Senior Care Options: A Complete Glossary of Care Types, 2026 Costs, and Who Each Is For

clinicalA plain-language glossary of every major senior care option — from aging in place to hospice — with 2026 national cost ranges, who each option is right for, and who it is NOT for. Designed for new caregivers who need a quick, scannable reference.

Introduction: A Starting Point for Families New to Senior Care

When a parent or spouse begins to need more help than you can provide alone, the first hurdle isn't deciding — it's understanding what the options even mean. Assisted living, skilled nursing, board and care, CCRC, hospice, palliative care. The vocabulary alone can make you feel like you need a translator before you can make a single decision.

This glossary is that translator. It defines each major senior care option in plain language, gives the 2026 national cost range, and — most importantly — tells you exactly who each option is right for and who it is NOT for. It is designed to be scanned, bookmarked, and returned to as your family's needs evolve.

If you encounter a term you don't recognize, check our Navigating Senior Health Care: Key Terms Every Caregiver Should Know guide for additional definitions.

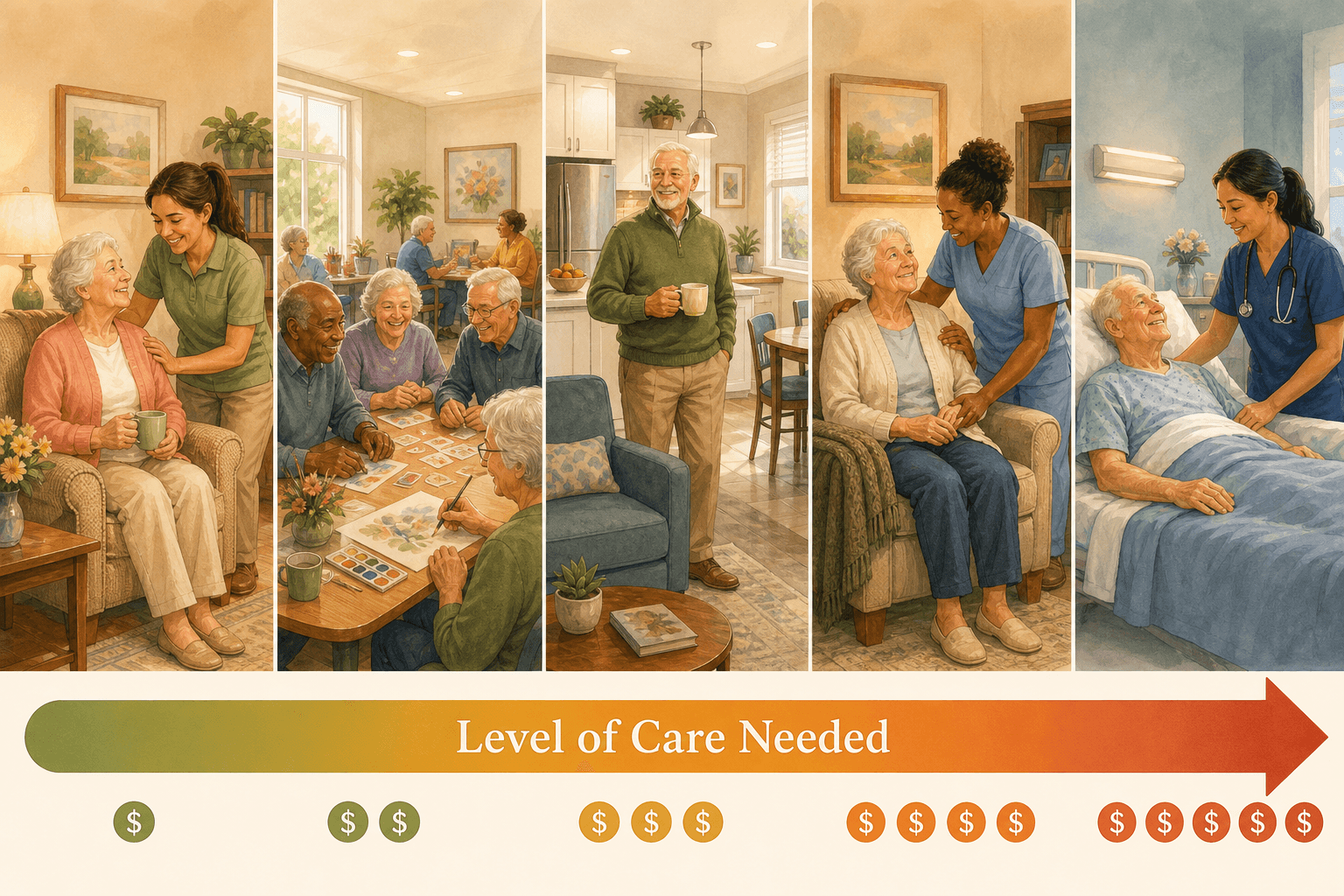

The Senior Care Spectrum: From Least to Most Intensive

Senior care options exist along a spectrum. On one end, a person lives independently in their own home with occasional help. On the other, a person receives round-the-clock skilled nursing care. Most families move along this spectrum gradually as needs increase, though some transitions happen suddenly after a hospitalization or diagnosis.

The entries below are organized roughly from least to most intensive, but individual needs vary. A person with advanced dementia may need memory care (a high-intensity setting) while still being physically healthy, while someone with a complex medical condition may need skilled nursing even if they are cognitively sharp.

Aging in Place

Aging in place means remaining in one's own home — a house, apartment, or condo — safely and independently for as long as possible. It is the most common preference among older adults and the least institutional option on the care spectrum.

Daily life typically involves a combination of home modifications (grab bars, stair lifts, widened doorways), family help with errands and transportation, and occasional paid services like meal delivery or housekeeping. The level of support can range from zero assistance to a full team of home care aides, depending on the person's needs.

Costs vary enormously — from $0 for family-only support to thousands per month for paid care and modifications. There is no single national median because the definition is so broad.

