Taking Care of Elderly Parents: The Real Cost to Your Health, Career, and Finances — and What You Can Do About It

Reviewed: 2026-06-30

Taking Care of Elderly Parents: The Real Cost to Your Health, Career, and Finances — and What You Can Do About It

This article reveals the documented health, financial, and career impacts of caring for an aging parent — and offers evidence-based strategies to protect yourself before burnout and financial strain become crises.

By Editorial Team

early-stage Alzheimer's

middle-stage Alzheimer's

late-stage Alzheimer's

wandering

sundowning

agitation

repetitive questioning

sleep disturbances

eating refusal

dementia communication

safety planning

hospice and end-of-life

BPSD

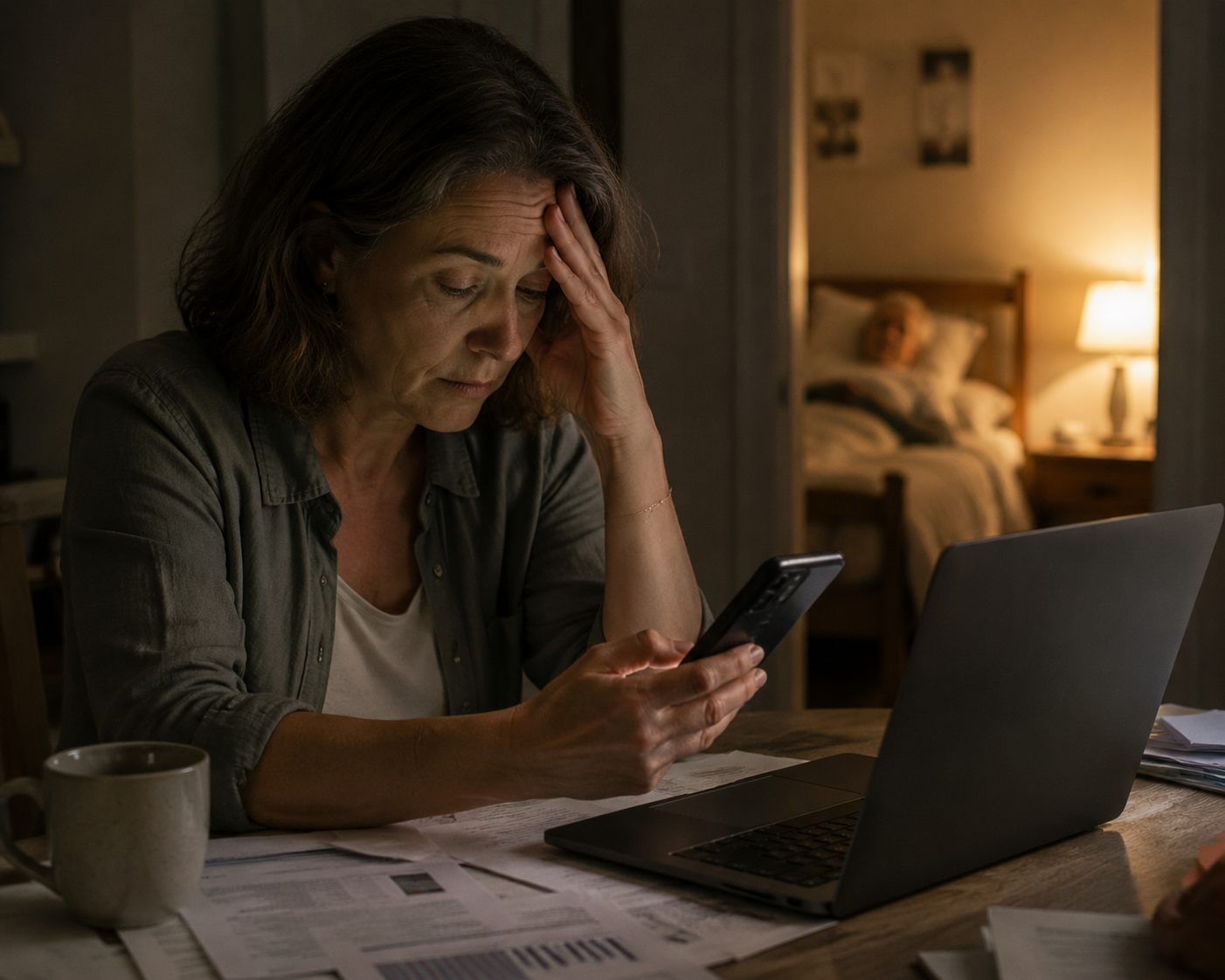

Taking care of elderly parents often starts with a reasonable promise: a few appointments, a medication pickup, a week of staying close after a fall. Then the calendar changes shape. Work calls move around doctor visits. Sleep gets interrupted by worry or by a phone that might ring. A household budget that once had ordinary tension begins carrying gas, supplies, missed hours, and paid help when no one else can step in.

If that private arrangement has begun to feel like a second unpaid job, the data does not treat that as an overreaction. In A Place for Mom’s 2025 survey conducted with Morning Light Strategy, 75% of family caregivers reported stress or anxiety at least monthly, 67% regularly had trouble sleeping, 47% said their physical health declined, and 42% reported emotional strain or burnout weekly.[1] Those numbers matter because they put words around what many adult children only notice after they are already exhausted: the body usually registers the load before the family has formally admitted how much care is being provided.

The Pattern Is Bigger Than One Tired Week

The first hard question is usually not policy-related. It is more personal: Is this normal, or am I failing at something other people handle better? The most honest answer is that the strain is common, measurable, and unevenly distributed. Pew Research Center’s 2026 report, based on a nationally representative survey conducted in September 2025, found that women caregivers were more likely than men caregivers to report negative effects on emotional well-being, 47% versus 30%, and physical health, 38% versus 26%.[2]

That gender gap rarely arrives as one explicit family vote. It more often builds through small assumptions: one daughter has the flexible job, one sister knows the medication list, one spouse is better at calming Mom, one person is already checking the portal. Competence becomes the reason more work lands on the same person. By the time anyone says, “You’re just better at this,” the schedule may already be structured around that unpaid labor.

