Help for Elderly and Disabled Adults at Home: A Family Guide to In-Home Care, HCBS, and Daily Living Support (HCBS)

clinicalA practical guide for family caregivers navigating the patchwork of in-home services and payment options — from personal care and home health to meal delivery and transportation — so their loved one can age in place safely.

Introduction: The Challenge of Aging in Place

The vast majority of older adults and people with disabilities want to remain in their own homes as they age. Staying at home preserves independence, familiar routines, and community connections. But the reality is that most families encounter a confusing patchwork of services and payment sources when they try to make that happen. One program covers skilled nursing for a few weeks after a hospital stay. Another might pay for help with bathing and dressing — but only if you meet strict income limits. A third offers free meal delivery, but only in certain zip codes.

This guide is designed for family caregivers who need a clear, practical map of the in-home services available and how to pay for them. We focus specifically on daily living support — personal care, home health, meal delivery, transportation, and companion services — and the major payment pathways that make them accessible. If you are looking for a broader overview of federal and state benefits programs, our Elder Care Assistance Programs guide covers that territory. Here, we stay focused on the services that help someone stay at home.

Types of In-Home Help: What Services Are Available?

In-home support is not a single service. It is a spectrum of assistance that ranges from a nurse changing a wound dressing to a volunteer sitting with your loved one for two hours so you can run errands. Understanding the categories helps you match the service to the actual need — and to the right payment source.

| Service Type | What It Covers | Who Typically Provides It | Common Payment Source |

|---|---|---|---|

| Personal care / ADL assistance | Bathing, dressing, toileting, eating, transferring, grooming | Home health aides, personal care aides | Medicaid HCBS, state plan personal care, private pay |

| Home health / skilled nursing | Wound care, medication management, physical therapy, speech therapy | Registered nurses, licensed practical nurses, therapists (Medicare-certified agency) | Medicare Part A/B (short-term), Medicaid, private insurance |

| Homemaker / chore services | Light housekeeping, laundry, meal preparation, grocery shopping | Homemaker aides, chore service providers | Medicaid HCBS, Older Americans Act, private pay |

| Meal delivery | Nutritious meals delivered to the home (often lunch and dinner) | Meals on Wheels, local senior nutrition programs | Older Americans Act, donations, private pay |

| Transportation | Rides to medical appointments, grocery stores, senior centers | Volunteer driver programs, Medicaid non-emergency transport, public paratransit | Medicaid (for appointments), Older Americans Act, some free volunteer programs |

| Friendly visitor / companion | Social visits, phone check-ins, light companionship (usually under 2 hours) | Volunteer programs, senior centers, faith-based organizations | Often free or low-cost; not covered by Medicare or most insurance |

| Respite care | Short-term relief for the primary caregiver — from a few hours to several weeks | Home care agencies, adult day centers, hospice providers | Medicaid HCBS, some LTC insurance, Medicare hospice (up to 5 days), private pay |

| Adult day care | Supervised daytime activities, meals, and social engagement in a group setting | Adult day centers (licensed by state) | Medicaid HCBS, private pay; Medicare does not pay |

The National Institute on Aging provides detailed descriptions of these services, including contact information for national referral networks. For example, Meals on Wheels America can be reached at 888-998-6325, and the National Adult Day Services Association at 877-745-1440.

