Many families assume Medicare will cover their parent's home care needs, but Medicare home health is limited to skilled, intermittent, homebound care only. This guide maps every funding option — Medicare, Medicaid, VA benefits, long-term care insurance, and private pay — with eligibility rules and 2026 costs to help you build a realistic payment plan.

By Editorial Team

new caregiver

experienced caregiver

long-distance caregiving

spousal caregiver

working caregiver

daily routines

medication management

personal hygiene

care coordination

first steps

ADLs

IADLs

The hard part of paying for senior home healthcare is that families usually mean two different things with one phrase. One parent may need a nurse to check a wound after surgery. Another may need someone there every morning to help with bathing, breakfast, laundry, and medication reminders. Those sound equally necessary at the kitchen table. To Medicare, Medicaid, an agency scheduler, and an insurance claims department, they are not the same kind of care.

That distinction matters because home care is no longer a small add-on expense. AARP reported that home care costs rose 7.9% from May 2025 to May 2026, and estimated that 30 hours a week of home care costs about $4,416 a month, or $51,480 a year, more than double the average annual Social Security benefit of about $23,700.[1] A Place for Mom’s 2026 proprietary cost survey puts the national median for non-medical home care at $34 an hour, with state medians ranging from $25 an hour in Mississippi to $44 an hour in South Dakota.[2]

Those are planning numbers, not promises. Local agency rates, minimum shifts, weekend premiums, and care needs can change the bill quickly. But they are useful enough to show why “Will Medicare pay?” is the wrong first question. The first question is: what kind of help is actually needed?

Start by separating medical care from daily help

For payment purposes, “home health” usually means medically necessary skilled care at home: skilled nursing, physical therapy, occupational therapy, speech-language pathology, and certain home health aide services tied to that skilled plan of care. Medicare’s home health benefit sits in this lane.

“Home care” usually means non-medical help with daily living: bathing, dressing, toileting, meal preparation, light housekeeping, transportation, supervision, and companionship. This is the help many families need most often and for the longest period. It is also the help Medicare usually does not pay for when it is the only need.

If your parent is still in the “What kind of help is this?” stage, it is worth pausing there before calling payers. A clear care category prevents the expensive mistake of building a weekly schedule around a benefit that was never designed to cover it. For a fuller terminology breakdown, see Home Health vs. Home Care vs. Hospice vs. Respite.