- Who it's for: Seniors with mild to moderate needs who have a safe, accessible home and a reliable family or paid caregiver network.

- Who it's NOT for: Seniors with high medical needs requiring 24/7 skilled nursing, those living in unsafe or inaccessible homes that cannot be modified, or those without any caregiver support.

Payment options include out-of-pocket funds, VA benefits, Medicaid Home and Community-Based Services (HCBS) waivers in some states, and long-term care insurance. Medicare does not cover custodial care at home.

Home Care (Non-Medical) vs. Home Health Care

These two terms are often used interchangeably, but they describe very different services. Understanding the distinction is critical because it determines what is covered by insurance and what is not.

Non-medical home care (also called custodial or personal care) helps with activities of daily living (ADLs) — bathing, dressing, toileting, eating, and transferring — and instrumental activities (IADLs) like meal preparation, light housekeeping, medication reminders, and companionship. The aides are not licensed medical professionals.

Home health care provides skilled services ordered by a physician — wound care, physical therapy, occupational therapy, speech therapy, medication management, and monitoring of vital signs. These services are delivered by licensed professionals: registered nurses, physical therapists, and certified home health aides who have completed at least 75 hours of training.

| Service Type | 2026 National Median Cost | Source |

|---|---|---|

| Non-medical home care (hourly) | ~$34/hour | A Place for Mom (based on 3,215 agencies, Jan 2026) |

| Non-medical home care (20 hrs/week) | ~$2,944/month | A Place for Mom |

| Home health aide (daily) | $220/day ($6,677/month) | Genworth via SeniorLiving.org |

| Homemaker services (daily) | $213/day ($6,481/month) | Genworth via SeniorLiving.org |

- Who non-medical home care is for: Seniors who need help with daily activities but do not require skilled nursing. They are safe at home with assistance.

- Who non-medical home care is NOT for: Seniors with complex medical needs, unstable conditions, or who need 24/7 skilled monitoring.

- Who home health care is for: Seniors recovering from a hospitalization, surgery, or illness who need short-term skilled therapy or nursing at home.

- Who home health care is NOT for: Seniors who only need custodial help with bathing, dressing, and meals — that is non-medical home care.

Payment options: Medicare Part A and B cover home health care under qualifying conditions. Medicaid covers both home health and custodial home care through HCBS waivers in many states. VA benefits and long-term care insurance may also apply. Most families pay for non-medical home care out-of-pocket. For a full breakdown, see How to Pay for Senior Home Care Services in 2026.