The national scale is large enough to sound abstract. AARP and the National Alliance for Caregiving estimated 63 million family caregivers in the United States and valued unpaid family care at $873 billion per year.[3] That figure is useful because it shows how much the care system depends on families. But the more immediate warning signs are smaller: the missed sleep, the reduced hours, the quiet spreadsheet where “temporary” care has turned into a household expense category.

Health Strain Usually Shows Up Before Anyone Calls It Burnout

Caregiver strain is often described as emotional, but it is not only emotional. Regular sleep disruption changes how a person thinks, works, drives, listens, and recovers. A caregiver who is awake at 2 a.m. because a parent wandered, fell, called repeatedly, or simply might need help is not starting the next workday from the same place as a rested colleague. When two-thirds of caregivers in one survey say sleep is regularly difficult, that is not a niche inconvenience; it is a systems problem being absorbed bedroom by bedroom.[1]

This is where articles about “self-care” often become too thin. A bath, a walk, or an app may help for an evening, but they do not answer who covers a parent with constant-care needs, who can afford respite, or what happens when the caregiver has already used every flexible favor at work. For a deeper look at the warning signs that tend to appear before full collapse, see Caregiver Burnout: Patterns, Warning Signs, and What the Evidence Says About Recovery.

The practical concern is not whether a caregiver feels stressed in a vague way. It is whether the arrangement is now producing predictable health consequences: chronic sleep loss, anxiety that does not reset, back or joint strain from transfers, missed medical appointments for the caregiver, or the feeling of being unable to stand down even when another adult is present. Those are not character flaws. They are signs that the care plan is using the caregiver’s body as its backup system.

Work Is Often the First Place the Cost Becomes Visible

The career impact rarely begins with quitting. It begins with leaving early, declining travel, turning down a project, taking unpaid time, or answering care calls during hours that used to belong to paid work. A Place for Mom reported that 35% of caregivers reduced work hours and 11% quit jobs entirely; the same source reported average lost income of $21,500 per year and that 37% said their finances worsened.[1]

Those figures describe a progression many families recognize too late. First, caregiving consumes slack time. Then it consumes sleep. Then it consumes work flexibility. Eventually, the caregiver may start trading income, advancement, benefits, or retirement savings for a care arrangement no one priced honestly at the beginning.

