The Hidden Financial Toll of Dementia: What Most Families Don't See Coming

Reviewed: 2026-06-30

The Hidden Financial Toll of Dementia: What Most Families Don't See Coming

Families facing a dementia diagnosis tend to focus on monthly memory care bills, but the true financial burden goes much deeper. This article uncovers the catastrophic hidden costs—lost wages, unpaid caregiving, and diminished quality of life—and explains why early planning is the only defense.

By Editorial Team

early-stage Alzheimer's

middle-stage Alzheimer's

late-stage Alzheimer's

wandering

sundowning

agitation

repetitive questioning

sleep disturbances

eating refusal

dementia communication

safety planning

hospice and end-of-life

BPSD

The first number most families search for is the monthly price of memory care. That is understandable. A diagnosis lands, someone opens a browser tab, and the family starts looking for a figure that can be divided among savings, Social Security, pensions, siblings, and hope.

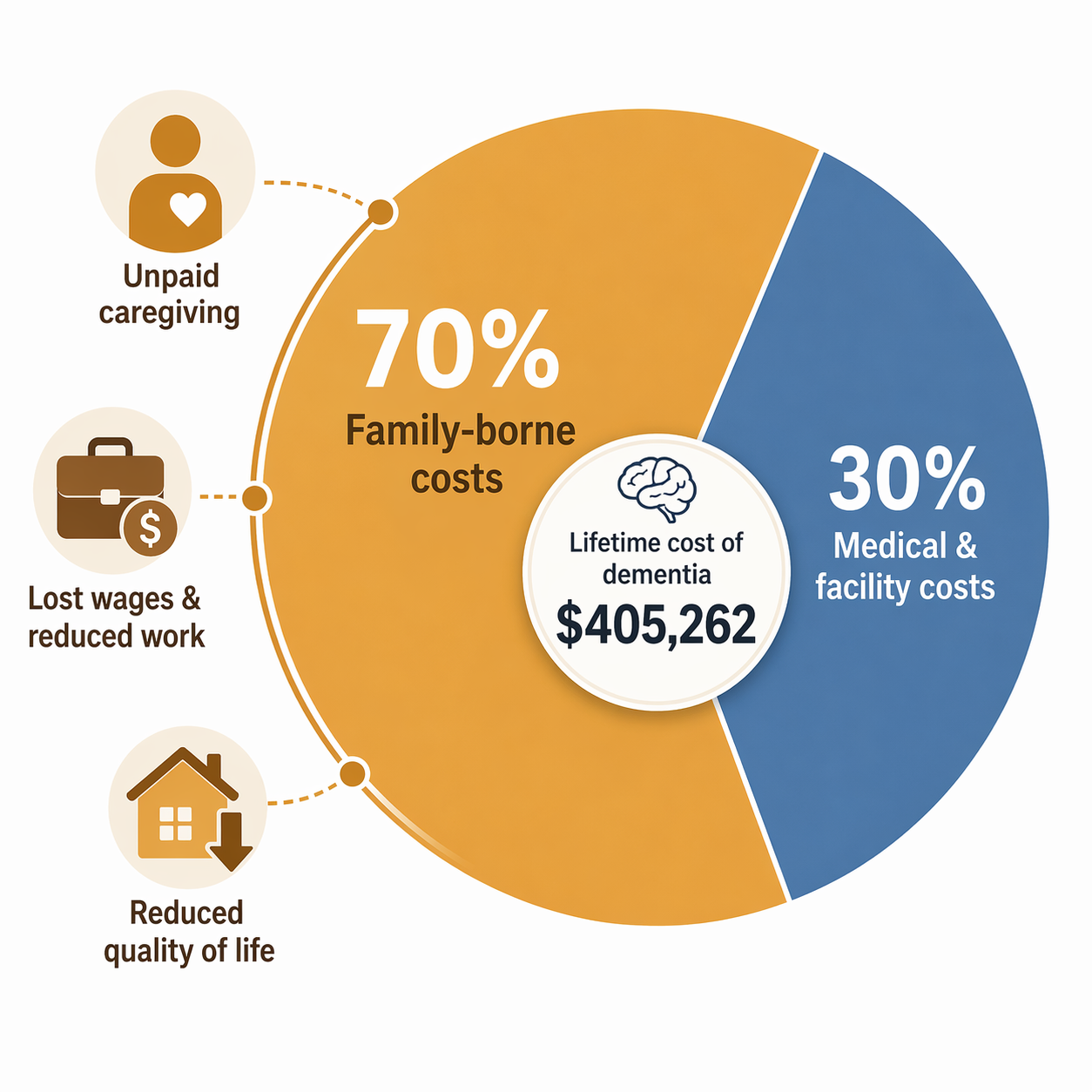

But the number that should stop the room is not the monthly bill. It is $405,262: the estimated total lifetime cost of care for a person with dementia. The Alzheimer’s Association reports that 70% of that cost is borne by families through unpaid caregiving and out-of-pocket spending.[1]

That is the part families are least prepared to name. The invoice from a memory care community is visible. The aide’s hourly rate is visible. What often stays hidden is the daughter who drops from full-time to part-time, the spouse who stops sleeping through the night, the brother who starts covering groceries and copays because he lives closest, and the adult child who quietly puts home care on a credit card while the family waits to understand Medicaid.

