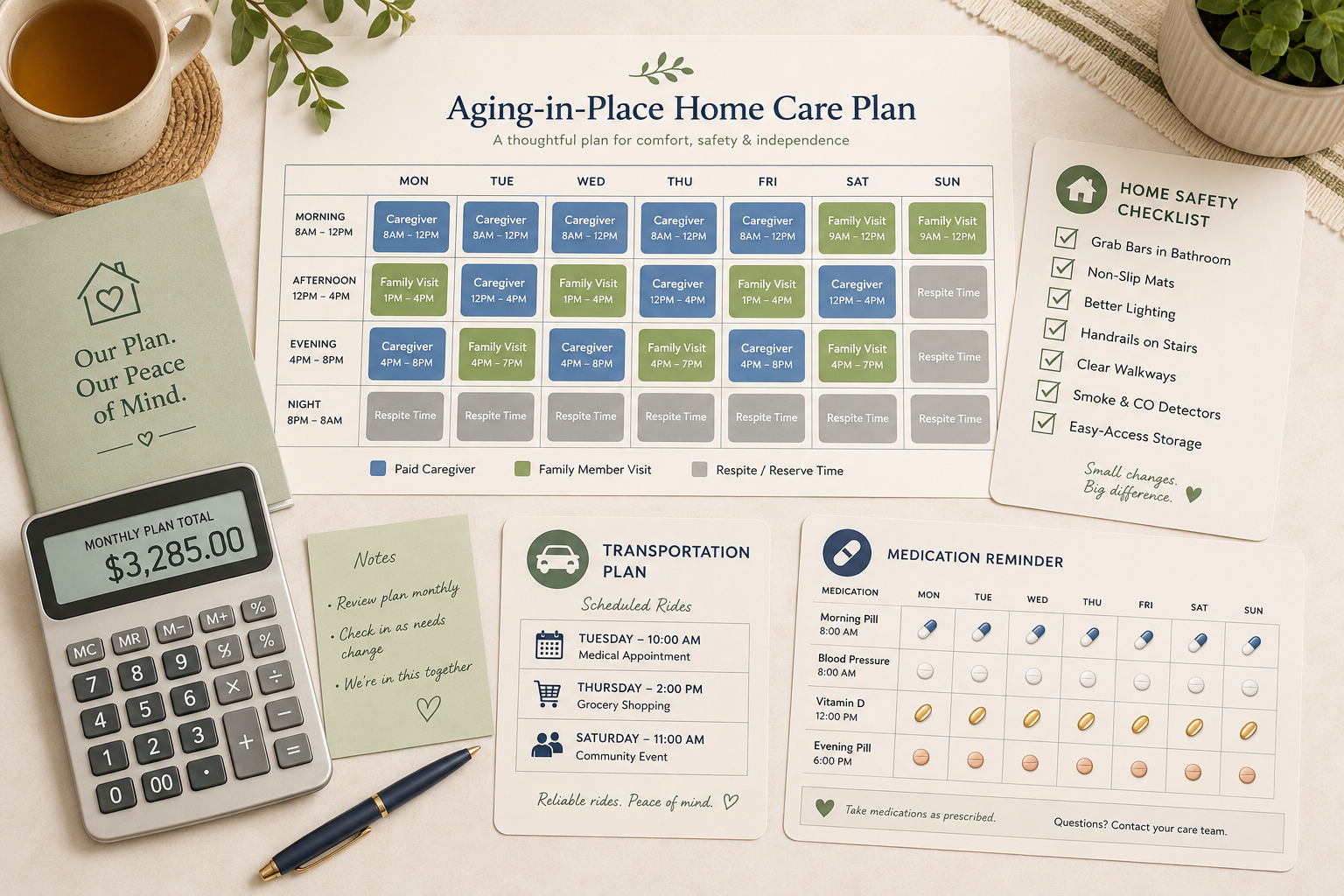

Turn the needs list into weekly hours

A home care budget does not begin with the monthly number. It begins with the calendar. If your parent needs help bathing, ask how many days a week, what time of day, and whether the caregiver also needs to prepare breakfast, change bedding, start laundry, or drive to an appointment while there. A one-hour need often becomes a three-hour shift because agencies and caregivers commonly schedule in blocks, and because real visits include arrival time, setup, cleanup, and notes.