Pressure point

What it can look like in daily life

Why it matters

Sleep

Night calls, monitoring, anxiety after falls or confusion

Fatigue makes work, driving, decision-making, and patience harder

Hours

Late arrivals, early departures, unpaid leave, fewer shifts

Income can fall before the family recognizes a financial crisis

Short-term coverage can become long-term economic loss

Household support

One person handles portals, appointments, bills, and emergencies

The “default” caregiver becomes harder to replace over time

This is also where sandwich-generation strain becomes less of a label and more of a daily routing problem. In the A Place for Mom data, 53% of caregivers held paid jobs, 48% were sandwich-generation caregivers, and 40% were single, widowed, separated, or divorced without a partner’s support.[1] A person can be deeply committed to a parent and still have no spare adult in the house, no backup driver, and no easy way to replace a missed paycheck.

If you are caring for a parent while also raising children or supporting young adults, the pressure is not just emotional multitasking. It is competing dependency at fixed times of day: school pickup, medication windows, shift start times, specialist appointments, meal support, and the unpredictable crisis that ignores all of them. The Sandwich Squeeze is a useful next read if the hardest part of caregiving is that two generations need you at once.

Why Caregiver Counts Vary, and Why That Should Not Distract You

Caregiving research does not always use the same doorway. Some studies count caregivers for adults above a certain age. Others include broader disability support, different care-recipient ages, or different minimum care tasks. That is why one report can estimate tens of millions of family caregivers while another, using another national data set and age threshold, reports a smaller but still sharply growing group.

For example, Johns Hopkins researchers reported that the number of family caregivers supporting older adults increased from 18.2 million to 24.1 million between 2011 and 2022, a 32% rise, and that care hours increased by about 50% over that period.[4] AARP and the National Alliance for Caregiving’s broader 2025 estimate of 63 million caregivers captures a different measurement frame.[3] The important point for a working adult child is not to force those figures into one number. It is to recognize that multiple data sources point in the same direction: more families are providing more care, and the load is not evenly buffered.

The Risk Factors That Turn Hard Care Into Crisis Care

Not every caregiver faces the same risk. Some families have siblings nearby, money for paid help, a parent who can still manage many daily tasks, or an employer that treats eldercare as a real responsibility. Others have none of that. Mayo Clinic’s caregiver-stress guidance names several risk factors that make strain more likely, including living with the care recipient, providing constant care, feeling alone, having little choice about becoming a caregiver, and lacking professional guidance.[5]

Those risk factors work well as a screening lens because they move the question away from guilt and toward logistics. A caregiver who lives with a parent with high overnight needs is not facing the same situation as a sibling who visits on Saturdays. A caregiver who never chose the role but became the only available person needs a different plan than someone with a broad family rotation. A caregiver making medical, financial, and housing decisions without professional guidance is carrying risk that love alone cannot organize.

If you live with your parent, plan for relief inside the home, not only occasional time away.

If your parent needs constant care, treat backup coverage as essential infrastructure, not a favor.

If you feel alone, name specific tasks that another person or service can own.

If you had little choice, do not wait for resentment to become the first proof that the plan is unfair.

If no professional is helping you interpret options, seek guidance before a hospital discharge or fall forces rushed decisions.

This does not mean every family can redistribute care cleanly. Some siblings are unavailable, unsafe, estranged, ill, far away, or financially stretched themselves. The point is not to pretend there is always a neat division of labor. The point is to identify which part of the arrangement is most likely to fail first, then protect that part before it breaks.

Prevention Starts With the Part of the Load Most Likely to Collapse

A protective plan does not have to solve the whole caregiving arrangement at once. It has to reduce the next predictable failure. For one caregiver, that is sleep. For another, it is work attendance. For another, it is the lack of anyone who can stay with Dad during a medical appointment for Mom. The right first move depends on where the current care plan is borrowing from the future.

Use Respite Before It Becomes an Emergency Word

Respite is often discussed too late, after the caregiver is already depleted. It can mean an adult day program, in-home help, a trained volunteer, a paid aide, a family rotation, or a short residential stay, depending on the parent’s needs and local availability. The practical question is not whether you “deserve” a break. It is whether the care arrangement has any safe substitute when you are sick, working, sleeping, or at the end of your capacity.

