The State-by-State Benefits Fragmentation Navigator: A Structured Method for Cutting Through State-Level Confusion Across All Five Key Program Categories

The State-by-State Benefits Fragmentation Navigator: A Structured Method for Cutting Through State-Level Confusion Across All Five Key Program Categories

This guide provides a structured navigational framework for adult children caring for aging parents who are paralyzed by the dramatic state-level variations in Medicaid HCBS waivers, consumer-directed care, paid family leave, AAA services, and eligibility thresholds — helping you map your specific state's landscape and find the benefits your family is entitled to.

By Editorial Team

new caregiver

care coordination

first steps

Medicaid

Medicare

📄

A printable version of this guide is available. Use your browser's print function (Ctrl+P / ⌘P) to save or print.

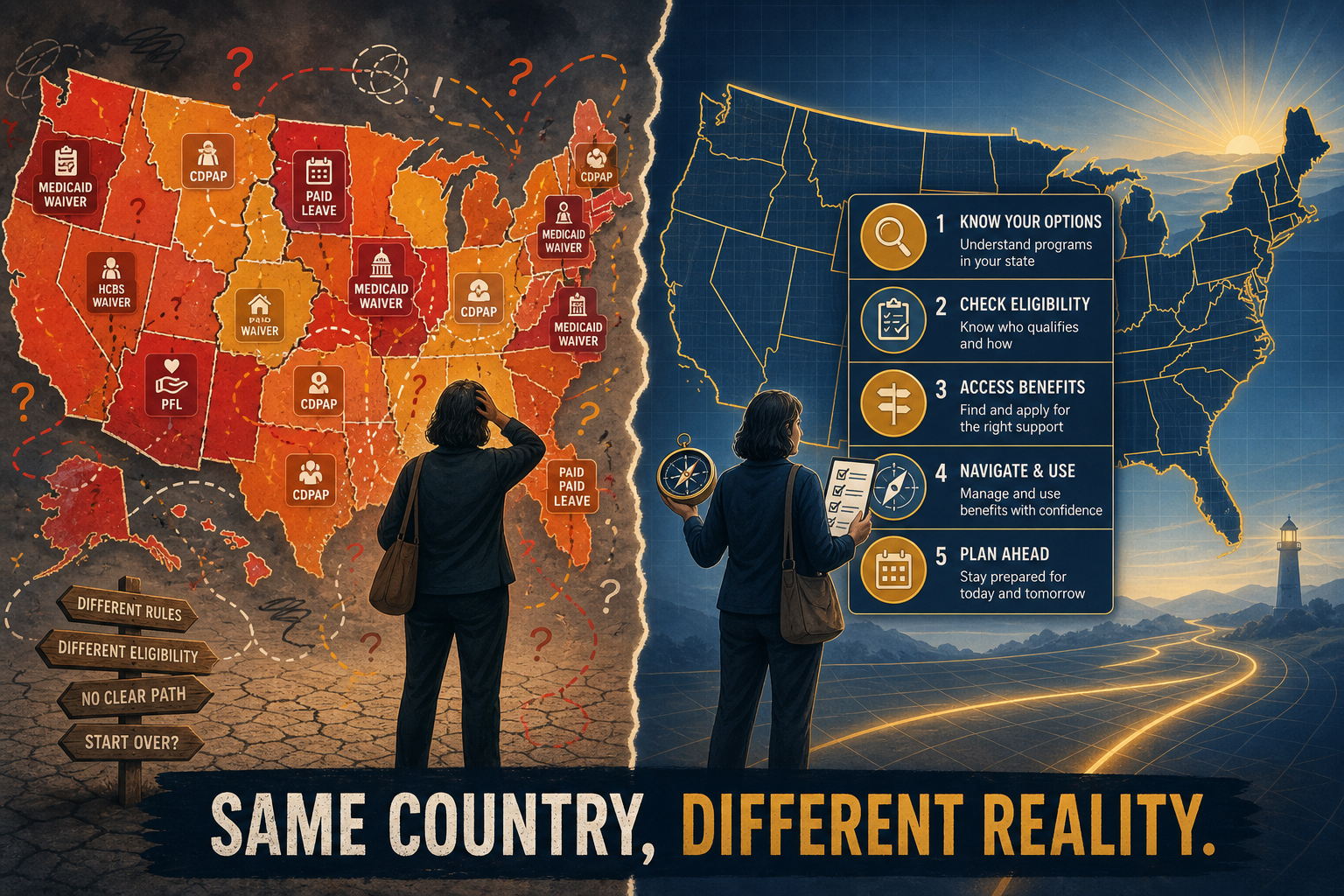

The same country produces completely different caregiving realities depending on which side of a state line you live on.

