Senior Care Options in 2026: A Cost Reality Check for Families

cost reality checkReviewed: 2026-06-20

Senior Care Options in 2026: A Cost Reality Check for Families

Adult children and spousal caregivers often underestimate annual senior care expenses by tens of thousands of dollars. This article provides a comprehensive 2026 cost reality check across all eight care types, including state-by-state data, pricing model traps, and a breakdown of payment sources to help families plan proactively.

By Editorial Team

senior care costs

assisted living cost

memory care cost

in-home care cost

Medicare coverage

Medicaid eligibility

VA benefits

long-term care insurance

crisis planning

caregiver financial planning

The 2026 Senior Care Cost Reality: Why Most Families Underestimate by $30,000+

If you are reading this in the middle of a crisis — after a fall, a hospital discharge, or a dementia diagnosis — you are not alone, but you are also at a financial disadvantage. Families who delay planning until an urgent event forces a decision routinely underestimate their annual senior care expenses by tens of thousands of dollars. The gap between what people expect to pay and what they actually pay is driven by three persistent misconceptions that this article will dismantle one by one.

First, many families assume that keeping a loved one at home is the cheaper option. It is not — not when care needs reach 44 hours per week or more. Second, a majority of Americans believe Medicare will cover long-term custodial care. It will not. A 2026 survey found that 56% of families get this wrong, a knowledge gap that can derail even the most careful budget. Third, the instinct to postpone difficult conversations about care and finances until "we have to" carries a real price tag: reactive decisions made under time pressure cost an estimated 20–30% more than proactive planning.

2026 National Cost Summary: What Each Care Type Actually Costs

The table below presents the national median monthly and annual costs for each care type, drawn from multiple 2026 sources. Note that memory care figures vary notably between datasets — a discrepancy we will explain below the table.

2026 National Median Senior Care Costs. Memory care ranges reflect source variation (see callout below).

Care Type

National Median Monthly Cost

National Median Annual Cost

Primary Source

In-Home Care (nonmedical, 44 hrs/wk)

$6,673

$80,080

U.S. News (CareScout 2025 data)

Adult Day Services (8 hrs/day)

$2,090

$25,080

U.S. News (CareScout 2025 data)

Independent Living

$3,200 – $3,523

$38,400 – $42,276

A Place for Mom 2026 / U.S. News

Assisted Living

$5,419

$65,028

A Place for Mom 2026

Memory Care

$6,690 – $8,399

$80,280 – $100,788

A Place for Mom 2026 / NIC via AARP

Skilled Nursing (Semi-Private)

$9,581

$114,972

U.S. News (CareScout 2025 data)

Skilled Nursing (Private)

$10,798

$129,576

U.S. News (CareScout 2025 data)

CCRC (Entrance Fee + Monthly)

$100,000 – $2,000,000 (entrance fee)

Varies widely

U.S. News

Hospice Care

Covered by Medicare, Medicaid, most private insurance

N/A

Alzheimer's Association

A few patterns jump out immediately. Assisted living costs have been rising roughly 5% per year, and in 2024 alone the median surged 10% to $70,800 annually before settling back slightly in 2025–2026 data. Memory care commands a 20–30% premium over assisted living, reflecting the higher staff-to-resident ratios, secure environments, and specialized programming required for residents with dementia. Skilled nursing remains the most expensive continuous care option, with a private room now exceeding $10,000 per month nationally.