Dementia changes what senior care costs mean. It stretches the bill across work hours, retirement savings, household income, family roles, and health. By the time everyone agrees it has become financially serious, the family may already have been paying for months or years.

The monthly bill is only the visible edge

Memory care prices are real, and they are high enough to force hard decisions. A Place for Mom reported a national median memory care cost of $6,690 per month in April 2026, based on its proprietary partner data.[2] SeniorLiving.org reported a higher national median of $8,019 per month in May 2026, using survey-based data.[3] The difference matters, but it does not cancel the point: families are often looking at a five-figure annual commitment before adding medication, transportation, clothing, dental care, incontinence supplies, or private help.

Home care can look gentler because it is priced by the hour. That comfort can disappear quickly. A Place for Mom reported median in-home care rates of about $34 to $35 per hour in 2026.[2] A few hours a week may help a working adult child keep a parent safe. Round-the-clock supervision is a different financial universe, which is why families comparing home care with memory care should run the math before assuming home is always cheaper. For a deeper payment-pathway comparison, see The Full Financial Picture of Dementia Care.

Nursing home care can be even more expensive. Amplify Life, citing Genworth data, reports a private nursing home room cost of $129,575 per year.[4] That figure is not a prediction for every person with dementia, but it is a useful warning: once care requires constant supervision, hands-on help, or a secure setting, the family is no longer budgeting for ordinary aging.

Care cost families often price first

Reported 2026 figure

What the figure does not capture

Memory care

$6,690 to $8,019 per month

Unpaid family labor, transition costs, uncovered extras, and lost work time

In-home care

$34 to $35 per hour

The cost jump when supervision becomes daily or continuous

Private nursing home room

$129,575 per year

The family losses that happened before nursing home care began

The hidden bill has names

In June 2026, USC Schaeffer estimated the total U.S. cost of dementia at $818 billion for 2026. The number is almost too large to feel personal until it is broken apart: $237 billion in unpaid caregiving, $320 billion in quality-of-life losses, and $23 billion in lost wages.[5]

Those categories are not soft costs. They are the places where families absorb the work because no one sends an invoice. A missed promotion does not arrive as a dementia bill. Neither does a spouse’s exhaustion, a sibling’s reduced retirement contribution, or the choice to decline overtime because no one else can stay with Mom after 4 p.m.

The Alzheimer’s Association estimated that 7.4 million Americans were living with Alzheimer’s dementia in 2026.[1] USC Schaeffer used a different definition, estimating costs for 5.7 million people with all-cause dementia.[5] Those figures should not be mashed together as if they count the same population. But both point to the same family reality: dementia care is not a narrow medical expense. It is a long, uneven transfer of labor and risk into households.

Unpaid caregiving is work, even when love is the reason

Many families want to provide care at home. That choice can be loving, culturally rooted, emotionally right, and still financially costly. Respecting the choice does not require pretending the labor is free.

The Population Reference Bureau reported that older Americans receiving dementia care at home received an average of 92 hours of care per month, and that 66% lived with a caregiver.[6] That is not “checking in.” That is a part-time job woven through medication reminders, bathing help, meals, wandering prevention, transportation, bill paying, emergency calls, and the constant mental load of being responsible.

Once the family absorbs those hours, the formal care plan can look cheaper than it is. A parent may be “aging in place,” but the daughter may be aging out of promotions. The spouse may be keeping the household together by giving up sleep. The nearby sibling may be spending Saturday after Saturday managing errands that no care-cost spreadsheet ever asks about.

Lost wages can become the family’s largest private loss

Penn LDI, discussing research by Norma Coe and colleagues, cited an estimated $80,000 to $100,000 per year in lost earnings and career advancement for a middle-aged daughter providing care.[7] The underlying wage data came from 1998 to 2012, so it should be read as a research benchmark rather than a fresh paycheck-by-paycheck estimate for every 2026 household. Even with that caveat, it names the loss many families never calculate.

That loss is not limited to the year of active caregiving. Reduced hours can lower Social Security earnings records, retirement contributions, employer matches, professional momentum, and future bargaining power. It can also concentrate the penalty on the person in the family who is already expected to be flexible.

Families often talk about whether they can afford paid care. They should also ask who is paying when they do not buy it. If one adult child is using vacation days for neurology appointments, another is fielding nighttime calls, and a spouse is missing sleep to prevent wandering, the bill has already been distributed. It just has not been labeled.

Out-of-pocket home care can erase income

The pressure is harsher when there is little margin to begin with. PRB reported that poor individuals with dementia spent 87% of their household income on home care out of pocket.[6] That figure is not a general average for all families; it is worse and more specific than that. It shows how dementia can turn ordinary income limits into a near-total loss of financial room.