Why State-Level Fragmentation Is the Real Barrier (Not a Lack of Federal Programs)

If you have spent any time researching how to pay for a parent's home care, you have almost certainly encountered the same pattern: a federal program exists, it sounds promising, and then you discover the details depend entirely on which state your parent lives in. This is not a minor inconvenience. It is the primary reason an estimated $58 billion in benefits go unclaimed every year. The programs are not hidden. The money is not absent. What is missing is a structured way to navigate the dramatic state-level variations in program names, eligibility rules, waiting lists, and application pathways.

Consider the following contrast. Texas maintains an unscreened interest list for Medicaid home- and community-based services (HCBS) that contains 181,697 names, and the estimated wait for services ranges from 5 to 15 years. Arizona and California, by contrast, have no waiting list at all. Nebraska eliminated its entire developmental disability waiver waitlist in June 2025 after a focused $18 million investment over 15 months. A family in Texas and a family in Nebraska face the same federal Medicaid program but live in completely different universes of access.

The same fragmentation applies to consumer-directed care. New York's Consumer Directed Personal Assistance Program (CDPAP) has long been one of the most flexible in the country, allowing broad family hiring, though it is currently undergoing a major restructuring that consolidates roughly 700 providers into a single co-employer model. In other states, spouses and legally responsible relatives are explicitly excluded from being paid caregivers under certain program authorities. The rules do not just vary by state — they vary by which specific waiver or state plan authority a state uses.

This guide gives you a structured method — the Five State-Level Levers — for cutting through the confusion. Instead of listing federal programs you already know exist, it shows you exactly what to look for in your specific state and how to find it.

The Five State-Level Levers: A Decision Matrix for Navigating Benefits

Rather than trying to learn every detail about every program, focus on five key decision points — the levers that determine whether your parent qualifies, how much support they can receive, and how quickly services can start. Each lever answers a specific question and requires a specific action.

The Five State-Level Levers decision matrix. Each lever targets a specific barrier and gives you a clear next step.

Lever

Key Question for Caregivers

Primary State-Level Variable

Action Step

1: Medicaid HCBS Waivers

What is the waiver called in my state, and is there a waiting list?

Program name, waitlist length, screening practices

Find your state's waiver name and check the waitlist status

2: Consumer-Directed Care

Can I be paid as a family caregiver for my parent?

Allowed relatives, program authority type

Determine which relatives can be paid under your state's rules

3: Paid Family Leave

Does my state offer paid leave to care for a parent?

Mandatory vs. voluntary, weeks, wage replacement

Check if your state has a mandatory paid family leave program

4: AAA/ADRC Services

What local support is available through the Area Agency on Aging?

Local funding levels, service availability

Contact your local AAA for a personalized benefits check

5: Eligibility Thresholds

Does my parent's income and assets qualify for Medicaid HCBS?

Income limit, asset limit, home equity rules

Compare your parent's finances to your state's specific limits

Lever 1: Medicaid HCBS Waivers — Finding the Right Name and Facing the Waitlist Reality

Medicaid HCBS waivers allow states to use federal Medicaid funds to pay for home- and community-based services instead of institutional care. Every state that offers them (47 states use 1915(c) waivers, 15 use 1115 waivers) gives them a different name. North Carolina calls its primary waiver the "Innovations Waiver." Kentucky calls one of its waivers the "Michelle P. Waiver." If you search for "Medicaid HCBS waiver" in your state, you may find nothing — because the program has a completely different local name.

