Paying for Home Help for an Elderly Parent: A 2026 Guide to Your Options

For: adult child10 minutesReviewed: 2026-06-27

Paying for Home Help for an Elderly Parent: A 2026 Guide to Your Options

Learn how to pay for home help for an older adult — from Medicare and Medicaid to VA benefits, insurance, and private pay options — with 2026 cost data and step-by-step guidance for matching your parent's situation to the right payment sources.

By Editorial Team

new caregiver

experienced caregiver

long-distance caregiving

spousal caregiver

working caregiver

daily routines

medication management

personal hygiene

care coordination

first steps

ADLs

IADLs

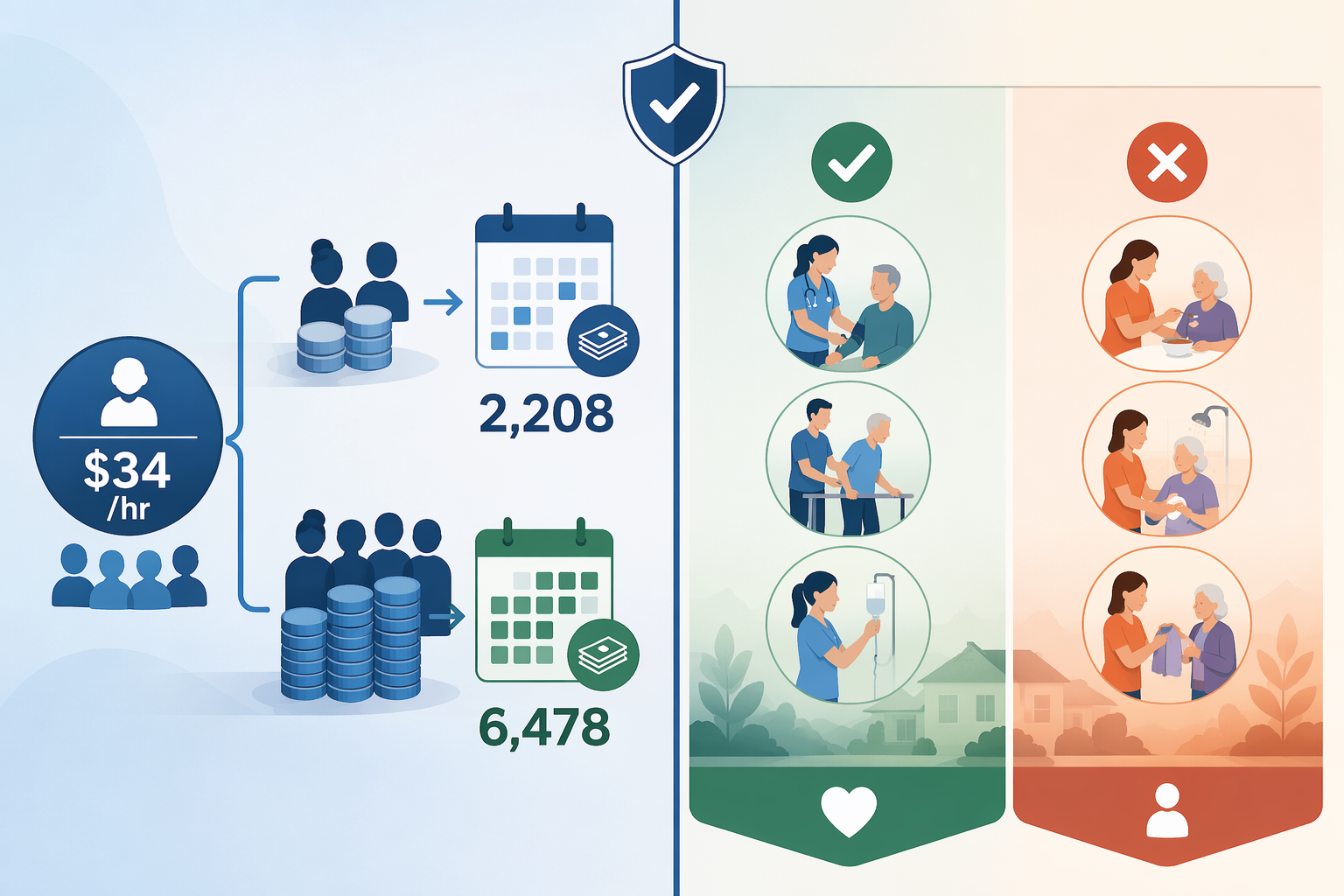

The first hard number in a home-care plan is usually the hourly rate. In 2026, the national median for nonmedical home care is $34 an hour, with state medians ranging from $25 an hour in Mississippi to $44 an hour in South Dakota. At 15 hours a week, that works out to about $2,208 a month. At 44 hours a week, it becomes about $6,478 a month.[1]

