How to Pay for Elderly Home Care: Medicare, Medicaid, VA Benefits, and Out-of-Pocket Options Explained

Last reviewed: — Review date is particularly important for Medicare coverage, device specifications, and clinical guidance, which change frequently.

The Real Cost of Home Care in 2026: What Families Face

Before you can figure out how to pay for home care, you need a clear picture of what it actually costs. In 2026, the national median rate for a non-medical home health aide is $34 to $35 per hour, according to data from A Place for Mom and SeniorLiving.org. That number varies dramatically by where your parent lives — from a low of around $23 per hour in Louisiana to a high of $44 per hour in South Dakota.

To make this concrete, here is what those hourly rates translate to in monthly spending at the national median, depending on how many hours of help your family needs each week:

| Hours of Care per Week | Estimated Monthly Cost (at $34/hr) |

|---|---|

| 7 hours (daily check-in) | $1,031 |

| 15 hours (part-time) | $2,208 |

| 30 hours (half-time) | $4,416 |

| 44 hours (near full-time) | $6,478 |

These figures assume you hire through an agency, which typically charges 20 to 30 percent more than hiring a private caregiver directly. The trade-off is that agencies handle background checks, training, scheduling, and backup coverage — a meaningful consideration when you are coordinating care from a distance.

The core problem this article addresses is simple: the payment landscape for home care is fractured across at least seven different funding sources — Medicare, Medicaid, VA benefits, long-term care insurance, private pay, community programs, and tax deductions — and most families miss at least one source they may qualify for simply because the information is scattered across different agencies. This guide consolidates every pathway into a single decision framework so you can stop hunting for fragments and start building a workable plan.