Start small if that is all the family can manage: two reliable hours each week, one backup driver, one afternoon at an adult day program, one sibling assigned to prescription refills. Then write it down. A respite plan that lives only in a group text often disappears when the next crisis arrives. For options to compare, see Respite Care Options for Family Caregivers.

Talk to Work Before the Job Damage Is Irreversible

Because 35% of caregivers in the A Place for Mom survey reduced work hours and 11% quit jobs, waiting until work is already unraveling is risky.[1] The earlier conversation is usually less dramatic and more useful: ask what leave, flexibility, remote-work, schedule-shift, employee assistance, or reduced-load options exist before attendance problems define the conversation for you.

Keep the request concrete. Instead of explaining the entire family story, identify the work impact and the proposed adjustment: a later start on appointment days, a predictable remote day after overnight care, intermittent leave for medical visits, or a temporary schedule while home care is arranged. If the employer has forms, policies, or HR language, use them. Caregiving is personal, but workplace protection often depends on documentation.

Look for Money That Is Easy to Miss

Financial strain is not only the big-ticket cost of assisted living or memory care. It is also co-pays, home modifications, transportation, supplies, missed shifts, unpaid leave, meals, legal documents, and the invisible cost of becoming the family administrator. If finances are worsening, do not rely on memory. Track the recurring expenses and the lost work time for one month. That record can change the family conversation from “I’m overwhelmed” to “Here is what this arrangement is costing.”

Then check whether any benefits or programs apply: Medicaid home- and community-based services, VA benefits, local aging services, disease-specific grants, life insurance options, tax-related documentation, or employer supports. Not every program will fit, and eligibility rules can be narrow. But families often miss help because they look only after a crisis. Hidden Money for Family Caregivers is a practical place to begin that search.

Bring in Guidance When Decisions Become Too Specialized

Professional guidance is not a luxury when the care needs are changing quickly. A geriatric care manager, social worker, Area Agency on Aging, elder law attorney, dementia clinic, discharge planner, or benefits counselor may each solve a different problem. The useful question is not “Who can fix everything?” It is “Who can explain the next decision clearly enough that I do not make it alone at midnight?”

Dementia Caregivers Should Check the GUIDE Model

Not every caregiver is caring for someone with dementia, and not every support program applies to every family. But for dementia caregivers, one federal program is important enough to check directly. The Centers for Medicare & Medicaid Services launched the GUIDE Model in July 2024, and the model is scheduled to run through 2032.[6]

The GUIDE Model is designed for Medicare beneficiaries with dementia and includes caregiver skills training, care navigation, a 24/7 support line, and up to $2,500 per year in respite services for eligible beneficiaries.[6] That last qualifier matters. This is not a universal respite benefit for all family caregivers. It is condition-specific, tied to dementia, and available through participating GUIDE providers.

If your parent has Alzheimer’s disease or another dementia diagnosis, ask the diagnosing clinician, health system, Medicare plan, or local dementia program whether a GUIDE participant is available. If no one recognizes the term, use the CMS GUIDE Model page as the reference point and ask who in the system handles dementia care navigation. The goal is not to become an expert in a federal model. The goal is to find out whether your family can stop building dementia care from scratch.

What to Do This Week, Before the Next Crisis Decides for You

The most useful first step is to identify the biggest current risk, not the most emotionally charged one. If sleep is failing, start with overnight coverage or a safety plan. If work is failing, start with HR, leave, schedule protection, and documentation. If money is failing, start with expense tracking and benefit screening. If decision-making is failing, start with professional guidance. If dementia is involved, check GUIDE Model eligibility before assuming respite is entirely out of reach.

For families already in the middle of a sudden decline, fall, discharge, or safety scare, a short triage tool may be more useful than a long planning process. The 72-Hour Caregiver Checklist can help sort immediate tasks from decisions that can wait.

Caregiving risk is predictable enough to plan around. Early action is not selfish; it is the difference between a care plan that can bend and one that breaks the person holding it together. Name the risk, get one other support in place, and make the next decision before exhaustion makes it for you.

Comments

Join the discussion with an anonymous comment.