The more urgent problem is the waiting list crisis. According to the Kaiser Family Foundation's 2025 survey of state Medicaid programs (which included all states except Florida), 41 states maintain waiting lists or interest lists for HCBS waivers. Nationally, over 607,000 people are on these lists. The average wait time in 2025 was 32 months, down from 40 months in 2024, but this average masks enormous variation. People with intellectual and developmental disabilities (I/DD) wait an average of 37 months. Waivers for older adults and people with physical disabilities average 15 months. Waivers for autism average 63 months.

A critical distinction that many caregivers miss: some states screen applicants for eligibility before placing them on a waiting list, while others do not. Texas, Florida, South Carolina, Iowa, Oklahoma, and Oregon do not screen for eligibility, which means their waiting list numbers include many people who would not qualify for services if assessed. People in states that do not screen wait an average of 49 months, compared to 32 months in states that do screen. The Texas number of 181,697 on interest lists is real, but it is not a count of 181,697 people who would actually receive services.

State-by-state comparison of HCBS waiver waitlist realities. The variation is extreme, and the presence or absence of screening dramatically affects the numbers.

State

Waitlist Status

Key Detail

Texas

181,697 on unscreened interest lists

5–15 year estimated wait; no screening before placement

North Carolina

18,950 on Innovations Waiver Registry

9.5 year average wait; 20+ years for new registrants

Nebraska

Waitlist eliminated (June 2025)

$18M+ investment over 15 months; ~46% of families accepted waiver offers

New Mexico

DD waitlist effectively eliminated

"Super Allocation" initiative began 2021; FY2026 funds no-waitlist policy

Oklahoma

DD waitlist reduced from 13 years to ~1 year

Over 2,600 of 6,300 applicants now receiving services

Oregon

No waitlist since 2000

Lawsuit settlement eliminated the waitlist

Minnesota

DD waitlist eliminated in 2016

Structural redesign eliminated the waitlist

Kentucky

Michelle P. Waiver

Would take 168 years to serve everyone at current funding level

The good news: over 80% of people on waiting lists are eligible for personal care or other state plan services while they wait. Being on a waiver waitlist does not mean your parent receives no help — it means they cannot access the specific waiver-funded services. And 12 states reported at least one new waiting list in 2025 (20 waivers total), while 29 states reported an increase in total numbers. The crisis is not static; it is actively worsening in most states.

Lever 2: Consumer-Directed Care — Who Can Be a Paid Family Caregiver in Your State?

Consumer-directed care programs allow Medicaid enrollees to hire, train, and dismiss their own caregivers — including family members. All 50 states and the District of Columbia offer at least one consumer-directed long-term services and supports (LTSS) option. All responding states pay family caregivers under some circumstances. The question is not whether your state offers consumer-directed care — it is which relatives can be paid and under which program authority.

The key distinction is between two types of program authority. Under 1915(c) waivers, 44 states allow payments to legally responsible relatives (including, in some states, spouses). Under 1905(a)(24) state plan personal care, only 6 states allow payments to legally responsible relatives. The 1915(j) and 1915(k) authorities also allow legally responsible relatives to be paid in participating states.

Which program authority your state uses determines whether you can be paid as a family caregiver. The same state may use multiple authorities.

Program Authority

Can Legally Responsible Relatives Be Paid?

Number of States Using This Authority

1915(c) waivers

Yes (44 states allow it)

47 states offer HCBS through 1915(c) waivers

1905(a)(24) state plan personal care

No (only 6 states allow it)

33 states offer state plan personal care

1915(j) self-directed personal assistance

Yes (allows legally responsible relatives)

Available in participating states

1915(k) Community First Choice

Yes (allows legally responsible relatives)

10 states use 1915(k)

State examples illustrate the range. Connecticut's 1915(k) Community First Choice option allows hiring family members but excludes spouses and legally responsible individuals; roughly 30% of its approximately 4,000 participants engage family caregivers as personal care assistants. Florida's PDO program (under a 1915(b)/(c) waiver) allows legally responsible individuals including spouses to be paid; 7,841 of 51,848 HCBS enrollees participated as of June 2020. Virginia's CCC Plus waivers allow relatives other than spouses or parents of minor children to be reimbursed, though COVID-19 flexibilities temporarily allowed spouses and parents to be paid.