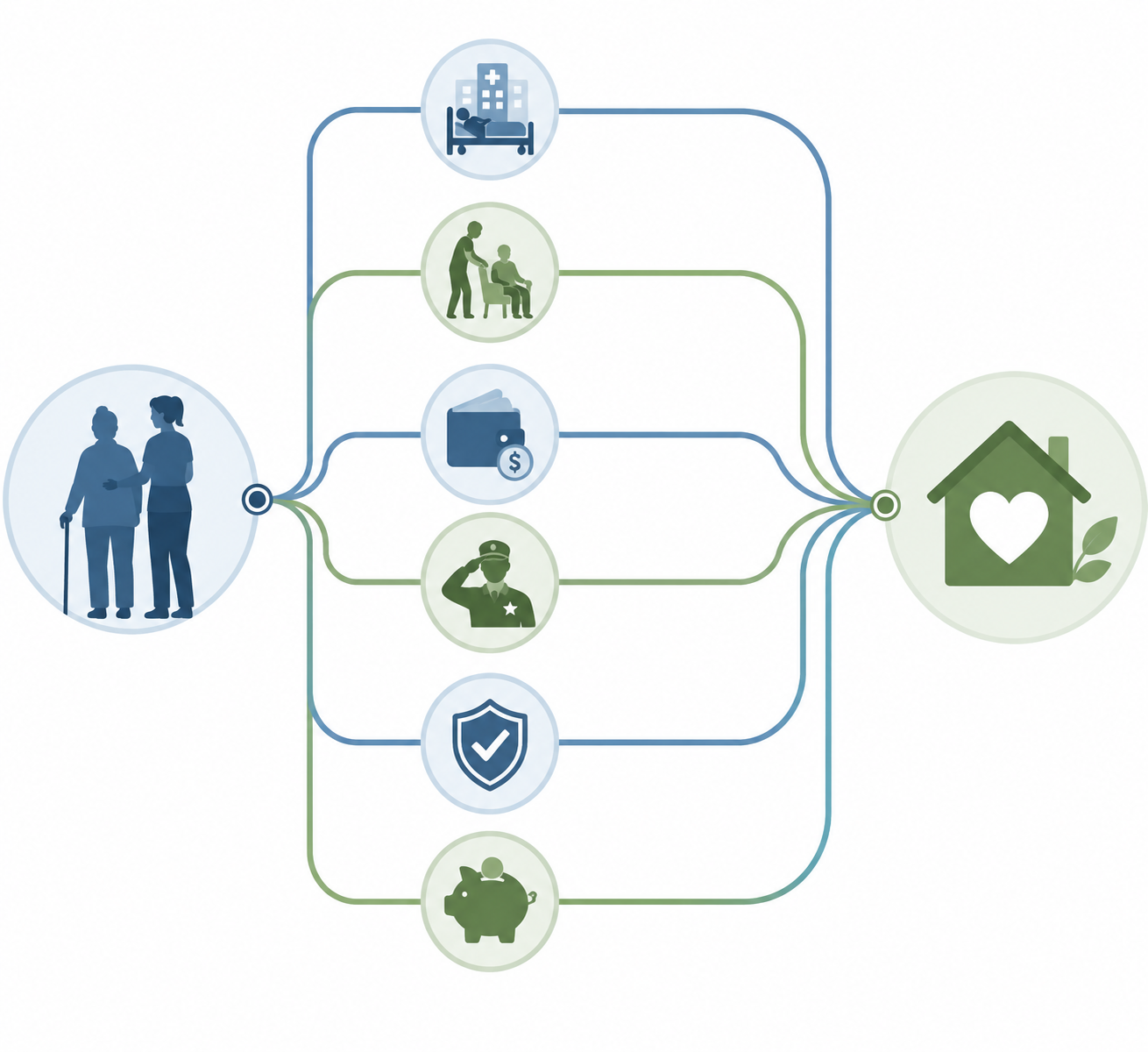

The 2026 payment map

Most families end up with a blended answer. One payer may cover a short period of skilled care. Another may help if income, assets, military service, or an insurance policy qualifies. Private pay often fills the rest.

Funding source

What it may pay for at home

Who may qualify

How to access it

Common gap

Original Medicare

Part-time or intermittent skilled home health services ordered by a doctor through a Medicare-certified agency

A beneficiary who is homebound and needs skilled nursing or therapy under Medicare rules

Doctor certifies the need and the agency accepts the case under Medicare

Does not cover 24/7 care, meal delivery, or custodial care alone[3]

Medicare Advantage

Medicare-covered home health, and sometimes plan-specific supplemental benefits

Plan member who meets Medicare rules and any plan requirements

Call the plan, confirm network agency rules, prior authorization, and supplemental benefits

Benefits vary by plan and can be limited by network, authorization, or service caps

Medicaid and HCBS waivers

Home health, personal care, and home- and community-based services depending on the state

People who meet state financial and functional eligibility rules

Apply through the state Medicaid agency or waiver program

Asset limits, state variation, and waitlists can delay or limit help

VA benefits

Some home-based care, homemaker/home health aide services, respite, or pension-related support for eligible veterans

Veterans, and sometimes surviving spouses, depending on service, health, financial, and program rules

Contact VA health care, a VA social worker, or an accredited veterans service officer

Eligibility and available services depend on VA program enrollment and local availability

Long-term care insurance

Personal care at home if the policy covers home care and benefit triggers are met

Policyholder who meets the policy’s definition of benefit eligibility

Review the policy, elimination period, daily or monthly benefit, and claim documentation

Older policies may have limits, waiting periods, inflation issues, or strict documentation rules