Adult Day Care

Adult day care is a structured daytime program that provides social activities, meals, and some health services in a community setting. Participants attend during the day (typically 6–8 hours) and return home in the evening. It is one of the most affordable and underutilized options in senior care.

Daily life includes group activities, exercise, music, art, lunch, and socializing. Some centers offer basic health monitoring, medication management, and transportation. For caregivers who work during the day, adult day care provides reliable supervision and engagement.

2026 cost: $103/day or $2,232/month median (Genworth via SeniorLiving.org). Some sources report a range of $80–$150 per day.

- Who it's for: Seniors who need supervision and social engagement during the day but are safe at home with a caregiver in the evenings and overnight. Ideal for working family caregivers.

- Who it's NOT for: Seniors who need 24/7 medical monitoring, have severe dementia with wandering behavior that requires a secure environment, or who cannot tolerate a group setting.

Payment options: Medicaid covers adult day care in many states through HCBS waivers. VA benefits may apply. Some long-term care insurance policies cover it. Otherwise, it is paid out-of-pocket.

Independent Living

Independent living communities are age-restricted housing (typically 55+) that offer apartments, condos, or single-family homes with shared amenities and social activities. They do not provide personal care or medical services. Residents must be able to live independently.

Daily life resembles living in a resort or college campus: a private apartment, communal dining options, fitness classes, clubs, transportation, and social events. The appeal is a maintenance-free lifestyle with built-in community.

2026 cost: $3,200/month median (A Place for Mom); range $1,500–$4,500/month (Senioridy).

- Who it's for: Active, healthy seniors who want to downsize, eliminate home maintenance, and enjoy a social community. No significant medical or personal care needs.

- Who it's NOT for: Seniors who need help with bathing, dressing, medication management, or any ADL assistance. Those with significant medical conditions or mobility limitations that require daily skilled care.

Payment: Almost always out-of-pocket. Medicare and Medicaid do not cover independent living. Some long-term care insurance policies may cover care services if they are added later, but not the rent.

Assisted Living

Assisted living is a residential setting for seniors who need help with daily activities but do not require 24/7 skilled nursing. Residents typically live in private apartments and receive personal care, meals, medication management, and 24-hour supervision.

Daily life balances independence with support. Residents have their own space but can access help with bathing, dressing, and medication at any time. Meals are provided in a communal dining room. Social activities, transportation, and housekeeping are included.

| Data Point | Value | Source |

|---|---|---|

| National median monthly cost | $5,419/month | A Place for Mom (based on 24,305 move-ins in 2025) |

| Median length of stay | 22 months | National Center for Assisted Living (NCAL) |

| Typical total cost over stay | ~$119,218 | Calculated from median monthly cost and length of stay |

| Median move-in fee | ~$3,000 | A Place for Mom |

| Second person fee (if applicable) | ~$1,200/month | A Place for Mom |

| National cost range | $3,000–$8,000+/month | Multiple sources |

- Who it's for: Seniors who need moderate help with ADLs (bathing, dressing, medication reminders), are mobile (can walk or use a wheelchair independently), and want social engagement. Good for those who are no longer safe at home alone but do not need a nursing home.

- Who it's NOT for: Seniors with advanced dementia who need a secure memory care environment, those with complex medical conditions requiring skilled nursing, or those who are bedbound or need two-person transfers.

Payment: Mostly out-of-pocket. Some long-term care insurance policies cover assisted living. VA Aid and Attendance benefits may apply. Medicaid covers assisted living in some states through HCBS waivers, but eligibility and availability vary widely. Medicare does not cover assisted living.

Board and Care Homes (Residential Care Homes)

Board and care homes — also called residential care homes or group homes — are small residential facilities that provide personal care, meals, and supervision in a home-like setting. They typically house 20 or fewer residents, often in a converted single-family home.

Daily life is more intimate and less institutional than a large assisted living community. Residents eat meals together in a shared dining room, have private or semi-private bedrooms, and receive help with ADLs from staff who are often more accessible than in larger facilities.

2026 cost: Private room $7,300/month; shared room $6,000/month (U.S. News).