For a first pass, build the week before you build the month:

Morning routine: bathing, dressing, breakfast, medication reminders, safe transfer out of bed.

Evening routine: dinner, medication reminders, toileting, getting ready for bed, fall prevention.

Household tasks: laundry, light housekeeping, groceries, trash, mail, pet care if relevant.

Supervision gaps: hours when your parent is unsafe alone, including overnight or early morning.

Then mark which hours must be paid, which can be covered by family, and which can be reduced by changing the environment. A grab bar will not replace a caregiver for someone who needs hands-on help transferring, but it may make a family visit safer. Grocery delivery will not solve loneliness, but it may remove a transportation errand from a paid shift.

Use the 2026 hourly cost as a planning number, not a promise

For 2026, national median home care estimates sit in the same uncomfortable range: A Place for Mom reports $34 per hour, while SeniorLiving.org, using CareScout data, reports $35 per hour.[3][4] The difference likely reflects different samples and methods. For family planning, the bigger point is that either number turns a modest-looking schedule into a serious monthly bill.

Care pattern

Example schedule

Approximate monthly cost at $34/hour

What this usually means

Occasional help

About 7 hours per week

$1,031

Errands, light housekeeping, a few companion or personal care visits

Moderate help

About 30 hours per week

$4,080

Regular help with morning or afternoon routines across much of the week

Extensive help

44 hours per week

$6,478

Near-daily coverage with longer shifts, but still not round-the-clock care

State prices can be materially different. SeniorLiving.org reports a 2026 range from $25 per hour in Mississippi to $44 per hour in South Dakota.[4] That is why a national median is useful for the first family conversation, but local quotes are necessary before anyone rearranges work schedules, signs an agency agreement, or assumes a parent’s savings will last a certain number of months.

The hard part is not only the hourly rate. It is the multiplication. Four hours a day, five days a week, may sound restrained until the family sees the monthly total. If costs are already moving faster than your parent’s income, use a deeper budgeting guide such as Home Care Costs Are Rising 7.9% Faster Than Inflation to test how long a plan can hold.

Test each need against each funding source

Do not ask, “Will insurance pay for home care?” Ask, “Which line on this weekly schedule might a benefit actually cover?” A shower visit, a wound-care visit, a ride to the grocery store, and overnight supervision may all happen at home, but they do not belong to the same payment category.

Funding source

What it may help with

Where families get surprised

Medicare home health

Intermittent skilled nursing, therapy, and certain home health aide services when eligibility rules are met

It is not ongoing custodial care, long-term personal care, or 24-hour supervision

Medicaid HCBS waivers

Home care and, in some states, home modifications for eligible low-income seniors

Eligibility, covered services, and waitlists vary by state

VA Aid & Attendance

Additional support for eligible veterans or surviving spouses who need help with daily activities

Eligibility depends on service, financial, and care-need rules

Long-term care insurance

Policy-defined home care benefits if the parent has an active policy and meets benefit triggers

Only a minority of older adults have this coverage, and policies differ

State or local programs

Limited homemaker, respite, transportation, meal, or caregiver support programs

Availability is local and often capped

Private pay and family contribution

The flexible backstop for hours not covered elsewhere

It can strain savings and sibling relationships if not written down clearly

Medicare deserves special caution because it is the benefit families most often assume will step in. Under Medicare’s home health rules, coverage is tied to being homebound, having a physician’s plan of care, and needing intermittent skilled care. The benefit can include skilled nursing, physical therapy, occupational therapy, speech therapy, and a home health aide when the conditions are met. It does not become a standing payment source for long-term help with bathing, meals, laundry, or someone staying all day so your parent is not alone.[1]

Choose the hiring model after the schedule is visible

Families often jump to the agency-versus-private-caregiver question too early. The better time to decide is after you know whether you need two short visits a week, a reliable morning shift every weekday, dementia supervision, transportation, or backup coverage when someone calls out.