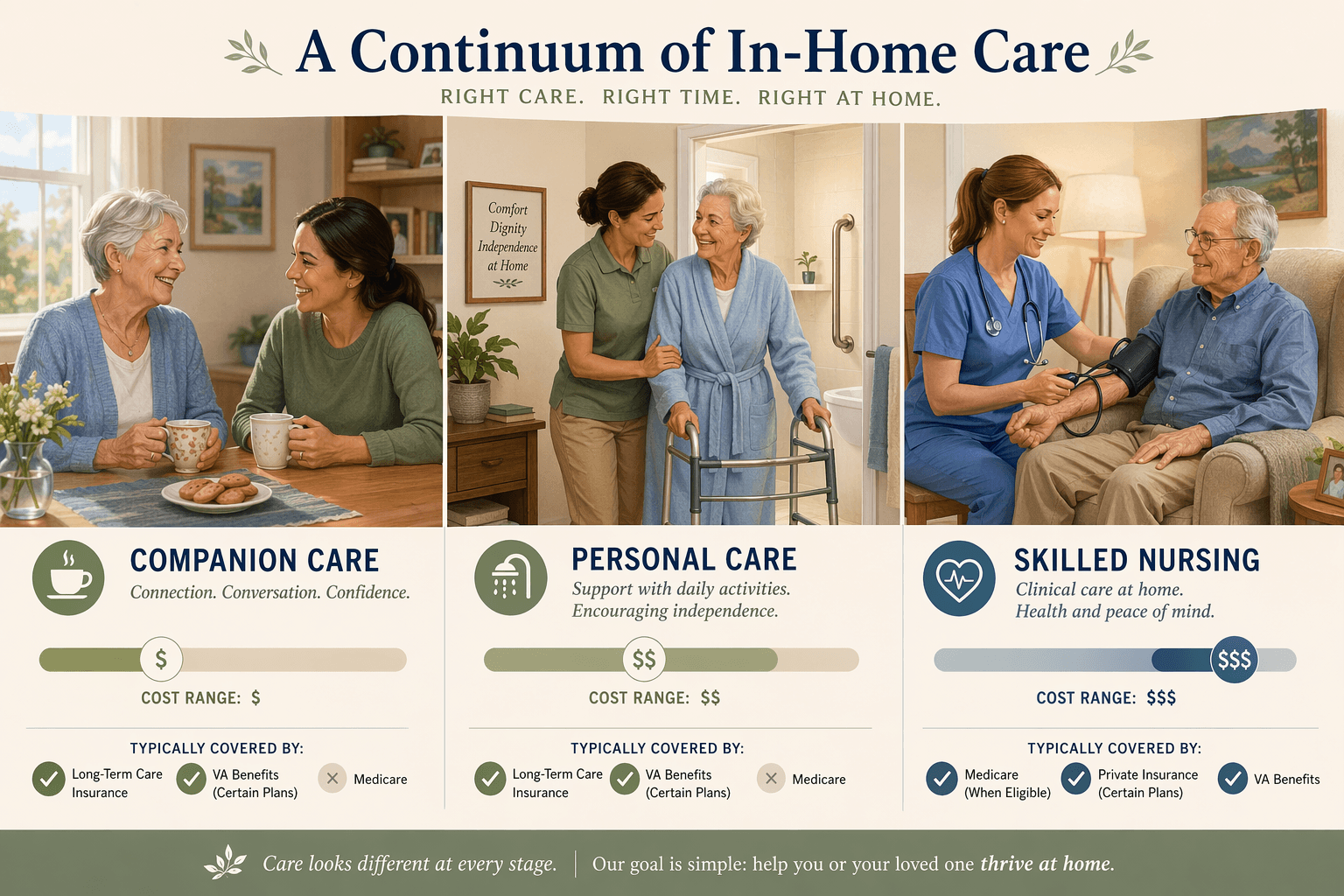

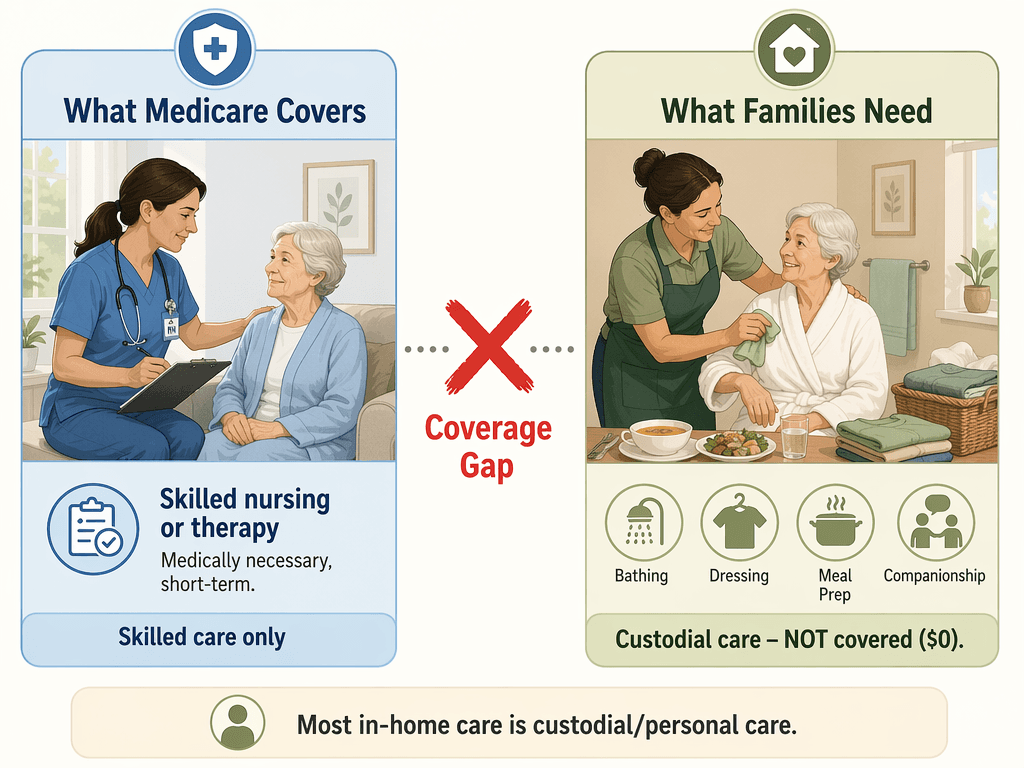

Medicare Part A & B: What It Covers and the Massive Gap Families Discover Too Late

This is the most common point of confusion — and the most painful surprise — for families navigating home care for the first time. Medicare Part A and Part B cover exactly $0 for custodial or personal care. That means the services most older adults need — help with bathing, dressing, toileting, eating, and getting in and out of bed — are not covered by Medicare when those are the only services required.

Here is what Medicare does cover for home health services, according to the official Medicare.gov guidelines:

- Skilled nursing care (part-time or intermittent) — must be medically necessary

- Physical therapy, occupational therapy, and speech-language pathology services

- Medical social services

- Home health aide services — but only when the patient is also receiving skilled care (a nurse or therapist must already be visiting)

- Durable medical equipment (DME) — at 80% of the Medicare-approved amount after the Part B deductible

To qualify for any of this, the patient must be homebound (leaving home requires considerable effort) and under the care of a physician who documents an in-person visit within 90 days before or 30 days after the start of home health services. The care must come from a Medicare-certified agency.