- Who it's for: Seniors who prefer a small, home-like environment and need moderate help with daily activities. Good for those who feel overwhelmed by large facilities.

- Who it's NOT for: Seniors who need skilled nursing care, specialized dementia care with secure wandering paths, or extensive medical services. Board and care homes typically do not have licensed nurses on staff.

Payment: Mostly out-of-pocket. Some states allow Medicaid coverage through HCBS waivers. VA benefits may apply.

Memory Care

Memory care is a specialized residential setting for seniors with Alzheimer's disease or other forms of dementia. These units or facilities are designed with secure environments, specially trained staff, and structured routines that reduce confusion and agitation.

Daily life includes structured routines, memory-enhancing activities, secure wandering paths (so residents can walk safely without eloping), and staff trained in dementia communication techniques. Meals, personal care, and medication management are provided. The environment is typically more controlled and less stimulating than standard assisted living.

2026 cost: $6,690/month median (A Place for Mom). Memory care typically costs 20–30% more than standard assisted living in the same area.

- Who it's for: Seniors with moderate to advanced dementia who need a secure environment, specialized programming, and staff trained in dementia care. Those who wander, have significant behavioral symptoms, or are no longer safe in standard assisted living or at home.

- Who it's NOT for: Seniors with mild memory issues who can still live safely in assisted living or at home with support. Those with complex medical needs that require skilled nursing (a nursing home may be more appropriate).

Payment: Mostly out-of-pocket. Some long-term care insurance policies cover memory care. VA benefits may apply. Medicaid covers memory care in some states through HCBS waivers or in nursing homes that have dementia units. For help deciding between assisted living and memory care, see our Assisted Living vs. Memory Care: A Decision Framework for Dementia Caregivers.

Skilled Nursing / Nursing Home

Skilled nursing facilities — commonly called nursing homes — provide 24/7 skilled nursing care, rehabilitation services, and personal care for seniors with complex medical needs. They are the most medically intensive residential setting outside of a hospital.

Daily life involves a high level of medical supervision. Licensed nurses are on staff around the clock. Residents receive help with all ADLs, medication management, wound care, feeding tubes, and other medical treatments. Physical, occupational, and speech therapy are available on-site.

| Room Type | 2025 National Median Cost | Source |

|---|---|---|

| Semi-private room | $9,555/month ($114,665/year) | Genworth via SeniorLiving.org |

| Private room | $10,965/month ($131,583/year) | Genworth via SeniorLiving.org |

- Who it's for: Seniors with serious medical conditions that require 24/7 nursing care — advanced dementia with complex behaviors, post-stroke recovery, severe mobility limitations, feeding tubes, ventilator dependence, or end-stage chronic diseases.

- Who it's NOT for: Seniors who only need help with ADLs and can be safely managed in assisted living or at home. Nursing homes are medical facilities, not social models of care.

Payment: Medicare Part A covers short-term skilled nursing stays (up to 100 days) after a qualifying hospital stay of at least 3 days. Days 1–20 are covered in full; days 21–100 require a daily copay (~$200/day in 2026). Medicaid covers long-term custodial care in nursing homes for those who qualify financially. Out-of-pocket and long-term care insurance also apply.

Short-Term Rehabilitation (Subacute Care)

Short-term rehabilitation — also called subacute care — is a temporary stay in a skilled nursing facility or dedicated rehab unit for recovery after a hospitalization. Common reasons include hip or knee replacement, stroke recovery, pneumonia, or cardiac events.

Daily life is therapy-intensive. Residents receive several hours of physical, occupational, and speech therapy each day with the goal of returning home. Nursing care is available 24/7. Stays typically last 2–6 weeks.

Cost: The daily rate is the same as a nursing home (semi-private ~$314/day), but Medicare Part A covers the first 20 days in full after a qualifying hospital stay. Days 21–100 require a daily copay (~$200/day in 2026).

- Who it's for: Seniors who have been hospitalized and need intensive therapy to regain strength, mobility, and independence before returning home. The person must be expected to improve with therapy.

- Who it's NOT for: Seniors who need long-term custodial care without a therapy goal, or those who are too frail to participate in and benefit from daily therapy.

Payment: Medicare Part A is the primary payer for qualifying stays. Medicare Advantage plans may have different rules. Medicaid may cover rehab for those who qualify. Private insurance and Medicare Supplement plans may also apply.