Oregon's Independent Choices Program (ICP) offers a different model entirely: it gives seniors a monthly cash benefit to hire caregivers, including spouses. This is not a Medicaid waiver program but a state-funded alternative that provides maximum flexibility.

Lever 3: Paid Family Leave — The 14-State Solution and What Everyone Else Gets

Paid family leave is the lever with the simplest state-by-state picture and the starkest divide. As of April 2026, only 14 states plus the District of Columbia have mandatory paid family leave programs. In these states, eligible workers can take paid time off to care for a seriously ill family member, including a parent. In the remaining 36 states, caregivers must rely on the federal Family and Medical Leave Act (FMLA), which provides 12 weeks of unpaid leave — and only if their employer qualifies (generally, employers with 50 or more employees) and the employee has worked at least 1,250 hours in the past year.

The mandatory state programs vary in duration and wage replacement. Most offer between 6 and 12 weeks of leave, with wage replacement ranging from 60% to 100% of the worker's regular pay, typically capped at a state-set maximum weekly benefit. Several states are phasing in new programs: Maryland's program is expected to take effect in 2027/2028, and Virginia's in 2028/2029. The landscape will continue to expand, but for now, the majority of American caregivers have no paid leave option.

The paid family leave landscape as of April 2026. Most caregivers still have no paid leave option.

Category

Number of States

What Caregivers Get

Mandatory paid family leave

14 states + DC

6–12 weeks paid leave; 60–100% wage replacement

Unpaid FMLA only

36 states

12 weeks unpaid leave (employer must qualify)

Phasing in programs

Maryland (2027/2028), Virginia (2028/2029)

Programs not yet operational

For caregivers in the 36 states without paid leave, the practical reality is that taking time off to care for a parent often means using accrued sick or vacation time, taking unpaid leave, or reducing work hours — all of which carry financial consequences. This is one reason why the state-level benefits navigator is so important: if your state does not offer paid leave, the other four levers become even more critical for finding financial support.

Lever 4: AAA/ADRC Services — The 'No Wrong Door' System and Its Uneven Reality

The Older Americans Act (OAA) funds a national network of over 600 local Area Agencies on Aging (AAAs) that provide community-based social services: home-delivered and congregate meals, transportation, caregiver support, chronic disease prevention, and the Long-Term Care Ombudsman program. In FY 2023, Title III programs (which account for nearly three-quarters of OAA funding) served more than 12 million individuals. The network serves roughly 1 in 6 older adults.

The "No Wrong Door" system — formally the Aging and Disability Resource Centers (ADRCs) — is designed to be a single entry point where families can get information about all available long-term services and supports, regardless of which program they ultimately use. In theory, you call one number and get connected to everything. In practice, AAA funding and service levels vary dramatically by state and local area. Some AAAs have robust caregiver support programs with trained counselors, respite vouchers, and support groups. Others can only provide information and referral due to limited budgets.

The ACL (Administration for Community Living) released over $1 billion in FY 2025 OAA funding, though this funding was initially withheld by the Trump administration before being released. The HHS has proposed dissolving the ACL and integrating its functions into a new Administration for Children, Families, and Communities (ACFC), which could affect how OAA programs are administered in the future. Trump administration restructuring has included layoffs of 10,000 HHS employees.

Lever 5: Eligibility Thresholds — The $2,000 vs. $130,000 Asset Limit Reality

Even if your state has a waiver with no waiting list and a consumer-directed program that allows family caregivers, your parent must still meet financial eligibility requirements. This is where the difference between states can determine whether a middle-class family qualifies for any help at all.

For Medicaid HCBS, the typical income limit is $2,982 per month (300% of the federal SSI benefit rate). Most states use this standard. The asset limit, however, varies enormously. In most states, the asset limit for an individual is $2,000. In California, the asset limit is $130,000. This is not a minor difference — it is the difference between a family with modest home equity and savings qualifying for services or being completely excluded.

State-by-state variation in Medicaid HCBS eligibility thresholds. The asset limit range of $2,000 to $130,000 determines whether middle-class families can qualify.

