Habitat for Humanity Aging in Place vs Other Home Modification Funding: A Triage Guide

Reviewed: 2026-06-27

Habitat for Humanity Aging in Place vs Other Home Modification Funding: A Triage Guide

Choosing the right home modification funding program depends on your parent's income, location, veteran status, and homeownership. This triage guide compares Habitat for Humanity's Aging in Place program with HUD, USDA, VA, and Medicaid options so you know where to start first.

Potential funding: VA HISA, USDA Section 504, Medicaid waiver, HUD OAHMP, Habitat for Humanity Aging in Place

Cost ranges are estimates. Verify eligibility directly with each program.

By Editorial Team

Start with Habitat for Humanity Aging in Place if your parent owns the home, falls within the local affiliate’s age and income rules, and needs more than a one-off grab bar. Habitat’s strongest fit is the older homeowner who needs practical construction help plus a check on the other things that make a home unsafe again: food access, transportation, health referrals, and similar supports. Habitat describes this as a “Housing Plus” approach, pairing home repairs and modifications with human-service connections rather than treating the ramp or bathroom change as the whole problem.[1]

Start somewhere else first if one of the bigger gates points clearly away from Habitat: veteran status, rural location, existing Medicaid enrollment, or not owning the home. Those details can change the first phone call completely. A veteran may have a VA path. A very-low-income rural homeowner may need USDA first. A Medicaid enrollee may need to ask about state waiver benefits. A renter may have to begin with Medicaid, a local Area Agency on Aging, a landlord-approved program, or a HUD-funded local provider rather than Habitat.

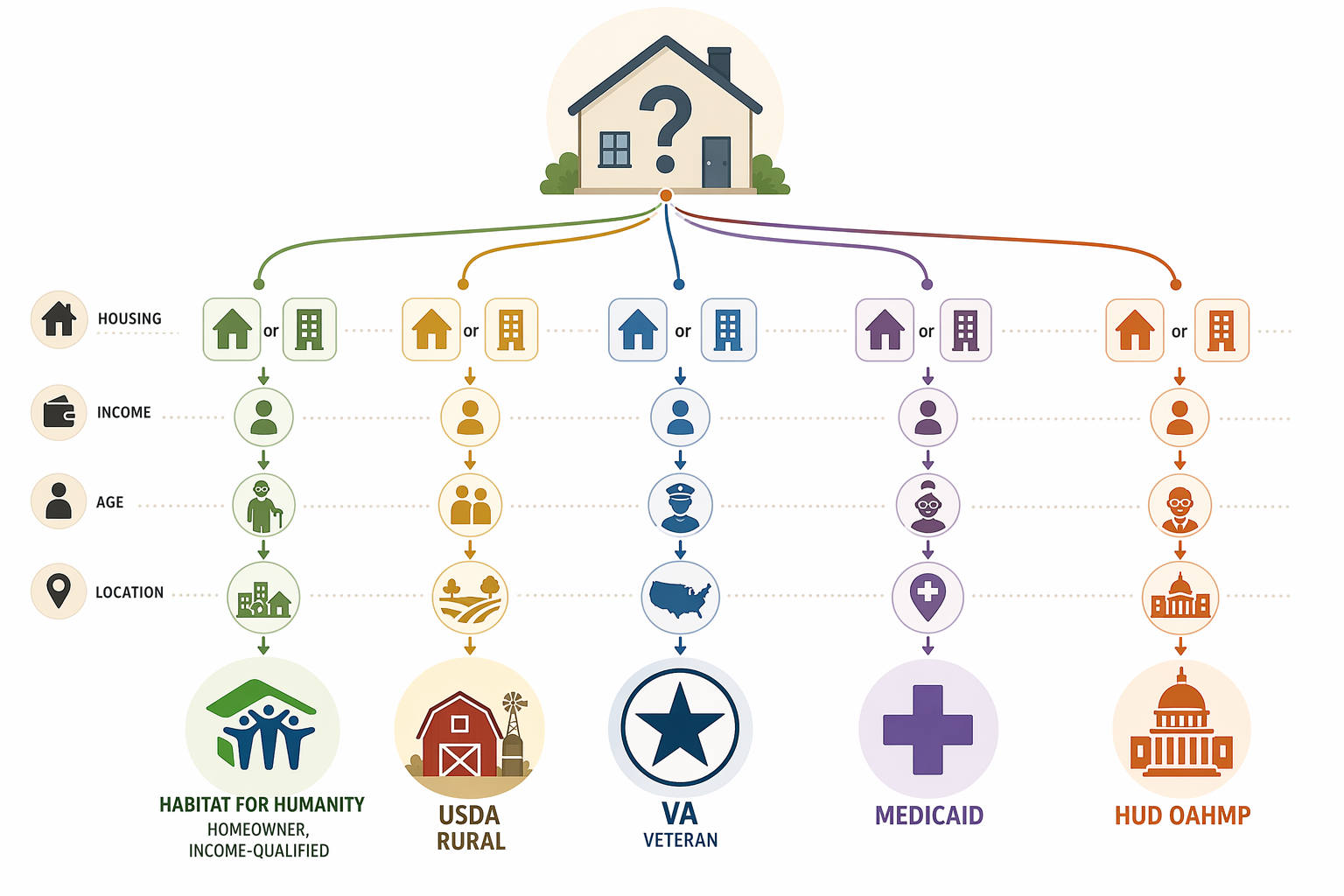

The first-door triage matrix

Use this as a sorting tool, not as a guarantee. Program rules change, local agencies run out of money, and a family may need to combine more than one source. The point is to avoid spending weeks on the wrong door.