For a more detailed breakdown of Medicare home health eligibility, coverage limits, and the specific conditions that must be met, see our dedicated guide: Does Medicare Cover Home Health Care? A Caregiver's Guide to Eligibility, Costs, and Coverage Gaps in 2026.

Medicare Advantage: Variations by Plan

Medicare Advantage plans (Part C) are offered by private insurers and may include additional home care benefits beyond what Original Medicare provides. Some plans offer limited coverage for personal care services, meal delivery after a hospital stay, or in-home support services. However, these benefits vary significantly by plan and change annually.

If your parent has a Medicare Advantage plan, the most reliable step is to review the plan's Summary of Benefits document for the current year. Look specifically for terms like "in-home support services," "personal care," or "home health aide" in the benefits list. Call the plan directly and ask: does this plan cover any non-skilled personal care at home, and if so, what are the limits on hours, duration, and prior authorization requirements?

Medicaid HCBS Waivers: The Largest Funding Source for Long-Term Home Care

For families with limited financial resources, Medicaid's Home and Community-Based Services (HCBS) waivers represent the single largest funding source for long-term in-home care. Unlike Medicare, Medicaid can cover non-medical personal care — bathing, dressing, meal preparation, light housekeeping, and companionship — for eligible individuals who would otherwise require nursing home care.

The catch is that HCBS waivers are state-administered programs, which means eligibility rules, covered services, and waitlist lengths vary dramatically depending on where your parent lives. Some states have generous programs with no waitlist; others have capped enrollment and years-long waiting periods.

Key features of Medicaid HCBS waivers include:

- Coverage for non-medical personal care services that Medicare does not cover

- Financial eligibility based on income and assets (limits vary by state)

- Functional eligibility — the applicant must need a nursing-home level of care

- Participant-directed or "cash and counseling" programs that allow families to hire their own caregivers, including family members in some states

The Alzheimer's Association notes that some states offer participant-directed services that let seniors with limited resources pay a person of their choosing — including a family member — for in-home services. This can be a game-changer for families who want to compensate a relative who is already providing care.

VA Aid & Attendance and Home Health Benefits

If your parent is a wartime veteran or the surviving spouse of one, the Department of Veterans Affairs offers two significant pathways for home care funding that are frequently underclaimed.

The first is the VA Improved Pension with Aid and Attendance benefit. This is a monthly cash payment added to the basic VA pension for veterans (and surviving spouses) who need the regular assistance of another person to perform daily activities. The funds can be used to pay for home care, including a home health aide, personal care assistant, or even a family caregiver in some circumstances.

The second pathway is home health benefits through the VA health system. Eligible veterans can receive skilled home health care — nursing, physical therapy, occupational therapy — through VA medical centers, often with no out-of-pocket costs. The VA also offers homemaker and home health aide services for veterans who need help with daily activities.

Eligibility for Aid and Attendance requires:

- At least 90 days of active military service, with at least one day during a wartime period

- An honorable discharge (other than dishonorable)

- Financial need based on income and assets

- Medical evidence that the veteran needs help with daily activities or is housebound

The application process requires submitting VA Form 21-2680 (Examination for Housebound Status or Permanent Need for Regular Aid and Attendance) along with medical evidence. Many veterans and surviving spouses who qualify for this benefit are not receiving it — the application process is complex, and awareness is low.

Long-Term Care Insurance: How It Works for Home Care Claims

Long-term care insurance policies vary enormously in what they cover for home care. Some policies explicitly cover home health aide services, personal care, and even companion care. Others cover only skilled nursing facility stays. The key is to read the specific policy — not the marketing materials — to understand the daily benefit amount, the elimination period (how many days of care you must pay for before the policy kicks in), and the list of covered services.

If your parent has a long-term care insurance policy, here is what to check:

- Does the policy cover home care, or only facility-based care?

- What is the daily or monthly maximum benefit for home care services?

- What is the elimination period, and does it apply to home care claims?

- Does the policy require prior authorization and a care plan from a physician?

- Are there restrictions on who can provide care (licensed agency only, or can you hire a private caregiver)?