Hourly minimums, rate changes, caregiver consistency, care plan updates, communication process

Private caregiver

Potentially more control over the relationship and schedule

Background checks, references, taxes, workers’ compensation, backup plan, written duties

Hybrid plan

Agency coverage for essential shifts plus family or private help for flexible tasks

Who coordinates the calendar, who handles gaps, and who has authority to change the plan

An agency can be worth the added structure when missed coverage would create a safety problem. A private caregiver may work well when the family has time to screen, manage, and create backup. Neither choice removes the adult child’s coordination role entirely. Someone still has to notice whether the care plan matches what is happening in the house.

Build one combined care plan, not three separate promises

The workable plan is usually not “hire a caregiver” or “the siblings will help.” It is a combined arrangement that says which tasks are paid, which tasks belong to family, which tasks can be simplified, and what happens when the usual person is unavailable.

A basic aging in place home care plan should name the following pieces in writing:

Paid care hours: days, times, tasks, hourly rate, monthly estimate, agency or caregiver contact.

Family responsibilities: visits, meals, bills, transportation, medical appointments, prescription pickup, social check-ins.

Medication support: who fills the organizer, who reminds, who watches for missed doses, who calls the prescriber.

Respite coverage: who covers the primary family caregiver’s breaks, travel, illness, or work conflicts.

Escalation rules: what triggers more hours, a doctor call, an emergency visit, or a broader care-setting discussion.

The family contribution needs the same honesty as the paid invoice. “I can stop by” is not a plan. “I can do groceries every Saturday morning and take Mom to the cardiologist if I have two weeks’ notice” is usable. If one adult child is handling the calendar, invoices, provider calls, medication questions, and parent resistance, name that role. Unpaid project management is still work.

Make the house part of the care plan

Home modifications should come after the care schedule is visible, because the right changes depend on where the real risk is. A parent who needs help stepping into the tub may need grab bars, a shower chair, a handheld showerhead, or a bathroom remodel. A parent who is safe bathing but unsafe on stairs needs a different plan. A parent who forgets the stove is on needs supervision and environmental controls, not just a new rail.

Walk through the home at the same times your parent struggles: morning bathroom routine, meal preparation, evening fatigue, nighttime toileting. Look for loose rugs, poor lighting, cluttered paths, missing handrails, high thresholds, hard-to-reach supplies, and furniture that makes transfers harder. Then decide whether the fix reduces paid hours, reduces injury risk, or simply makes family caregiving safer.

Some changes are inexpensive. Others are construction projects. For room-by-room budgeting, use a home modification cost guide for aging in place before assuming that the only choices are a few grab bars or a major renovation.

When the home plan may not be enough

Aging in place is not proven by keeping the address the same. It has to be safe enough, funded enough, and staffed enough to hold. If your parent needs continuous supervision, frequent overnight help, complex clinical care, or more hours than the family can pay for or provide, the responsible next step is not to pretend the calendar will somehow stretch.

That does not mean moving is automatically the answer. It means the comparison has changed. At that point, use a broader senior services decision framework to weigh home care against other settings with the same level of seriousness you brought to the home plan.

A real home care plan is not a wish, a provider list, or a promise that siblings will figure it out later. It starts by knowing whether you are arranging non-medical home care or skilled home health. From there, it becomes a matched plan: needs, hours, costs, funding, people, backup coverage, and a home that can support the care being asked of it.

References

Seven Things You Should Know About Medicare’s Home Health Care Benefit, National Council on Aging, link

Most older adults who live at home want to age in place, but they aren’t entirely confident they’ll get to, Pew Research Center, February 26, 2026, link

Comments

Join the discussion with an anonymous comment.