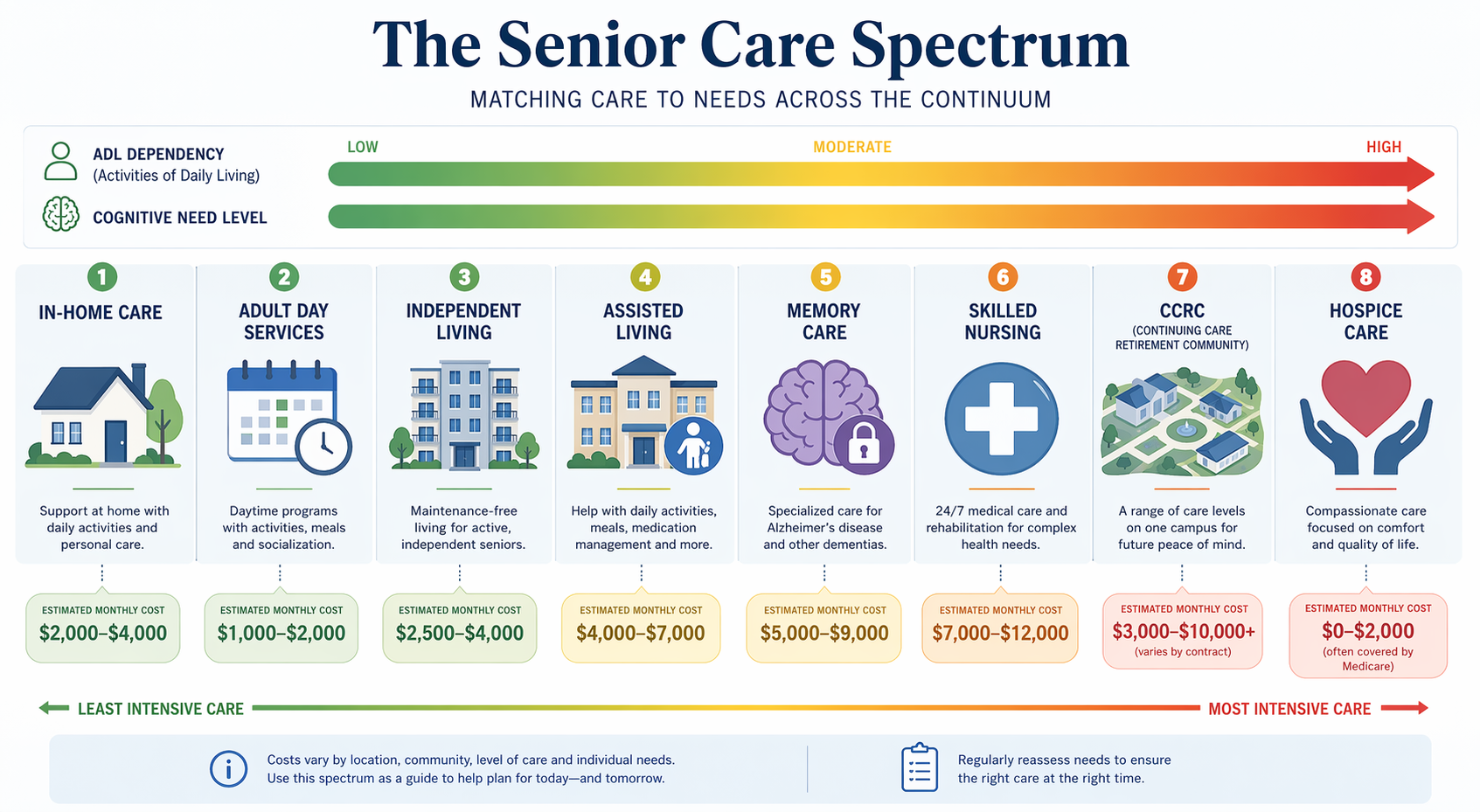

The senior care spectrum: matching care type to need level and cost. Source: CareWise Guide analysis of 2026 national data.

Geographic Cost Variation: Why Location Changes Your Budget by $60,000/Year

National medians are a useful starting point, but they can mislead families who live in high-cost or low-cost states. The difference between the most and least expensive states for assisted living alone exceeds $60,000 per year. According to A Place for Mom's 2026 state-by-state analysis of 24,000+ resident moves, the range is dramatic.

2026 State-by-State Median Assisted Living Costs. Source: A Place for Mom 2026 Pricing Guide.

State

Median Assisted Living Monthly Cost

Annual Cost

Louisiana

$3,983

$47,796

Missouri

$4,100

$49,200

Florida

$4,624

$55,488

Texas

$5,458

$65,496

California

$5,739

$68,868

New York

$6,195

$74,340

Massachusetts

$6,800

$81,600

District of Columbia

$8,960

$107,520

A family in Louisiana paying $3,983 per month for assisted living is spending less than half of what a family in Washington, D.C. pays for the same level of care. This variation means that a budget that works in one state may be completely inadequate in another — and that relocation, while emotionally difficult, can be a legitimate financial strategy for some families.