Parent’s situation

Best first call

Why this door comes first

Watch for

Homeowner, low-to-moderate income, age 55–65+ depending on local affiliate, needs home safety modifications plus support referrals

Local Habitat for Humanity affiliate

Habitat’s Aging in Place model is built around older homeowners and may combine construction with human services through its Housing Plus approach.[1][2]

Rules vary by affiliate; national Habitat pages do not tell you whether your county has funding or an open application window.

Eligible veteran or veteran with qualifying medical need for home alterations

VA HISA before Habitat

VA Home Improvement and Structural Alterations grants can provide up to $6,800 lifetime for service-connected disabilities and $2,000 for non-service-connected conditions.[3]

VA eligibility and medical documentation matter; do not assume a general aging concern qualifies.

Very-low-income homeowner in an eligible rural area

USDA Section 504 before Habitat

USDA Section 504 can provide up to a $10,000 grant and up to a $40,000 loan for eligible rural homeowners.[4]

Rural eligibility is the gate. A household can be low-income and still be in the wrong geography.

Already on Medicaid, likely Medicaid-eligible, or receiving long-term services and supports

State Medicaid waiver or managed care plan inquiry

Home modification coverage is state-specific and often tied to Medicaid long-term services and supports or waiver authority.[5]

Coverage varies widely and waiting lists may apply.

Low-income older adult homeowner in an area served by a HUD-funded local organization

Participating OAHMP organization, not HUD directly

HUD’s Older Adult Home Modification Program funds organizations to deliver low-cost modifications and fall-prevention help; the grant is not a direct individual application.[6]

You need to find the local grantee or partner, not fill out a HUD homeowner grant form.

Renter

Medicaid waiver, Area Agency on Aging, local nonprofit, or landlord-approved program before Habitat

Habitat Aging in Place is generally a homeowner-focused lane.[2]

Any structural change may require landlord approval.

Where Habitat fits best

Habitat is worth an early call when three things line up: the parent owns the home, the household income fits the local affiliate’s limits, and the parent is old enough for that affiliate’s Aging in Place program. Habitat’s national FAQ points families back to local Habitat organizations because eligibility, services, costs, and availability are locally administered.[2] That local variation is not a footnote. It is the difference between “apply this month” and “we do not offer that program here.”

The income gate is usually the first hard stop. Habitat’s Aging in Place materials describe the program as serving low-income older adults, and affiliate pages commonly tie eligibility to area income rules.[1][2] The useful number is not a national poverty line; it is the limit for your parent’s household size in that county or service area.

Memphis Habitat shows how concrete — and local — the rules can get. Its Aging in Place program lists a homeowner requirement, an age threshold of 60 or older, household income limits, and a forgivable grant structure in which 20% is forgiven each year over five years if the homeowner remains in the home. Its posted example includes a one-person income limit of $31,900.[7] That is helpful as a sample of how an affiliate may structure the program. It is not a national Habitat promise.

The age gate also moves. In practice, families will see local thresholds around the older-adult range — often somewhere in the 55–65+ band depending on the affiliate and funding source. The only safe move is to ask the local affiliate two plain questions before describing the whole bathroom: “What age does your Aging in Place program serve?” and “What income limit applies to a household of this size?”

Habitat’s niche is strongest when the home problem is connected to daily-life fragility. A parent who needs a safer entrance, a bathroom change, and help finding transportation or food assistance is closer to Habitat’s Housing Plus model than a parent who only needs reimbursement for one medically prescribed alteration.[1] For examples of the kinds of changes Habitat affiliates may install, use the room-by-room Habitat modification guide.

What to ask Habitat before you apply

Does this affiliate currently offer Aging in Place services in the parent’s ZIP code?

What is the minimum age for the program?

What income limit applies to the parent’s household size?

Must the parent own and occupy the home?

Is the help a grant, a forgivable loan, a deferred-payment arrangement, or a subsidized repair?

Is there a waitlist, and are emergency safety issues handled differently from general repairs?

Does the program include human-service referrals or only construction work?

If those answers are favorable, move from triage to application details using the dedicated Habitat for Humanity Aging in Place program guide. If the first two answers are “not in your area” or “not eligible,” do not keep polishing the application. Go to the next door.