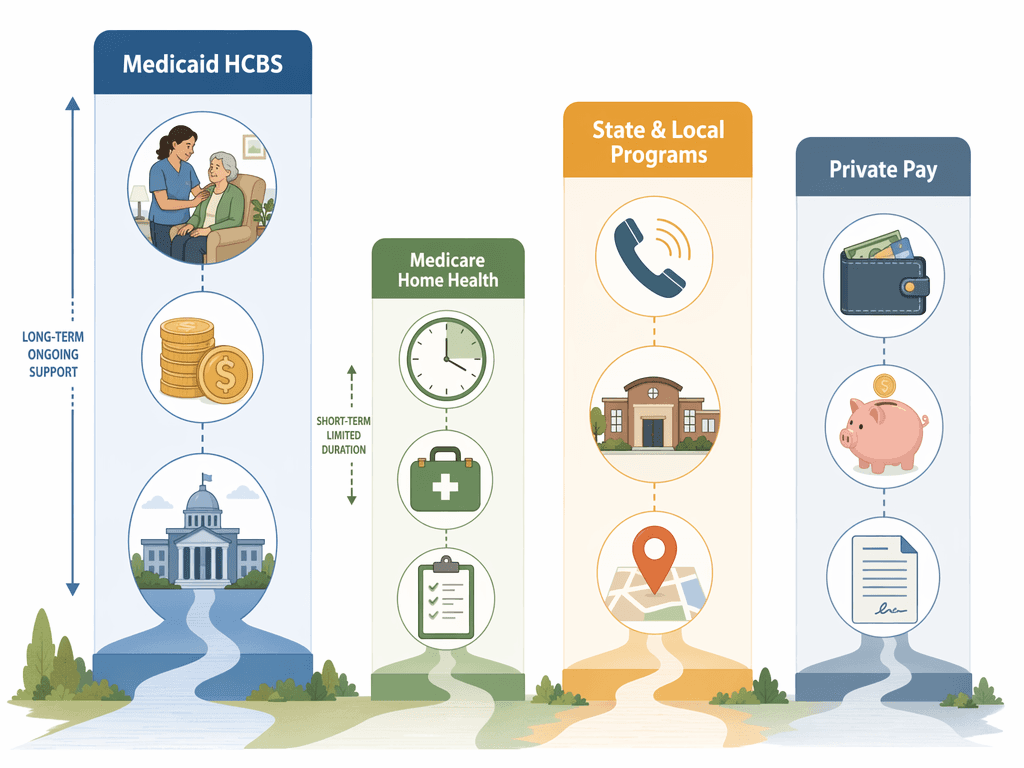

Medicaid HCBS: The Primary Payer for Long-Term Home Care

If your loved one needs ongoing help with daily activities and has limited income and assets, Medicaid is likely the most important program to understand. According to the Kaiser Family Foundation (KFF), Medicaid is the primary payer for home care in the United States, covering two-thirds of all home care spending in 2022. About 4.5 million people receive Medicaid-covered home care annually.

Medicaid home and community-based services (HCBS) are delivered through several pathways. Every state offers at least one option, but the specific programs and eligibility rules vary significantly.

| HCBS Pathway | Number of States Offering It | Key Features |

|---|---|---|

| 1915(c) waivers | 47 states | Target specific populations (e.g., 65+, physical disabilities, ID/DD); states can limit enrollment and maintain waiting lists |

| 1115 waivers | 14 states | Allow broader demonstration projects; may cover services not available under 1915(c) |

| State plan personal care | 34 states | An entitlement — no waiting list; must be offered to all eligible individuals in the state |

| Community First Choice | 10 states | Enhanced federal matching rate for states that offer attendant services and supports |

A critical detail: 46 states have HCBS waivers specifically targeting people ages 65 and older or those with physical disabilities. This means that even if your state does not offer a broad personal care state plan, there is likely a waiver program that can help. However, many waivers have waiting lists, and eligibility is determined at the state level.

It is also worth noting that the policy landscape is shifting. The 2025 federal reconciliation law enacted Medicaid funding reductions and a 10-year moratorium on certain eligibility simplification rules. As of June 2026, the downstream effects on state optional HCBS pathways are still unfolding, per KFF's April 2026 analysis. Families should check for the most current state-level information.

Medicare Home Health: Short-Term, Skilled, and Limited

A common misconception is that Medicare covers long-term in-home personal care. It does not. The Medicare home health benefit is designed for short-term, skilled care provided by a Medicare-certified agency. To qualify, the person must be homebound, need skilled nursing or therapy services on an intermittent basis, and have a doctor's plan of care.

Medicare covers services such as:

- Skilled nursing care (wound care, medication management, catheter changes)

- Physical therapy, occupational therapy, and speech-language pathology

- Medical social services

- Part-time or intermittent home health aide services (only when you are also receiving skilled care)

Medicare does not pay for 24-hour-a-day care, meal delivery, transportation, or personal care (like bathing and dressing) when that is the only help needed. For a detailed breakdown of what changed in 2026 and what families need to know, see our Medicare Home Health Care in 2026 FAQ.