Most policies require that the insured person needs help with at least two activities of daily living (ADLs) — such as bathing, dressing, or transferring — and that a physician certifies this need. If the policy covers home care, it can significantly offset the monthly costs shown in the table above.

Out-of-Pocket Strategies: Home Equity, Reverse Mortgages, and Life Insurance Conversions

When government programs and insurance fall short — which they often do — families turn to private-pay strategies. These are not ideal, but they are common, and understanding the options can help you make a more informed decision.

The most frequently used out-of-pocket approaches include:

- Home equity: A home equity line of credit (HELOC) or reverse mortgage can provide a lump sum or ongoing payments to fund care. A reverse mortgage allows homeowners aged 62+ to convert part of their home equity into cash without selling the home. The loan is repaid when the homeowner moves out or passes away.

- Life insurance conversions: Some permanent life insurance policies can be converted to a viatical settlement (selling the policy to a third party for a lump sum) or an accelerated death benefit (receiving a portion of the death benefit early). These options are typically available only for policyholders with a terminal or chronic illness.

- Home care loans: Some financial institutions and nonprofit organizations offer loans specifically for home care expenses. These are less common but worth exploring if other options are exhausted.

Community Programs and State-Specific Options

Beyond the major funding sources, a network of community-based programs can supplement paid care and reduce the overall financial burden. These programs rarely cover the full cost of home care, but they can fill important gaps.

Key community resources include:

- Area Agencies on Aging (AAAs): These local offices provide information, referrals, and access to home- and community-based services. They can help you navigate Medicaid waivers, meal programs, and caregiver support services.

- National Family Caregiver Support Program: This federal program provides grants to states to offer information, counseling, respite care, and supplemental services to family caregivers.

- Meals on Wheels: Delivers nutritious meals to older adults at home. While not a substitute for personal care, it reduces the need for meal preparation assistance.

- Adult day care subsidies: Some states and local organizations offer financial assistance for adult day care programs, which can reduce the hours of in-home care needed.

- State-specific programs: For example, California's In-Home Supportive Services (IHSS) program provides personal care services to low-income seniors and people with disabilities, allowing them to hire their own caregivers — including family members.

Participant-directed or "cash and counseling" programs, mentioned by the Alzheimer's Association, are available in many states. These programs give families a budget to hire their own caregivers — including relatives — rather than being limited to agency-provided staff. This can significantly reduce costs while allowing the family to choose someone the older adult trusts.

Tax Deductions for Medical Care at Home

Some home care expenses may be tax-deductible as medical expenses, but the rules are specific and often misunderstood. According to A Place for Mom, unreimbursed medical expenses that exceed 7.5% of your adjusted gross income (AGI) can be claimed as an itemized deduction on your federal tax return. This includes costs for medically necessary help with activities of daily living — such as bathing, dressing, and toileting — if a physician prescribes that care.

However, SeniorLiving.org notes that non-medical ADL assistance costs — such as companion care or homemaker services that are not prescribed by a doctor — are generally not deductible. The key distinction is whether the care is medically necessary and prescribed by a physician, versus simply helpful for daily living.