That is the moment many families start searching for home helps for the elderly and hoping Medicare has a hidden doorway. It usually does not. Medicare can cover skilled home health care when it is short-term, medically necessary, ordered by a doctor, and provided through a Medicare-certified agency. It does not pay for ongoing custodial help such as bathing, dressing, meal preparation, companionship, homemaking, or 24-hour supervision when those are the main services needed.[2][3]

That distinction is not a technicality. It decides whether you are calling a doctor and a Medicare-certified home health agency, or whether you are building a patchwork of Medicaid, VA benefits, long-term care insurance, local programs, family money, and private pay. If you are still sorting out the difference between companion care, personal care, and skilled home health, start with a basic guide to home help for elderly adults. Once you know what help is actually needed, the payment question becomes more honest.

Start with the service, not the program

A discharge planner may say “home health.” An agency may say “home care.” A family member may say “we just need someone with Mom.” Those phrases lead to different payment sources.

If your parent mainly needs…

What that usually means

First payment door to check

Nursing, therapy, wound care, injections, monitoring after illness or surgery

Skilled home health care

Medicare, if doctor-ordered and through a Medicare-certified agency

Medicaid waiver, VA grant, USDA Section 504, state or local grants

This is why two families can both say “we need help at home” and get completely different answers. A parent who needs short-term physical therapy after a hospitalization may have a Medicare-covered episode. A parent with dementia who cannot be left alone while an adult child works may need the kind of supervision Medicare excludes.

The payment sources, in the order I would usually check them

There is no perfect order for every household, but there is a practical order that prevents wasted weeks. Do not start by asking, “What programs exist?” Start by asking, “Which door could realistically open for this parent?”

Payment source

Most useful when

Main catch

Medicare

The need is skilled, short-term, doctor-ordered home health

It does not cover ongoing custodial or personal care

Medicaid HCBS waivers or state Medicaid long-term care programs

The parent meets state financial and functional eligibility rules

Rules, covered services, and waitlists vary by state

VA benefits

The older adult is an eligible veteran or surviving spouse

Eligibility depends on service history, disability, income/assets, and the specific benefit

Long-term care insurance

The parent already bought a policy and meets its benefit triggers

It is rarely an immediate solution if no policy exists

Private pay, savings, family contributions, home equity

Middle-income families who do not qualify for enough public help

The monthly cost can rise quickly as hours increase

USDA, state, local, and nonprofit programs

The need includes home repairs, accessibility, meals, respite, or limited support

Programs are local, capped, and not guaranteed

Area Agency on Aging

You need a local map of programs and applications

It is a navigation doorway, not one single funding source

Medicare: useful for skilled home health, unsafe to count on for daily care

Medicare is often the first card on the table because almost every older adult has it, and because hospital discharge can make “home health” sound broader than it is. Medicare-covered home health care is tied to medical need. The care must be ordered by a doctor, provided by a Medicare-certified home health agency, and generally focused on skilled nursing or therapy needs rather than long-term daily living support.[2][3]

That can matter a great deal after a fall, surgery, stroke, wound, or new diagnosis. A nurse may come to check a wound. A physical therapist may work on walking and transfers. An occupational therapist may help with safe movement at home. Those visits can stabilize a parent and reduce the immediate burden on the family.

But Medicare is not a long-term home aide program. If the main need is help getting out of bed, showering, changing briefs, preparing lunch, remembering medications, or being watched because wandering is a risk, families should not plan as if Medicare will fund that schedule. For a deeper look at this specific gap, see what Medicare actually pays for in home health care versus home care.