Private pay

Non-medical home care, extra hours, uncovered supervision, agency minimums, and gaps between benefits

Anyone who can pay the agency or caregiver

Hire through an agency or private caregiver, with written rates and responsibilities

Costs continue as long as care continues

Tax deductions

Possible medical expense deductions for qualifying care costs

Taxpayers who meet IRS rules and itemization thresholds

Ask a tax professional and keep care invoices, care plans, and medical necessity documentation

A deduction is not upfront funding and may not help families who do not itemize

What Medicare home health actually covers

Medicare is the benefit most likely to be misunderstood because it does cover home health care in some situations. The problem is the boundary. Medicare says a patient must be under the care of a doctor or allowed practitioner, have a plan of care that is regularly reviewed, need part-time or intermittent skilled nursing care or qualifying therapy, be homebound, and use a Medicare-certified home health agency.[3]

That is a medical benefit, not a general household support benefit. Medicare states that home health services do not include 24-hour-a-day care at home, meals delivered to the home, homemaker services such as shopping or cleaning when that is the only care needed, or custodial and personal care when that is the only care needed.[3]

This is where many invoices begin. A parent may truly need help bathing and dressing. The family may be right that the help is necessary for safety. But if the need is custodial care alone, Medicare’s home health benefit is not the payer.

Skilled care means a licensed clinical need

A skilled need is care that requires a nurse or therapist, such as wound care, injections, certain disease monitoring and teaching, physical therapy after a fall or surgery, speech therapy after a stroke, or occupational therapy to regain daily function. A home health aide may be part of the Medicare-covered plan, but usually because the aide service supports the skilled plan of care.

Medication reminders alone are usually not the same as skilled nursing. Meal preparation alone is not skilled care. Standing by while someone showers may be essential, but essential is not the same as Medicare-covered.

Intermittent does not mean all day

Medicare describes covered home health as part-time or intermittent. Medicare rules allow a combined limit of up to 8 hours a day and 28 hours a week for skilled nursing and home health aide services, with up to 35 hours a week possible for a short period when medically necessary. That is not a promise that every eligible person receives those hours. The plan still has to be medically necessary, ordered, provided by a Medicare-certified agency, and accepted under the rules.

The practical point is simple: Medicare home health can help a parent recover or stabilize at home after a qualifying medical event. It is not designed to staff a daily care schedule indefinitely.

Homebound does not mean bedbound

Medicare’s homebound requirement does not mean a person can never leave the house. It generally means leaving home takes considerable and taxing effort, and absences are limited or for specific reasons such as medical care. The exact determination can be fact-specific, so families should not self-deny or self-approve this point from a checklist. Ask the doctor and the Medicare-certified agency to document how the standard applies.

Certification, recertification, and written notices matter

Medicare home health is not approved once and then left alone. Medicare home health generally works on a 60-day certification cycle, and care ends when the patient no longer meets medical eligibility. Families should treat each certification period as a checkpoint: what skilled need remains, what goals are documented, and what services are being reduced or stopped?

If a Medicare home health agency reduces or stops services, families should ask for the written notice and appeal information. Medicare materials describe the Home Health Change of Care Notice, often called the HHCCN, for certain changes in care, and the Advance Beneficiary Notice, or ABN, before services are provided that Medicare may not cover.[3] These forms are not junk paperwork. They are the paper trail that tells you whether the family is about to become the payer.

Medicare Advantage can add benefits, but check the plan before scheduling care

Medicare Advantage plans must cover Medicare-covered home health services when the member meets Medicare’s rules, but the plan may use network agencies, prior authorization, care management, and plan-specific procedures. Some plans also advertise supplemental in-home supports. Those extras can be useful, but they are not a national Medicare guarantee.

Before counting on a Medicare Advantage plan for home help, call the plan and ask narrow questions: Is this service covered under the medical home health benefit or as a supplemental benefit? Does it require prior authorization? Which agencies are in network? How many visits or hours are approved? What happens if the agency says the care is custodial?