The Hidden Cost of Staying Home: When In-Home Care Costs More Than Assisted Living

The most persistent myth in senior care is that staying at home is always the most affordable option. It is not — not when care needs reach a level that requires consistent, daily assistance. Nonmedical in-home care averages $35 per hour nationally. At 44 hours per week — roughly the threshold where a family caregiver can no longer manage alone — that adds up to $80,080 per year. Compare that to assisted living at $65,028 per year, and the math flips.

The cost crossover: at 44+ hours per week of paid care, assisted living is more affordable than in-home care.

The crossover point — where facility care becomes cheaper than in-home care — typically occurs somewhere between 30 and 40 hours per week of paid in-home help, depending on local labor rates and facility pricing. Below that threshold, part-time in-home care is usually less expensive. Above it, assisted living or memory care often saves families $15,000 or more per year while also providing built-in social engagement, meals, and 24-hour supervision.

Pricing Model Traps: All-Inclusive vs. Tiered vs. A La Carte

Even when families have accurate base rates, they can be blindsided by how facilities structure their pricing. Assisted living and memory care communities typically use one of three pricing models, and each carries distinct risks for the unwary budgeter.

All-inclusive: A single monthly fee covers rent, meals, housekeeping, activities, and most care services. This model is cost-effective for residents with high care needs because additional services do not trigger extra charges. However, low-need residents may pay for services they never use, effectively subsidizing higher-need neighbors.

Tiered pricing: The base rate covers a low level of care (e.g., 30 minutes of assistance per day). As needs increase, the resident moves into higher tiers, each with a significant price jump. Families who budget only for the entry-level tier can be shocked when monthly costs rise by $1,000–$2,000 as care needs escalate.

A la carte: The base rate covers only room and board. Every additional service — medication management, bathing assistance, escorts to meals — is billed separately. This model offers flexibility but makes it very difficult to predict total monthly expenses. Families often underestimate by 30–50% in the first month.

Beyond the monthly pricing model, two additional fees frequently catch families off guard. The median community or move-in fee is approximately $3,000, and some facilities charge a second-person fee — typically around $1,200 per month — if a couple shares a unit. Always ask for a complete fee schedule during the first tour, not just the base rate.

Payment Sources Breakdown: What Medicare, Medicaid, VA Benefits, and LTC Insurance Actually Cover

Understanding what each payment source actually covers — and, just as importantly, what it does not cover — is the single most important step in building a realistic senior care budget. The table below summarizes the key facts every family should know.

What each payment source covers — and the critical gaps families must plan for.

Payment Source

What It Covers

What It Does NOT Cover

Key Limitation

Medicare (Parts A & B)

Short-term skilled nursing (up to 100 days after a qualifying hospital stay); limited home health care if homebound and requiring skilled services

Long-term custodial care; assisted living room and board; 24/7 in-home care; memory care

56% of families mistakenly believe Medicare covers long-term care. It covers only skilled, short-term, medically necessary care.

Medicaid

Long-term custodial care in nursing homes; some home and community-based services (HCBS waivers); may cover assisted living in certain states

Assisted living room and board in most states; memory care in many states; CCRC entrance fees

Requires spending down assets to near-poverty levels. Has a five-year look-back period on asset transfers. Eligibility rules vary by state.

VA Aid and Attendance

Monthly pension supplement for veterans and surviving spouses who need assistance with daily activities

Does not cover the full cost of care; supplements other income

Single veteran: up to $2,424/month. Married veteran: up to $2,874/month. Surviving spouse: up to $1,558/month. (Per American Council on Aging, 2025 data.)

Long-Term Care Insurance

Varies by policy; typically covers a daily or monthly benefit for assisted living, memory care, nursing home, or home care

May have elimination periods (e.g., 90 days before benefits begin); may not cover all care types; premiums can increase

Fewer than 10% of older adults have LTC insurance. Policies purchased years ago may have inadequate benefit amounts for 2026 costs.

Private Pay / Out-of-Pocket

Any care type; no restrictions

Depletes savings rapidly

The most common payment method for assisted living and memory care. At $5,419/month, a $200,000 savings account lasts about 3 years.