A good Medicare question is narrow: “Is there a skilled, doctor-ordered home health need right now?” If yes, pursue it. If no, move on quickly. The mistake is not applying for Medicare-covered skilled care when it is available. The mistake is losing time expecting Medicare to pay for the aide hours that will keep a parent safe every week.

Medicaid HCBS: often the most important public option, but state rules decide the answer

For long-term help with daily activities at home, Medicaid is the public program families should understand next. Medicaid is the largest payer of long-term services and supports in the United States, accounting for about 46% of LTSS spending, or $257 billion in 2023.[4] A Congressional Research Service summary also reports that roughly three in four Medicaid LTSS beneficiaries receive services through home- and community-based services rather than institutional care.[5]

That does not mean every older adult who needs help at home can get a Medicaid aide next week. Medicaid is both powerful and unforgiving. The parent usually has to meet financial limits and functional need criteria. The exact income and asset rules, the services covered, whether family caregivers can be paid, and whether there is a waiting list depend on the state.

The phrase to ask about is usually “home- and community-based services,” often shortened to HCBS. Some states run waiver programs; some use other Medicaid authorities or managed care structures. The names are not intuitive. A family may be told to apply through Medicaid, an Aging and Disability Resource Center, a county office, a managed care plan, or a waiver intake line.

When you call, do not only ask, “Does Medicaid pay for home care?” Ask these questions:

What Medicaid long-term care or HCBS programs serve older adults who need help with activities of daily living?

Is there an income or asset limit for the program, and is there a medically needy or spend-down pathway?

Is a nursing-home level of care required?

Can services include personal care, homemaker help, respite, adult day services, home modifications, or emergency response systems?

Is there a waiting list, and if so, how is priority determined?

Can a family member be paid as a caregiver under any state option?

This is also where the Area Agency on Aging becomes more than a nice phone number. It may be the fastest way to learn the local program names and the right application door. If you need a broader local-services roadmap, see this guide to Area Agency on Aging help for older and disabled adults.

VA benefits: check them early if your parent served

If your parent is a veteran, or the surviving spouse of a veteran, VA-related benefits deserve an early check. They can be meaningful, but they are not one universal home-care benefit. The right question is not “Will the VA pay?” It is “Which VA benefit could fit this service member’s record, disability status, income and assets, and current care need?”

For monthly care costs, many families look at pension-related benefits such as Aid and Attendance. For home safety changes, the benefits may be completely different. Home Improvements and Structural Alterations grants are described in 2026 funding summaries as up to $6,800 under the standard HISA limit and up to $13,600 for severe qualifying conditions, while the VA’s Specially Adapted Housing program can provide grants up to about $117,000 for eligible veterans with certain service-connected disabilities.[6][7]

Those home-modification grants do not replace an aide at the kitchen table, but they can reduce the amount of paid help needed. A ramp, accessible shower, stair solution, or safer entry may change whether one caregiver can manage transfers safely. For more detail on modification-specific funding, see funding sources for home modifications, including VA, Medicaid, and grants.

Long-term care insurance: valuable if it already exists

Long-term care insurance can be one of the cleanest ways to pay for home help, but only if the parent already bought a policy and still has it in force. If no policy exists and the need is immediate, this is usually not the rescue plan. Premiums cited in 2026 long-term care cost summaries range widely, from about $900 to $7,225 a year, depending on age, benefits, inflation protection, and other policy choices.[8]

If there is a policy, ask for the full contract, not just the sales brochure. Look for the benefit triggers, elimination period, daily or monthly benefit amount, maximum benefit pool, inflation protection, covered care settings, and whether informal caregivers can be paid. Many policies require that the insured need help with a certain number of activities of daily living or have a severe cognitive impairment.

One practical warning: do not delay filing a claim because the family is “not sure it is time.” If your parent is already paying privately for aides, and the policy may cover home care, call the insurer and ask exactly what documentation is needed. Some policies have waiting periods before benefits start.

Private pay is not a failure; it is the middle-income reality for many families

Many households land here after Medicare is too narrow, Medicaid is unavailable or delayed, VA benefits do not apply, and no long-term care policy exists. That is not poor planning. It is the structure of the U.S. long-term care system.