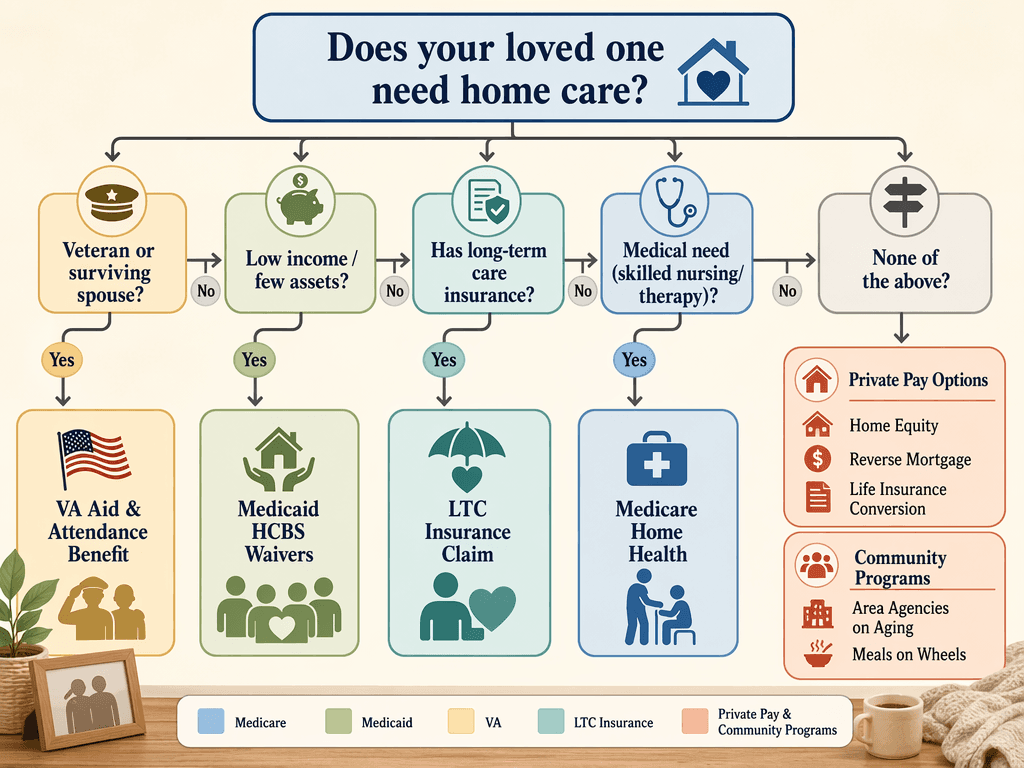

Decision Flowchart: Which Funding Source Applies to Your Situation

The following decision framework consolidates all the pathways discussed above into a single, scannable guide. Start at the top and work through each question to identify which funding sources are most relevant to your parent's situation.

- Is your parent a wartime veteran or the surviving spouse of one? If yes, apply for VA Aid & Attendance and explore VA home health benefits. This is the most commonly missed funding source.

- Does your parent have limited income and assets? If yes, contact your state Medicaid agency to check eligibility for HCBS waivers. These waivers can cover personal care services that Medicare does not.

- Does your parent have a long-term care insurance policy? If yes, review the policy to see if it covers home care. Check the daily benefit amount, elimination period, and whether prior authorization is required.

- Does your parent need skilled nursing, physical therapy, or occupational therapy after a hospital stay or illness? If yes, Medicare home health may cover these services on a short-term basis, provided your parent is homebound and under a physician's care.

- Does your parent need only custodial care (help with bathing, dressing, meals) with no skilled care component? If yes, Medicare will not cover it. Move to private-pay options, community programs, and tax deductions.

- Can your family afford to pay out of pocket for the needed hours of care? If yes, consider using home equity, a reverse mortgage, or life insurance conversion to fund care. Compare the cost of home care to assisted living using the 40-hour rule of thumb.

- Are there community programs available in your parent's state? Contact the local Area Agency on Aging or call the Eldercare Locator (800.677.1116) to learn about meal delivery, adult day care subsidies, and participant-directed programs.

- Have you tracked all out-of-pocket medical expenses? If the total exceeds 7.5% of your AGI, consult a tax professional about deducting medically necessary home care costs.

This decision framework is designed to be used alongside the site's other resources. For a quick-reference list of all funding sources, see How to Pay for In-Home Care in 2026: 7 Funding Sources Families Need to Know. For a broader overview of government programs beyond home care, see The Complete Guide to Government Help for Elderly and Disabled Adults: 8 Major Programs and How to Access Them.

No single funding source will cover everything for every family. The goal is to layer multiple sources — VA benefits plus community programs, or Medicaid waivers plus a small amount of private pay — to build a sustainable plan that keeps your parent safe at home without bankrupting the family.

Read the Full Guide

FAQs provide a concise answer. For comprehensive coverage, see these related guides.

- Are Home Monitoring Cameras Legal for Elderly Parents? A Privacy and Consent Guide

A practical FAQ for family caregivers navigating the legal and ethical questions around installing cameras in an aging parent's private home — covering federal and state consent rules, cognitive capacity, placement restrictions, and privacy-respecting alternatives.

- CAPS Contractor vs General Contractor: Which Do You Need for Aging-in-Place Home Modifications?

Deciding between a CAPS-certified specialist and a general contractor for home modifications? This article compares their training, focus, and costs to help you choose the right professional for your aging-in-place project.

- What Medications Increase Fall Risk in Older Adults? A Caregiver FAQ

This FAQ helps family caregivers quickly identify which prescription and over-the-counter medications raise fall risk in older adults, explains how they cause falls (sedation, orthostatic hypotension, dizziness), and provides actionable steps — including when to talk to a doctor or pharmacist about a medication review.

Comments

Join the discussion with an anonymous comment.