Moderate-income families can also be trapped. They may have too much income or too many assets to qualify easily for public help, but not enough to sustain years of private care. That middle zone is where siblings start negotiating who can pay this month, who can take leave, and whether a parent’s remaining savings should go to home care, a move, legal planning, or a facility deposit.

Quality-of-life losses are not sentimental accounting

USC Schaeffer’s $320 billion estimate for quality-of-life losses is the category some people are tempted to treat as less concrete than wages or invoices.[5] Families know better. Dementia can shrink a household’s choices long before paid care begins: fewer visits with grandchildren because the day is too unpredictable, fewer safe outings, less privacy, less sleep, less patience, and less ability to make ordinary plans.

A Place for Mom’s caregiver survey work found that 54% of caregivers wished they had planned sooner, 70% felt only partially ready, and 78% reported burnout.[8] These are attitudes and self-reports, not proof that every family will have the same experience. Still, they line up with what the cost data keeps showing: the crisis is often recognized only after the family’s capacity has already been spent.

The coverage trap catches families late

The most painful misunderstandings usually involve Medicare, Medicaid, and long-term care insurance. Families hear “covered” and assume dementia care will be treated like other serious medical conditions. Then they discover that the care they need most is often classified as custodial: help with bathing, dressing, supervision, meals, toileting, and safety.

Medicare does not cover long-term custodial care. It covers medical care, and it can cover skilled nursing care for a limited period after qualifying conditions, including 100% coverage for the first 20 days. But it does not become a standing payment source for non-medical home care, assisted living, or memory care simply because a person has dementia.

That boundary is where many family budgets break. A parent can be unsafe alone, unable to manage medications, and dependent on daily help, yet still need care that Medicare does not pay for. For more on the skilled-care cutoff and what happens when the need continues, see when Medicare stops paying for home health.

Medicaid can help with long-term care, but it is not a simple fallback for families trying to preserve a parent’s savings. In many states, Medicaid eligibility requires countable assets of $2,000 or less. Rules vary by state, by marital status, and by program, which is why families should not rely on casual advice from a neighbor, a facility tour, or a hurried internet search.

Long-term care insurance helps some households, but many families arrive too late to use it as a clean solution. Amplify Life, citing AARP and AALTCI data, reports that only 21% of adults age 65 and older have long-term care insurance, and that waiting 10 years from age 55 increases the cost of the same coverage by 49.9%.[4] Advice to “look into long-term care insurance” is useful only if it reaches families before age, health, and premiums have narrowed their options.

What early planning can actually change

Planning does not make dementia inexpensive. It can, however, keep the family from learning every rule at the most expensive possible moment. The work starts before the fall, before the wandering episode, before the hospital discharge planner needs an answer by noon, and before one sibling has quietly become the entire care system.

The first practical step is to map the care need, not just the care setting. A family should write down what already happens each week: medication management, meals, bathing, transportation, bill paying, supervision, nighttime safety, appointment scheduling, and behavior changes. This is not paperwork for its own sake. It shows which costs are already being paid in labor and which ones may soon require money.

Ask what Medicare will and will not cover before assuming home care, assisted living, or memory care is included.

Check whether the person with dementia may qualify for Medicaid long-term care or waiver programs, and speak with a qualified elder law or benefits professional early.

Review long-term care insurance while the person is still healthy enough and young enough for options to exist.

Price home care by the likely number of hours needed, not by the comforting hourly rate.

Name the family caregiver’s lost wages, reduced hours, travel, sleep, and health as real costs.

Newly diagnosed families should also check the CMS GUIDE Model. CMS launched the model in July 2024 as an 8-year program, and CMS listed 320 participating organizations nationwide as of 2026. For eligible Medicare beneficiaries, GUIDE can provide care navigation, 24/7 support, caregiver training, and up to $2,500 per year in respite with no cost-sharing.[9]

GUIDE is not a national cure-all. Availability and quality depend on participating organizations, and the 320 figure counts organizations, not facility locations.[9] Still, it is one of the few resources aimed directly at the navigation and caregiver-support gap that leaves families improvising.

The hard part is that dementia planning asks families to make financial decisions while they are still hoping the diagnosis will move slowly. Waiting feels kinder. It can also leave the family with fewer choices.

The first crisis is not only a medical event. It is often the moment families start paying with work hours, savings, sleep, and choices they cannot easily recover. That is why early conversations about Medicare limits, Medicaid rules, GUIDE availability, home care math, memory care costs, and the caregiver’s own financial exposure are not pessimistic. They are protection.

No article can tell a family which tradeoff is right. But it can say this plainly: the cost of dementia is not just the facility bill. If the plan does not count unpaid caregiving, lost wages, and the family’s shrinking room to breathe, it is not yet a real plan.

Comments

Join the discussion with an anonymous comment.