The Medicare knowledge gap is particularly damaging. A 2026 survey found that 56% of families incorrectly believe Medicare will cover long-term custodial care. In reality, Medicare covers only short-term skilled nursing care following a qualifying hospital stay (up to 100 days, with significant copays after day 20) and limited home health care for those who are homebound and require skilled services. It does not cover assisted living room and board, memory care, or 24/7 in-home care.

The Crisis-Planning Penalty: Why Reactive Decisions Cost 20–30% More

There is a hidden cost that does not appear on any facility's fee schedule, yet it affects the majority of families: the crisis-planning penalty. When a fall, a hospital discharge, or a wandering episode forces a family to make a care decision in days rather than months, the financial consequences are severe.

The crisis-planning penalty: reactive decisions cost 20–30% more than proactive planning.

Based on observed patterns across thousands of family cases, reactive decisions carry a cost premium of 20–30% for several reasons. Families who need placement immediately have limited options — they may have to accept whatever bed is available, often at a higher rate than a pre-selected community. They lack time to explore payment options like VA benefits or Medicaid planning, so they default to private pay. They cannot wait for a facility with a waitlist, even if that facility offers better value. And they often choose a higher level of care than needed because they do not have time to assess whether a less intensive option would suffice.

The contrast between proactive and reactive planning is stark. A family that begins researching options six to twelve months before care is needed can tour multiple facilities, compare pricing models, verify Medicaid eligibility, apply for VA benefits, and negotiate move-in fees. A family that makes a decision from a hospital discharge planner's list of available beds has none of those advantages.

Budgeting for the Full Care Trajectory: How Costs Escalate as Needs Increase

Most families make a critical budgeting error: they plan for the current level of care, not the expected progression. But senior care is rarely static. A person who enters independent living today may need assisted living in two years, memory care in four years, and skilled nursing in six years. Each transition brings a significant cost increase.

Typical cost progression as care needs increase. Each transition represents a significant jump in monthly expenses.

Care Level

Typical Monthly Cost

Annual Cost

Cost Increase from Previous Level

Independent Living

$3,200

$38,400

Baseline

Assisted Living

$5,419

$65,028

+69%

Memory Care

$6,690 – $8,399

$80,280 – $100,788

+23% to +55% over assisted living

Skilled Nursing (Semi-Private)

$9,581

$114,972

+43% over memory care

Skilled Nursing (Private)

$10,798

$129,576

+13% over semi-private

Continuing care retirement communities (CCRCs) offer an alternative to this stepwise cost escalation. By paying a substantial entrance fee — typically ranging from $100,000 to $2 million, with 25–80% potentially refundable upon departure or death — residents lock in access to a full continuum of care on a single campus. Monthly fees then increase only modestly as care needs rise, rather than jumping by 69% or more. The trade-off is the upfront cost and the requirement to enter the community while still relatively independent.

Action Checklist: 5 Steps to Build Your Senior Care Budget Today

The best time to start planning was a year ago. The second-best time is today. Use this checklist to move from anxiety to action, whether you are planning proactively or responding to a recent crisis.

Conduct a financial audit. List all sources of income (Social Security, pensions, retirement accounts, VA benefits, rental income) and all assets (savings, investments, home equity, life insurance cash value). Calculate the monthly income available for care costs. This is your baseline budget.

Gather key documents. Collect bank statements, tax returns (last 3 years), Social Security award letters, pension statements, insurance policies (health, long-term care, life), VA records, and any trust or estate planning documents. You will need these for Medicaid applications, VA benefit claims, and facility financial reviews.

Research state-specific costs and Medicaid eligibility. Use the state-by-state data in this article as a starting point, then contact facilities in your target area for current pricing. Check your state's Medicaid eligibility rules, income limits, and asset limits — they vary significantly and change frequently.

Consult an elder law attorney. Before transferring assets, selling a home, or making any major financial move, get professional advice. An elder law attorney can help with Medicaid planning, asset protection trusts, VA benefit applications, and powers of attorney. The cost of a consultation ($300–$500) is trivial compared to the cost of a mistake.

Schedule a family care talk — now, not later. The single most expensive decision a family can make is to delay the conversation until a crisis forces it. Use the cost data in this article to start the discussion with concrete numbers, not abstract fears. Even if no decision is made immediately, the act of talking creates a foundation for proactive planning.

Comments

Join the discussion with an anonymous comment.