Private pay may come from the older adult’s income, savings, retirement accounts, family contributions, or home equity. Some families use a home equity line of credit, sell a home, rent out a property, or consider a reverse mortgage when the homeowner is 62 or older. Those choices deserve careful advice because they can affect taxes, inheritance, Medicaid eligibility, housing security, and what happens if the parent later needs facility care.

The key is to convert the hourly quote into a monthly and yearly plan before everyone gets used to a schedule they cannot sustain. At the 2026 national median of $34 an hour, 15 hours a week is about $2,208 a month. That may cover three five-hour shifts for bathing, laundry, meals, errands, and some respite. At 44 hours a week, the same median rate becomes about $6,478 a month.[1]

That larger number is where families need permission to compare options without guilt. Extensive home care can approach or exceed assisted living costs. In 2026 comparisons, 44 hours a week of home care at about $6,478 a month sits near assisted living median estimates of roughly $5,190 to $6,200 a month, while a nursing home semi-private room is cited around $9,581 a month.[1][8] Those are not interchangeable settings, and the right answer depends on safety, dementia, staffing, medical needs, housing, and what the parent wants. But the math belongs in the conversation.

Home repairs, accessibility grants, and smaller programs can still matter

Not every funding source pays for an aide. Some pay for the conditions that make home care safer or less intensive. The USDA Section 504 Home Repair program, for example, provides grants of up to $10,000 to very-low-income homeowners age 62 or older for repairs that remove health and safety hazards.[9]

State and local programs may help with meals, transportation, minor home repairs, respite, caregiver support, adult day services, utility assistance, or emergency response systems. The frustrating part is that these programs may have different applications, eligibility rules, funding cycles, and waiting lists. The useful part is that even small supports can reduce the number of paid aide hours you need to buy.

This is another reason to call the Area Agency on Aging. Ask for a benefits screening, caregiver support options, respite programs, Medicaid long-term care contacts, local transportation, home-delivered meals, and home-modification resources. If you want a broader benefits map before calling, use a guide to government benefit programs for seniors as a checklist, not as a guarantee.

Do not forget the unpaid care already being spent

Families often underestimate the care they are already providing because no invoice arrives. AARP estimated that family caregivers provide 49.5 billion hours of unpaid care annually, valued at more than $1 trillion.[10] That figure includes care for older adults and people with disabilities across ages, so it should not be used as a household calculator. But it does name the hidden work many adult children are already doing before they hire a single aide.

Federal long-term care projections also show why this problem is not rare: about 70% of adults turning 65 are expected to need some long-term services and supports, and nearly one in five will face more than $200,000 in lifetime long-term care costs.[11] Most families are not failing because they find this expensive. It is expensive.

Still, the family contribution needs a boundary. If one daughter is covering nights, one son is paying the agency, and a spouse with health problems is handling weekends, write that down as part of the care plan. The question is not only “Can Mom stay home?” It is “What paid help is needed, what can be covered, what remains out of pocket, and who is absorbing the rest?”

A practical sequence for paying for home help in 2026

When the quotes are coming in and everyone is tired, use this order. It keeps Medicare in its proper place, gives public benefits a fair check, and forces the private-pay gap into the open.

Name the actual need: skilled nursing or therapy, personal care, companionship, supervision, transportation, meals, home modification, or some combination.

Check Medicare only for the skilled, short-term, doctor-ordered portion through a Medicare-certified home health agency.

If the need is long-term personal care, screen for Medicaid HCBS or your state’s Medicaid long-term care programs.

If the parent is a veteran or surviving spouse, check VA pension benefits, Aid and Attendance, and home-modification grants that may apply.

Find and review any long-term care insurance policy before paying months of bills out of pocket.

Call the Area Agency on Aging for state, local, nonprofit, respite, meals, transportation, and home-safety options.

Build the private-pay plan for the remaining gap, using monthly numbers rather than hourly hope.

Recompare home care, assisted living, and nursing home costs when weekly hours rise enough that home is no longer clearly less expensive.

In 2026, paying for home help is usually a patchwork. The safest first move is to stop expecting Medicare to solve custodial care and start matching your parent’s actual situation to the payment sources that might apply.

Comments

Join the discussion with an anonymous comment.