State and Local Programs: Area Agencies on Aging, Older Americans Act, and More

Beyond Medicaid and Medicare, a network of state and local programs fills important gaps. These programs are often less well-known but can provide critical support, especially for families who do not qualify for Medicaid.

- Area Agencies on Aging (AAAs): Local offices that provide information, referrals, and direct services (nutrition, transportation, caregiver support) funded by the Older Americans Act. Find yours through the Eldercare Locator (800-677-1116).

- Older Americans Act services: Includes congregate and home-delivered meals (Meals on Wheels), transportation, legal assistance, and the National Family Caregiver Support Program (NFCSP), which offers counseling, support groups, and respite.

- Aging and Disability Resource Centers (ADRCs): One-stop entry points for long-term services and supports, serving people of all ages and disabilities. They can help you understand Medicaid HCBS eligibility and connect you to local programs.

- Adult Day Care: Supervised daytime programs that provide social activities, meals, and some health services. Less expensive than in-home care or nursing homes. Medicaid may pay if the person is eligible for HCBS.

- Respite care: Short-term relief for family caregivers. The ARCH National Respite Locator (703-256-2084, archrespite.org) can help you find local options. Medicare covers up to 5 consecutive days of respite in a facility for those receiving hospice care.

The National Institute on Aging notes that most private health insurance does not cover respite, though some long-term care insurance policies may. The Eldercare Locator (800-677-1116) is the primary national entry point for older adults; for younger adults with disabilities, ADRCs serve a broader age range.

Private Pay and Long-Term Care Insurance: When You Pay Out of Pocket

For many families, private pay is a reality — either because they do not qualify for Medicaid, or because they need services that public programs do not cover. Understanding the costs and alternatives is essential for planning.

| Payment Option | What It Covers | Key Considerations |

|---|---|---|

| Private pay (out of pocket) | Any service you choose — personal care, homemaker, companion, home health | Costs vary widely by region and level of care; see our guide on in-home care costs after a fall for real-world examples |

| Long-term care insurance | Personal care, home health, adult day care, respite (depending on policy) | Must have a policy in place before care is needed; policies vary in what they cover and when benefits begin |

| Medicare Advantage in-home support benefits | Some plans offer supplemental benefits like meal delivery, transportation, or in-home support services | Not all plans offer these; benefits are plan-specific and may have limits; see our Medicare Advantage in-home support benefits guide for details |

| Supplemental Security Income (SSI) | Cash assistance for low-income individuals who are 65+ or disabled | 2026 FBR is $994/month for an individual — generally not enough to cover home care costs, but can supplement other income |

| Social Security Disability Insurance (SSDI) | Cash benefits for disabled workers | 2026 SGA is $1,690/month for non-blind disability; benefits are modest and not intended to cover home care |

For a deeper look at what families actually pay for recovery care after a fall, read our article on In-Home Senior Care Cost After a Fall. And if your loved one has a Medicare Advantage plan, check our guide on Medicare Advantage In-Home Support Benefits in 2026 to see if their plan offers supplemental in-home support.

How to Find and Vet In-Home Care Providers

Once you know what type of service you need and how you will pay for it, the next step is finding a reliable provider. This process requires careful vetting, especially when the care involves entering your loved one's home.

- Use Medicare Care Compare: If you are using Medicare home health, this tool lists Medicare-certified home health agencies and provides quality ratings. Only agencies that are Medicare-certified can bill Medicare for services.

- Check state regulatory agencies: Most states license home health agencies and home care agencies. Your state's health department or department of aging can tell you if a provider has had complaints or violations.

- Verify certification and insurance: Ask if the agency is licensed, bonded, and insured. For home health, confirm Medicare certification. For personal care, ask about training and background checks for aides.

- Conduct interviews: Ask about the agency's hiring process, how they match aides to clients, what happens if an aide is sick, and how they handle emergencies.

- Check references: Ask for references from current or past clients. A reputable agency should be willing to provide them.

- Check the Better Business Bureau: Look for complaints and resolution history.