State

Income Limit (Typical)

Asset Limit (Individual)

Key Note

Most states

$2,982/month

$2,000

Standard federal minimum

California

$2,982/month

$130,000

Highest asset limit in the country

18 states with higher limits

Varies

Varies

Have increased income or savings limits beyond federal minimums

Alabama

SSI level only

SSI level only

Only state that does not extend optional coverage

Eighteen states have increased income or savings limits for Medicare beneficiaries beyond the federal minimums. All states except Alabama extend optional coverage to low-income adults with disabilities or people ages 65 and older with income above SSI limits. Forty-seven states offer a Medicaid Buy-In program for working adults with disabilities, which allows higher income and asset limits for people who are employed.

Between 2024 and 2025, few eligibility changes occurred, but 12 states increased the personal needs allowance for institutional care (South Dakota had the largest increase, from $60 to $100 per month). The broader point: eligibility is not static. States can and do adjust their thresholds, and the 2025 reconciliation law is estimated to reduce federal Medicaid spending by $911 billion over a decade, which could lead to further state-level changes.

Building Your State Profile: Five Questions Every Caregiver Can Answer in an Afternoon

You do not need to become a Medicaid expert. You need to build a profile of your specific state's landscape. These five questions correspond to the five levers and can be researched in a single focused afternoon. Use your state's Medicaid website, the local AAA, and the resources linked in this guide as your primary sources.

What is the name of my state's primary HCBS waiver for older adults or people with physical disabilities, and does it have a waiting list? Search your state Medicaid agency's website for "HCBS waiver," "home and community-based services," or "waiver services." Look for the specific program name and any information about enrollment caps or waiting lists.

Under my state's consumer-directed care program, can I be paid as a family caregiver? Check whether your state uses a 1915(c) waiver, 1915(j), 1915(k), or state plan personal care. Then look for the specific rules about which relatives can be hired. The NASHP report on paying family caregivers is an excellent starting point.

Does my state have a mandatory paid family leave program, and if so, what are the eligibility rules? Check the Bipartisan Policy Center's state tracker or your state's labor department website. If your state does not have a program, check whether your employer offers voluntary paid family leave as a benefit.

What is the phone number or website for my local Area Agency on Aging, and what services do they offer? Use the Eldercare Locator (eldercare.acl.gov) or call 1-800-677-1116 to find your local AAA. Ask specifically about caregiver support programs, respite care, and benefits counseling.

What are my state's specific income and asset limits for Medicaid HCBS? Check your state Medicaid agency's website for the current income and asset limits for HCBS waivers. Compare these to your parent's financial situation. If your parent's assets exceed the limit, ask about Medicaid planning options.

The Five State-Level Levers framework: a structured method for cutting through state-level confusion across all five key program categories.

Putting It All Together: Where State-Benefit Navigation Fits in Your Caregiving Timeline

State-level benefit navigation is not a one-time task. It is a recurring process that should align with your broader caregiving decision-making timeline. The five levers framework is designed to be revisited as your parent's needs change, as state policies shift, and as new programs become available.

Initial assessment (first 30 days): Build your state profile using the five questions above. Contact your local AAA. Check your state's paid family leave status. This gives you a baseline understanding of what is available.

Application phase (next 60-90 days): Apply for the appropriate Medicaid HCBS waiver. If there is a waiting list, get on it immediately — time on the list counts. Explore consumer-directed care options. Apply for paid family leave if available.

Ongoing monitoring (every 6-12 months): Recheck your state's waiting list status, eligibility thresholds, and any new programs. State budgets change, new waivers are created, and waiting lists can be reduced or eliminated.

Trigger events: Revisit the five levers whenever your parent's health status changes significantly, when they move to a new state, or when you hear about state policy changes that could affect benefits.

The core thesis of this guide is simple: the information you need exists. The programs exist. The funding exists. What has been missing is a structured method for finding what applies in your specific state. The Five State-Level Levers framework gives you that method. Use it to cut through the fragmentation, build your state profile, and claim the benefits your family is entitled to.

Comments

Join the discussion with an anonymous comment.