The answer to those questions should be written down with the date, representative name or ID if available, and any authorization number. A friendly “yes, home care is included” is not enough to build a Monday-through-Friday schedule.

Medicaid may help with long-term support, but the answer is state-specific

Medicaid is often the most important public payer for long-term services and supports, including some care at home. But it is also the place where national generalizations become dangerous. Medicaid home health, personal care, and Home- and Community-Based Services waivers vary by state, and eligibility usually includes both financial rules and functional need.

A waiver may help pay for personal care, adult day services, respite, homemaker support, or other services that keep a person at home instead of in an institution. But waivers can have enrollment caps, waitlists, service limits, and assessment requirements. Asset and income rules also differ by state and by eligibility pathway.

The useful move is not to ask, “Does Medicaid cover home care?” The useful move is to ask your state Medicaid office or Area Agency on Aging: Which Medicaid home care or HCBS waiver programs serve older adults in this state? What are the income and asset rules? Is there a waitlist? What functional assessment is required? Can services begin after hospital discharge, or only after full approval?

Do not transfer assets, spend down accounts, or change ownership of property based on a general article. Medicaid planning can affect eligibility and penalties, and the right answer is state-specific. This is where an elder law attorney, benefits counselor, or state Medicaid specialist earns the phone call.

VA benefits are worth checking early for veterans and surviving spouses

If the older adult is a veteran, or the surviving spouse of a veteran, VA pathways should be checked before the family assumes private pay is the only option. Depending on eligibility and local availability, VA programs may include homemaker and home health aide services, respite, adult day health care, home-based primary care, or pension-related support that can help with care costs.

This is not one benefit with one simple test. Service history, discharge status, health needs, income and assets, VA enrollment, disability status, and local program capacity can all matter. Start with a VA social worker if the person is already in VA care, or an accredited veterans service officer if the family is unsure where to begin.

Long-term care insurance can be useful, if the policy actually covers home care

A long-term care insurance policy is not the same as Medicare, and it should not be left in a drawer until the first agency invoice arrives. Many policies cover care at home, but the details decide whether the benefit is usable: the elimination period, daily or monthly benefit amount, benefit period, inflation protection, covered provider type, and the trigger for benefits.

Most families should look for the policy’s definition of benefit eligibility. Many policies require either help with a certain number of activities of daily living or a cognitive impairment that requires supervision. The policy may require an assessment, care plan, invoices, caregiver credentials, or agency documentation before paying.

Coordination with Medicare matters. Medicare might cover skilled home health after a hospitalization or medical decline, while the long-term care policy may cover custodial home care if the policy triggers are met. One does not automatically replace the other. Ask the insurer how claims are coordinated when Medicare-covered home health and private-duty home care happen in the same month.

Private pay is often the gap filler, so price it like a real bill

Private pay is not a failure of planning. It is often the predictable result of needing daily non-medical help that no public program has agreed to cover. The planning mistake is treating it as a vague backup instead of a monthly number.

Using the 2026 national median of $34 an hour, 10 hours a week is about $1,473 a month before any agency minimums or surcharges. Thirty hours a week is about $4,416 a month, which matches AARP’s planning estimate.[1][2] If a parent needs morning and evening help seven days a week, the schedule can grow faster than the family expects.

Before signing an agency agreement, ask for the hourly rate, minimum shift length, weekend and holiday rates, cancellation rules, mileage or transportation charges, care plan fees, deposit requirements, and what happens if the caregiver calls out. If hiring privately, families also need to think through payroll taxes, workers’ compensation rules, background checks, backup coverage, and supervision. Those issues are administrative, but they become care issues the first morning no one arrives.

Tax deductions may soften the cost, but they do not fund care upfront

Some home care costs may qualify as medical expenses for tax purposes if they meet IRS rules, especially when care is medically necessary or connected to a care plan. But a tax deduction is not the same as a benefit card, insurance payment, or waiver slot. It may help after the fact, and only if the taxpayer’s situation makes the deduction usable.