For a step-by-step walkthrough of the entire process — from assessing needs to hiring and managing a home health aide — see our guide on How to Set Up In-Home Nursing Care for an Elderly Parent. It covers the practical decisions families face, including how to evaluate agencies and what questions to ask during interviews.

When to Bring in a Geriatric Care Manager

For families navigating complex medical, financial, and care coordination challenges, a geriatric care manager — now often called an Aging Life Care Manager — can be invaluable. These professionals are typically nurses, social workers, or gerontologists who specialize in assessing needs, coordinating services, and providing ongoing oversight.

A geriatric care manager can:

- Conduct a comprehensive assessment of your loved one's physical, cognitive, and social needs

- Develop a care plan and coordinate services across multiple providers

- Navigate payment options, including Medicaid HCBS eligibility and Medicare coverage

- Monitor care quality and adjust the plan as needs change

- Provide crisis intervention and family mediation

The National Institute on Aging notes that geriatric care managers charge by the hour and are not covered by Medicare or Medicaid. The Aging Life Care Association (520-881-8008) can help you find a qualified professional in your area.

Checklist: Evaluating Your Loved One’s In-Home Care Needs

Use this checklist as a starting point. It will help you organize your thoughts, identify the most pressing needs, and take the next steps with confidence.

- Identify ADL and IADL needs: Which daily activities does your loved one need help with? Bathing, dressing, toileting, eating, transferring (ADLs)? Or medication management, transportation, meal preparation, housekeeping (IADLs)?

- Check Medicaid HCBS eligibility: Contact your local ADRC or AAA to find out if your loved one qualifies for Medicaid HCBS waivers or state plan personal care. Income and asset limits vary by state.

- Explore Medicare home health: If your loved one recently had a hospitalization or needs skilled nursing or therapy, ask their doctor about a Medicare-certified home health agency.

- Contact the Eldercare Locator (800-677-1116): This is the fastest way to find your local AAA and learn about Older Americans Act services like meal delivery, transportation, and caregiver support.

- Research private pay options: If public programs are not available or have waiting lists, get cost estimates for private-pay home care in your area. See our guide on in-home care costs after a fall for typical ranges.

- Interview providers: Use the vetting steps above to evaluate agencies. Ask about certification, insurance, background checks, and how they handle emergencies.

- Consider a geriatric care manager: For complex situations, a care manager can save time and reduce stress. They charge by the hour and are not covered by Medicare or Medicaid.

- Review long-term care insurance: If your loved one has a policy, review what it covers and how to file a claim. Some policies cover in-home personal care and respite.

- Plan for the future: Needs change over time. Reassess every few months and adjust the care plan as necessary.

See This Term in Context

- Skilled Nursing Facility (SNF): What It Is and When Medicare Covers It

A skilled nursing facility (SNF) is a Medicare-certified setting for short-term post-hospital skilled nursing and rehabilitation — not a permanent nursing home — and Medicare Part A covers it only under five specific conditions. This glossary entry explains the eligibility rules, 2026 cost structure, the observation-status trap, and how to appeal a wrongful denial.

- Original Medicare vs. Medicare Advantage in 2026: A Caregiver's Decision Guide for Choosing the Right Coverage for a Parent

This guide helps adult children compare Original Medicare and Medicare Advantage for a parent in 2026. It covers the core trade-offs, a side-by-side cost and coverage comparison, the critical Medigap lock-out risk, 2026 market changes, and scenario-based guidance to make an informed choice.

- Senior Health Services by Care Need: Matching Services to Your Parent's Actual Situation

A scenario-based guide for crisis-driven caregivers. Instead of organizing services by facility type, this guide helps you match the right service — home health, adult day care, respite, PACE, or memory care — to your parent's specific situation, whether it's a recent fall, a dementia diagnosis, or caregiver burnout.

Also related: In-Home Senior Care Cost After a Fall, Medicare Home Health Care in 2026, How to Set Up In-Home Nursing Care for an Elderly Parent, Medicare Advantage In-Home Support Benefits in 2026, Long-Term Care for the Elderly

Comments

Join the discussion with an anonymous comment.