When another program should come before Habitat

Veterans: check VA HISA first

If your parent is an eligible veteran, do not bury that fact in a general home-repair search. VA HISA is not the same thing as a community home repair charity; it is a health-related alteration benefit with stated lifetime grant amounts: up to $6,800 for service-connected disabilities and up to $2,000 for non-service-connected conditions.[3] That does not mean every bathroom remodel qualifies. It means veteran status is important enough to move the VA inquiry ahead of a general Habitat call.

A practical order is: ask the VA care team or prosthetics department about HISA eligibility, find out what medical documentation is required, and only then compare any remaining unfunded work with Habitat, local grants, or other funding sources. For a broader comparison of VA, Medicaid, and grant options, use the home modification funding sources guide.

Rural very-low-income homeowners: test USDA eligibility early

USDA Section 504 is easy to waste time on if the address is not eligible. It is restricted to rural areas and very-low-income homeowners, but when those gates line up, the program can matter: USDA identifies up to a $10,000 grant and up to a $40,000 loan for eligible rural homeowners.[4] Those amounts are large enough that a rural family should not treat USDA as an afterthought.

Do the geography check before you start comparing paint colors, contractor bids, or local nonprofit waitlists. A parent in a rural county may have a stronger first step with USDA than with Habitat, especially if the needed work is broader than small safety modifications. A parent in a suburb or city may fail the USDA gate immediately and should move on without guilt.

Medicaid: powerful, but only in the right state and enrollment lane

Medicaid home modification help belongs in its own lane because it is tied to state rules, waiver design, managed care arrangements, and long-term services and supports. Coverage can be meaningful in one state and narrow in another, and waiting lists may apply.[5] For a parent already enrolled in Medicaid, the first call may be the case manager, waiver office, managed care plan, or Aging and Disability Resource Center rather than Habitat.

This is also the lane that may matter most for renters. Habitat’s Aging in Place work is generally homeowner-focused.[2] Medicaid or local aging-service channels may be more relevant if the parent does not own the home, though landlord approval can still control what changes are possible.

HUD OAHMP: look for the local organization, not a personal HUD grant

HUD’s Older Adult Home Modification Program is often misunderstood because the name sounds like something a homeowner might apply to directly. The grants go to organizations that deliver low-cost home modifications and fall-prevention services for older adults, not to individual families as a direct check.[6] LeadingAge described HUD awards intended to help older adult homeowners age in place, including grants to local organizations.[8]

That changes the assignment. You are not looking for a HUD form for Mom. You are looking for the nonprofit, public agency, or local provider in her area that received or participates in OAHMP-funded services. If there is one, it may be a useful door. If there is not, the national program’s existence does not help your parent this month.

The modification type matters less than the eligibility gate

Families often start with the project: a ramp, a tub-to-shower conversion, a wider doorway, better lighting, stair safety, a handrail. That is understandable after a fall or a hospital discharge. But funding programs usually start somewhere else. They ask who owns the home, where it is located, how much income the household has, whether the person is a veteran, whether Medicaid is involved, and whether the applicant is old enough for that specific program.

For a bathroom-only problem, the funding path may differ from a whole-home safety plan. Use the elderly bathroom remodel funding guide if the project is mostly bathing safety. Use the broader 2026 remodel funding guide when the work spans repairs, accessibility, and financing choices.

Where to start Monday morning

Before calling anyone, write down six facts on one page: ownership, ZIP code, household size and income, age, veteran status, and Medicaid status. Add the top two safety problems, but keep them underneath the eligibility facts. The first call is about getting through the right gate.

If the parent is a veteran, ask about VA HISA first.

If the home is rural and the parent is very low income, check USDA Section 504 eligibility early.

If the parent is already on Medicaid or likely eligible, ask the state waiver office, case manager, managed care plan, or Aging and Disability Resource Center about home modification coverage.

If the parent owns the home, is low-to-moderate income, and meets the local age rule, call the local Habitat affiliate and ask whether Aging in Place is active in that ZIP code.

If Habitat is not available, ask the Area Agency on Aging or local housing department whether a HUD OAHMP-funded provider or similar local home modification program serves the address.

If more than one door seems possible, start with the one that has the tightest status gate. Veteran status, rural eligibility, and Medicaid enrollment are not details to mention later; they can determine the entire route. Habitat becomes the right first call when those other gates do not clearly outrank it and the parent fits the local homeowner, age, and income rules.

If the household does not fit Habitat, use a broader home modification funding navigator rather than trying to make the wrong application work. If the issue started with a fall, the fall-to-home-assistance guide can help connect the safety problem to the right kind of help.

Habitat for Humanity Aging in Place is a strong first call for the right older homeowner: income-qualified, in a participating affiliate area, and in need of both home modification and wrap-around support. The best first call, though, is determined by the parent’s status — not by which program has the friendliest name.

Comments

Join the discussion with an anonymous comment.