Keep invoices, care plans, medical necessity letters, and proof of payment. Then ask a tax professional how the rules apply to the person paying, the person receiving care, and any dependency or itemization issues. This is another place where a confident general answer can be expensive if the household facts do not match.

Match the situation to the likely payer

The cleanest way to avoid a coverage surprise is to work from the care situation, not from the program name. The same parent may move through several of these categories in one year.

If the main need is...

Start here

Then check

Do not assume

Short-term skilled care after a hospitalization, fall, surgery, wound, stroke, or medical decline

Doctor-ordered Medicare home health through a Medicare-certified agency

Medicare Advantage authorization rules if enrolled in a plan; long-term care policy if custodial help is also needed

That Medicare will cover meal prep, supervision, or daily bathing after the skilled need ends

Ongoing help with bathing, dressing, meals, laundry, transportation, or companionship

Private-pay home care quotes and a realistic weekly schedule

Medicaid HCBS waiver eligibility, VA benefits, long-term care insurance

That calling it senior home healthcare makes it Medicare-covered

Low income or limited assets plus functional need

State Medicaid office, Area Agency on Aging, or benefits counselor

HCBS waivers, personal care programs, waitlists, estate recovery and state-specific rules

That Medicaid rules are the same in every state

Veteran or surviving spouse in the household

VA health care team, VA social worker, or accredited veterans service officer

Homemaker/home health aide services, respite, adult day care, pension-related support

That VA help is automatic or identical in every location

That premiums paid for years mean every home care invoice will be reimbursed

Unsafe home layout plus care needs

Care plan and home safety assessment

Separate funding for home modifications, grants, loans, or tax treatment

That home care benefits automatically pay for ramps, bathroom changes, or stair lifts

The last row matters because families often discover two bills at once: people-help and house-help. If the home itself needs changes, see How to Pay for Aging in Place Home Modifications. Keep that funding search separate from the weekly aide schedule so one delay does not hide the other.

Build the payment plan in writing before increasing hours

The U.S. Department of Health and Human Services has estimated that 56% of adults turning 65 from 2021 through 2025 will need long-term services and supports during their lifetime.[4] That does not mean every person will need paid home care, and it does not say which payer will cover any specific family. It does mean the need is common enough that families should not treat the payment plan as an afterthought.

A workable home care payment plan usually has five written pieces:

Care classification: skilled medical care, non-medical personal care, supervision, homemaker help, transportation, respite, or a combination.

Medicare status: whether the doctor has ordered home health, whether the person is homebound, whether the agency is Medicare-certified, and what the written plan of care includes.

Public-benefit checks: Medicaid and HCBS waiver screening in the correct state, plus VA screening if military service may apply.

Insurance review: any long-term care policy, Medicare Advantage plan documents, prior authorization rules, and claim requirements.

Private-pay backup: the weekly schedule the family can afford if no program covers the custodial hours.

The private-pay backup should not be left blank while applications are pending. Medicaid waiver approval can take time. VA benefits can take time. Long-term care insurance claims can take time. Medicare home health can end when the skilled need ends. The parent still needs breakfast, a shower, and safe transfers while those systems move at their own pace.

Questions to ask before agreeing to a home care schedule

Before adding hours or signing an agency agreement, ask the questions that separate covered care from wishful thinking:

Is this service skilled home health, non-medical home care, or both?

If Medicare is expected to pay, who ordered the care, what skilled need is documented, and is the agency Medicare-certified?

If services are reduced or denied, what written notice will the agency provide, and what appeal rights apply?

If Medicare Advantage is involved, has the plan approved the agency, service type, and number of visits or hours?

If Medicaid may apply, which state program or waiver is being considered, and is there a waitlist?

If the family is paying privately, what is the monthly cost at the proposed weekly schedule, including minimums and surcharges?

There may be no single program that pays for the exact care plan a family wants. That is frustrating, but it is better to know before the schedule starts. Classify the care need, verify Medicare eligibility in writing, check Medicaid and VA pathways if they may apply, review any long-term care policy, and price the private-pay hours that no program has agreed to cover.

Comments

Join the discussion with an anonymous comment.