Continuing Care Retirement Community (CCRC)

A Continuing Care Retirement Community (CCRC) is a campus that offers independent living, assisted living, and skilled nursing on one site. Residents move between levels of care as their needs change, without having to leave the community or find a new facility.

Daily life depends on which level of care the resident is in. Independent living residents enjoy apartments, amenities, and social activities. If they later need help with ADLs, they can move to the assisted living wing. If they eventually need skilled nursing, that is available on the same campus.

| Cost Component | Range | Source |

|---|---|---|

| Entrance fee (buy-in model) | $100,000 – $2 million | U.S. News |

| Monthly fee (buy-in model) | $3,000 – $8,000 | U.S. News |

| Monthly fee (rental model) | $2,000 – $6,000 | U.S. News |

- Who it's for: Seniors who can afford a significant entrance fee and want guaranteed access to higher levels of care without moving to a new community. Best for those who are still healthy enough to enter at the independent living level.

- Who it's NOT for: Seniors with limited assets who cannot afford the entrance fee, those who already need skilled nursing and would pay for services they cannot use, or those who prefer to age in place in their own home.

Payment: Almost always out-of-pocket. Some long-term care insurance policies may cover the assisted living or skilled nursing portion. Medicare and Medicaid do not cover the entrance fee or independent living costs.

Hospice Care

Hospice is a philosophy of care focused on comfort and quality of life for individuals with a terminal illness — typically a prognosis of six months or less. It is not a place but a service that can be provided at home, in a nursing home, in an assisted living facility, or in a dedicated hospice center.

Daily life centers on pain management, symptom control, and emotional and spiritual support for both the patient and family. Curative treatments are stopped. A hospice team — including nurses, social workers, chaplains, and volunteers — visits regularly and is available 24/7 by phone.

Cost: Covered in full by Medicare Part A for eligible individuals. There is no copay for hospice services, medications related to the terminal diagnosis, or respite care. Medicaid and most private insurance also cover hospice in full.

- Who it's for: Seniors with a terminal diagnosis who have chosen comfort-focused care over curative treatment. The person must be certified by two physicians as having a prognosis of six months or less if the disease runs its normal course.

- Who it's NOT for: Seniors who are still pursuing curative treatments or who have not yet accepted a terminal prognosis. Hospice is not appropriate for those who want aggressive treatment.

Palliative Care

Palliative care is specialized medical care for people with serious illness, focused on symptom relief and quality of life. Unlike hospice, palliative care can be provided alongside curative treatment at any stage of illness — not just at the end of life.

Daily life involves working with a palliative care team — doctors, nurses, and social workers — who manage pain, nausea, shortness of breath, fatigue, and other symptoms. They also coordinate care across specialists and provide emotional support. The person continues to see their regular doctors and receive treatments for their underlying condition.

Cost: Covered by Medicare Part B, Medicaid, and most private insurance. There is no separate cost to the patient beyond standard copays and deductibles.

- Who it's for: Seniors with serious chronic illness at any stage — cancer, heart failure, COPD, Parkinson's, kidney disease — who need help managing symptoms and improving quality of life. Can be provided alongside curative treatment.

- Who it's NOT for: Palliative care is appropriate for many people with serious illness. The key distinction from hospice is that curative treatment continues. There is no prognosis requirement.

Respite Care

Respite care is short-term, temporary care provided to give the primary family caregiver a break. It can be provided at home (a paid aide comes in), in a facility (a short nursing home or assisted living stay), or through an adult day care program.

Daily life during respite depends on the setting. In-home respite means the caregiver can leave the house while a trained aide stays with the senior. Facility-based respite means the senior stays in a nursing home or assisted living for a few days to a few weeks, receiving all meals, care, and activities.

2026 cost: Facility-based respite ~$350/day (U.S. News). In-home respite varies by hourly rate ($25–$40/hour depending on location and agency).

- Who it's for: Family caregivers who need a break to prevent burnout — whether for a vacation, a medical procedure, or simply to rest. Essential for long-term caregiving sustainability.

- Who it's NOT for: Respite is a temporary service, not a long-term care solution. It does not replace a permanent care arrangement.

Payment: Some Medicaid programs cover respite through HCBS waivers. VA benefits may cover respite for eligible veterans' caregivers. Some long-term care insurance policies include respite benefits. Nonprofit organizations sometimes offer subsidized respite. Otherwise, it is paid out-of-pocket.

How to Pay for Senior Care: A Quick Overview

Payment is often the most confusing part of choosing senior care. The table below summarizes which payment sources apply to which care types. This is a quick reference — each payment source has detailed eligibility rules that vary by state and plan.

| Payment Source | Covers | Does NOT Cover |

|---|---|---|

| Medicare Part A | Short-term skilled nursing (up to 100 days after hospital stay), hospice, home health care | Long-term custodial care, assisted living, independent living, adult day care |

| Medicare Part B | Palliative care, home health care (skilled), doctor visits | Custodial home care, room and board in any facility |

| Medicaid | Long-term nursing home care, HCBS waivers (home care, adult day care, assisted living in some states) | Independent living, most CCRCs (except nursing home portion) |

| VA Aid and Attendance | Assisted living, home care, adult day care, nursing home (for eligible veterans) | Independent living (unless care is added) |

| Long-term care insurance | Varies by policy — may cover home care, assisted living, memory care, nursing home | Pre-existing conditions during elimination period, independent living |

| Out-of-pocket | Any care type | N/A — but costs can be prohibitive for long-term facility care |

Next Steps: Where to Go From Here

This glossary is a starting point. Each entry above is designed to give you enough information to understand what an option is and whether it might fit your situation. For deeper guidance on specific care types, costs, and decision-making, explore the following resources:

- For a broader vocabulary of eldercare terms, see Navigating Senior Health Care: Key Terms Every Caregiver Should Know.

- For state-by-state home care hourly costs, see Elderly Care Cost Per Hour in 2026: A State-by-State Guide.

- For a full breakdown of home care payment options, see How to Pay for Senior Home Care Services in 2026.

- For help deciding between assisted living and memory care when dementia is a factor, see Assisted Living vs. Memory Care: A Decision Framework for Dementia Caregivers.

- For in-home dementia care guidance before transitioning to a facility, see Home Care for a Parent with Dementia: A Stage-by-Stage Guide.

- For a broader look at in-home support services and HCBS waivers, see Help for Elderly and Disabled Adults at Home.

Bookmark this page and return to it as your family's needs evolve. The vocabulary of senior care becomes less intimidating the more you encounter it — and having a clear reference at hand makes every subsequent conversation with providers, insurers, and family members more productive.

See This Term in Context

- The Medicare DME Prevention Paradox: What Won't Medicare Pay For and How to Plan for the Gap

Family caregivers often discover that Medicare covers hospital beds and wheelchairs but not the grab bars, shower chairs, or stair lifts that prevent falls. This article explains the coverage gap, lists what is excluded, and provides actionable strategies to bridge the out-of-pocket costs.

- Navigating Senior Health Care: Key Terms Every Caregiver Should Know

A plain-language glossary of essential senior health care terms—from Medicare and Medicaid to ADLs and advance directives—designed to help new and spousal caregivers understand the system, advocate for their loved one, and avoid costly misunderstandings.

- Palliative Care for Seniors with Chronic Conditions: When to Start and How It Differs from Hospice

This guide helps adult children of seniors with heart failure, COPD, dementia, or Parkinson's understand why palliative care is appropriate years before hospice becomes relevant, how to advocate for earlier enrollment, and what the interdisciplinary team provides for symptom management and caregiver support.

Also related: Navigating Senior Health Care: Key Terms Every Caregiver Should Know, Elderly Care Cost Per Hour in 2026: A State-by-State Guide for Family Caregivers, How to Pay for Senior Home Care Services in 2026: Medicare, Medicaid, VA, and Out-of-Pocket Costs, Help for Elderly and Disabled Adults at Home: A Family Guide to In-Home Care, HCBS, and Daily Living Support, Assisted Living vs. Memory Care: A Decision Framework for Dementia Caregivers, Home Care for a Parent with Dementia: A Stage-by-Stage Guide to Options, Costs, and When to Transition

Comments

Join the discussion with an anonymous comment.